Growing Data Products and Services

While the custom research (CR) business accounted for 56% of FY17 revenues, this is on a deliberately reducing trend (FY16: 61%; FY15: 68%). The nature of the CR work undertaken is also changing away from one-off, complex projects towards data-oriented tracking and in-depth studies building on YouGov’s data products. The more attractive opportunities are those that help to build embedded client relationships through realising the value of panel-generated data, improving the quality of the group’s earnings. The more rapid growth of this data products and services (DP&S) segment (in particular in BrandIndex and YouGov Profiles in Data Products and Omnibus in Data Services) should drive the mix to revenue parity over time. DP&S already generates 59% of adjusted operating profits, up from 52% in the prior year. With the increasing incorporation of its own gathered rich data, YouGov now sees itself as a ‘true internet company’, with its activities designed to take full advantage of the strengths of a web-based model.

Exhibit 1: FY17 Revenue by activity

|

Exhibit 2: FY17 operating profit by activity

|

|

|

|

|

|

Exhibit 1: FY17 Revenue by activity

|

|

|

|

Exhibit 2: FY17 operating profit by activity

|

|

|

|

YouGov’s growth engine is the Data Products and Services. Activity in Data Products is dominated by key product, BrandIndex, as is shown clearly in Exhibit 2, above. BrandIndex continues its very strong progress, with revenues ahead by 36% year-on-year in FY17 (FY16: +39%, FY15:+ 30%), and subscriber numbers increasing by 150 to 650 in 32 markets (from 27 in FY16). Italy, Spain, the Philippines, Taiwan and Vietnam were added in the year.

BrandIndex is targeted at brand curators in corporate clients, media planners and buyers within media agencies. It appraises sentiment towards brands in their peer space, including ‘buzz’, purchase history and likelihood to recommend, all in real time. The product is syndicated, with YouGov deciding on the sectors and brands to be covered. Some of these brands are global and so are tracked in all markets; some are national and limited to relevant country versions. Subscribers automatically see the data for all the brands covered in the market version that they buy. The additional brand owners included in the analysis who are not (yet) subscribers can then be targeted, with a clear picture already built up of the competitive landscape and their position in it. Being very sensitive to changes in opinion, BrandIndex is also a valuable tool for reputation and crisis management, when reactions can be tracked against events and in comparison to other brands’ reputations post similar events.

YouGov Profiles is also gaining ground rapidly. It was launched in November 2014 and achieved £3.7m of revenues in FY17, with annualised sales running at £7.0m as at the year end. Profiles is aimed at the corporate market/brand curators and at agencies, and is effectively the ‘front end’ of the data Cube. A sophisticated planning tool, it allows marketers to put in place very detailed segmentation of their target audience, far beyond the demographic and location data traditionally available. Profiles’ primary application is in media campaign planning, where it facilitates appropriate targeting by identifying typical characteristics of brand adherents versus the norm. It is being sold on a subscription basis, accessible via an interactive portal and has grown to 125 subscribers worldwide (from 75 last year), many of whom also subscribe to BrandIndex. Bundling these two products together gives a particularly rich resource for agencies and brand owners, and sales of this package have been made to major industry names. Profiles has now been rolled out to eight territories, with France tabled for FY18. The investment in this multi-country availability has been validated by the recent high-profile win at Dentsu Aegis Network business, which selected Profiles as its main tool for its audience understanding, media planning and strategy (in place of WPP’s TGI).

Additional connected data applications are being launched in both data products and services. These tools should allow marketers to allocate their budgets more effectively, with the capability to evaluate campaign effectiveness or test putative campaigns with seed audiences. With the ability to link into BrandIndex, the impact of television or digital campaigns can be tested, while the reach of campaigns can be tested through assessing who has been exposed – an important validation when media transparency is so much of an industry issue. The Data Intelligence Unit has also developed methodologies to incorporate dynamic segmentation and plug directly into programmatic media. There are also new data applications enabling re-contact studies via Omnibus (see below).

Together, BrandIndex and YouGov Profiles account for 97% of Data Products. The division grew by 29% at constant currency in FY17. With the main investment phase for Profiles now passed, the operating margin moved up from 27.1% in FY16 to 29.1% in FY17.

Data Services is also dominated by one offer, Omnibus, which accounts for 94% of segmental revenues, which were up by 30% in FY17 (the same high level of increase as the prior year). Omnibus is the clear market leader in the UK, where it has been available for a number of years and continues to grow at least in line with the overall MR market at +7%. YouGov’s ability to facilitate multi-country projects is bringing in larger, multinational clients and helped overall Omnibus revenues to grow by 23% in FY17. The operation of Omnibus is highly efficient and it is straightforward to incorporate additional business given the degree of automation. YouGov now has more than 1,000 clients for its Omnibus service globally and continues to add both new clients and new territories (often across multiple territories), with Acer, Bertlesmann, E.ON and Allianz Insurance among those joining the roster in the year just reported.

Again, the group is not sitting back on its success. YouGov has been extending the range of services that it is offering, in particular adding value through segmentation, increasing the degree of automation in the submission of questions into surveys and by giving more flexibility in the way that output is delivered back to the clients. A new self-service survey tool, Collaborative Insights, has been developed to allow quicker survey build both within Omnibus and as distinct custom projects, as well as having the capability to bring both together within a single dashboard.

It is also planned to deliver Omnibus survey results through the Crunch analytics software. Crunch facilitates the configuration of the output according to client requirements. It allows very large data sets to be searched, examined and analysed extremely quickly (measured in milliseconds), with the output available in flexible formats, including visualisation, dashboards and automated reporting. It also allows clients to combine and analyse data from other sources as well as that flowing from YouGov’s data products. This ability is enabling YouGov to differentiate its offer through incorporating elements of its other activities – such as adding market positioning/reputational data from BrandIndex or by accessing specialised niche samples derived from data from the existing panel, such as key corporate influencers. These additional elements are also allowing the group to pitch for more substantial pieces of business. Notable larger clients include ITV, Google, HSBC, Ford, Sun Products and Microsoft, with Bausch + Lomb, Mastercard, M&C Saatchi, Sony, SEE and Virgin Money added during FY17.

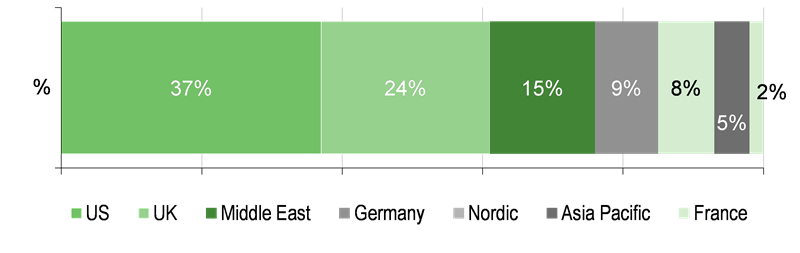

Custom research still represents the majority of revenues, but was overtaken by the operating profits generated from Data Products and Services in FY16. However, the focus of the custom research business has been changing towards projects and product-level trackers that utilise the group’s existing panel data and the YouGov Cube resource. This is already improving the quality of the achieved earnings and moving it away from the most commoditised and therefore competitive parts of the market. There is a shift from the generally ad hoc studies, building out the multi-client or syndicated studies and/or full research programmes. The latter are particularly attractive for tracking studies and research under multi-year contracts in an industry dominated by relatively small and one-off contracts. The sales effort is now focused on increasing the share of clients’ spend, for example by increasing the number of geographies covered. The move to focus custom research on the core panel-based services led to flat revenues (at constant currency) in FY17, with underlying growth in the US (+7%), the UK (+4%) and Asia Pacific (+28%, but obviously off a lower base) and reductions most notable in Germany (-37%). However, there was a good improvement in operating margins, from 12.6% in FY16 up to 14.8% in FY17. Our model anticipates further progress through FY18 and FY19, albeit at a less spectacular pace.

")