We are initiating research on Exopharm, a company focused on providing solutions for the development of targeted therapeutics using extracellular vesicles (EVs). EVs are small packets of material naturally released by cells in the body that are being investigated for their therapeutic properties and for improving drug delivery, and Exopharm has a suite of technology that may be useful for the development and manufacture of EV therapeutics. Its goal is to out-license this platform to one or more major pharmaceutical partners for the development of EV-based drugs.

Year

end |

Revenue

(A$m) |

PBT

(A$m) |

EPS

(c) |

DPS

(c) |

P/E

(x) |

Yield

(%) |

06/18 |

0.0 |

(0.2) |

(1.40) |

0.00 |

N/A |

N/A |

06/19 |

0.0 |

(2.3) |

(4.03) |

0.00 |

N/A |

N/A |

06/20 |

2.7 |

(5.3) |

(5.62) |

0.00 |

N/A |

N/A |

|

EVs: Potential for tissue-specific drug delivery

EVs are small packets of plasma membrane that bud from a range of different cell types. They resemble liposomes in some respects because they are composed of a lipid bilayer, but can contain surface proteins and carry a range of molecules important for intracellular signalling, such as nucleotides. They were initially studied as therapeutics in their own right (ie naïve EVs), but are also of great interest in drug delivery (engineered EVs). EVs are readily taken up by cells in a targeted manner and deliver their cargo directly into the cell, and the goal is that these properties can be utilised for tissue-specific delivery of therapeutics. This being said, all programmes in this space are still at a very early stage and some of the first are only now entering the clinic.

Goal is to license to drug developers/manufacturers

The company at this time is focused on delivering a suite of technology as a solution for other drug developers and manufacturers interested in entering the EV space. This includes the company’s EV purification technology (LEAP) as well as technology for controlling the surface expression (EVPS) and contents (LOAD) of the EVs. The licensing potential of the platform is highlighted by recent deals between other EV developers, Codiak and Evox, and major pharmaceutical companies, with upfronts in the range of US$20–72.5m. The company has discontinued its earlier internal development programmes on naïve EVs, but has stated it may start other internal development programmes in the future.

The company ended March 2021 with A$5.1m in cash and made a A$12m (gross) offering (16.7m shares at A$0.72) in April. The ability to finance itself into the future will largely be dependant on the company’s ability to secure partnerships, otherwise it may be forced to seek dilutive financing on the capital markets.

Company description: An EV platform for sale

Exopharm is an Australian drug delivery company focused on developing and marketing its platform for the purification and engineering of EVs. EVs are a natural method of intracellular communication that a number of companies are investigating, both for their potential as a therapy in the native state as well as potential vehicles to deliver therapeutics in a tissue-specific manner. The company has three main technologies. LEAP, its EV purification strategy, forms the cornerstone of its platform. Additionally, it recently in-licensed EVPS, a platform for engineering surface proteins on EVs, and LOAD, a method of loading EVs with specific oligonucleotides. The company’s main operational goal is to out-license these technologies as a platform to other drug companies interested in developing EVs.

Financials: Recent shift to focus on out-licensing

The company recently shifted its strategy to focus exclusively on out-licensing its development platform, whereas previously it had been developing a number of proprietary EV therapeutics. While these are also available for out-licensing, the main goal will be to offer the whole development platform as a solution to one or more larger drug companies that might be interested in the space. We expect this to reduce the company’s recurring costs, of which A$2.98m was associated with R&D in FY20 (ending June, A$5.27m net loss). A number of other EV companies have recently signed similar development agreements. The company ended March 2021 with A$5.1m in cash and subsequently made a A$12m offering (gross, 16.7m shares at A$0.72). We expect Exopharm to attempt to finance future operations through the aforementioned hypothetical licensing agreement(s).

Sensitivities: Unique to current strategy

The risks Exopharm faces are unique to its current focus on out-licensing its development platform. Most of its risk is tied up in its ability to demonstrate and communicate the potential of its platform to prospective licensees. This is in contrast with other biotechnology companies in the space, which predominantly face development risk. The shift to focusing on out-licensing (from internal development) will reduce some of the funding risk for the company, as we expect this to reduce costs and prolong its runway. However, licensing deals will need to be executed and the pressure to complete these deals before the company runs out of cash has weakened its negotiating position since it has no other active avenues for growth. Moreover, the potential licensing of Exopharm’s technology is contingent on continued interest from large pharma and hence the timing or completion of such deals cannot be assured. There have been a number of large licensing deals for EV technology in recent years, but there is no guarantee that this will continue. If EVs fail to deliver on their promise of tissue-directed drug delivery in studies run by these other companies, this may negatively affect Exopharm’s ability to license its platform through no fault of its own. The company may face significant dilution risk if it is unable to finance its operations through such licensing deals in a timely manner.

Company description: An EV development platform

Exopharm is a medical technology company focused on developing products to harness the potential of EVs. EVs are small secreted particles formed naturally by cells and are composed of cell membrane components, and they are being examined in both the academic setting and by pharmaceutical/biotechnology companies as a drug delivery mechanism. Exopharm has a series of proprietary technologies useful for the development and manufacturing of EVs for drug delivery purposes. The cornerstone of its near-term commercial strategy is the ligand-based exosome affinity purification (LEAP) technology, a method of producing high-purity EVs from a number of different tissue sources. The company’s goal is to license the LEAP technology to biotech and pharmaceutical companies interested in developing products utilising EVs by providing a large-scale manufacturing solution. There are other potential applications for the LEAP technology, such as the small-scale isolation of EVs on a single patient/tissue sample basis. Additionally, the company has licensed the technology called extracellular vesicle positioning system (EVPS) from Santa Clara University that can be used to functionalise the surface of EVs with proteins. This technology can potentially be used to target EVs to specific tissues in the body for drug delivery purposes. The final piece of the company’s three-part technology portfolio is leveraging oligonucleotide packing for amplified dosing (LOAD), a method of inserting a specified RNA cargo into EVs. These three technologies together may provide all the pieces necessary to develop an EV-based therapeutic.

The company has wound down its own previous naïve EV product development programmes. These products include Plexaris, a formulation of platelet-derived EVs, and Cevaris, EVs from allogeneic adult stem cells. Phase I safety data were recently reported for Plexaris, but the company does not intend to develop this or Cevaris further without a partner. It has indicated that these products are available for licensing (but are otherwise outside the scope of this report). The company has stated that it intends to develop additional products internally in the future, but we know little about these programmes at this time.

Exhibit 1: Exopharm technology portfolio

Technology |

Description |

Application |

EVPS |

Decorate EVs with proteins of choice |

Tissue targeting |

LOAD |

Insert RNA into EVs |

Therapeutic development |

LEAP |

Purification technique for isolating EVs |

Manufacturing of EV therapeutics, isolation of EVs from patients |

EVs are small lipid-based particles secreted by a range of cell types in the body that are used in intracellular signalling processes. The components of an EV are similar to those of a cell plasma membrane, a lipid bilayer containing various proteins, but these components can be controlled by the secreting cell to specialise these particles for a specific signalling process.

Although initially discovered in the 1980s, research into EVs has been slow and only in the past 10 years or so have researchers been able to identify the range of roles these structures have in our biology. This is in part owed to their chemical structure, which makes the particles harder to detect than protein or small molecule signals. The lipid bilayer that composes the body of the EV is sensitive to chemical and mechanical perturbation, and this helped them elude detection. Even after they were discovered, the importance of their role in intracellular signalling was underappreciated until recently. They were previously considered cellular debris or waste products. Despite their ubiquity in the natural setting, these interesting biologic structures have only recently been investigated in potential roles as therapeutics.

A vesicle in the general sense is a packet of fluid formed by a portion of membrane, and this nomenclature is generally used to refer to intracellular vesicles, which are used in a wide variety of processes within the cell. EVs by comparison are portions of cell membrane that detach from a cell body. These small packets can contain a range of proteins on the surface as well as a small amount of cytoplasm that can be loaded with a range of contents from proteins, to DNA, to mRNA.

EVs come in two main subtypes based on their origin within the cell: exosomes and ectosomes. Exosomes are EVs that are formed within a separate intracellular vesicle called the multivesicular body, which then fuses with the plasma membrane releasing the particles. The role of these EVs is primarily signalling, and a large portion of the research into EVs as a whole has been focused on exosomes. To complicate the issue, in some instance the words ‘exosome’ and ‘extracellular vesicle’ have been used synonymously. By comparison, an ectosome (also known as a microvesicle or microparticle) is an EV that is secreted directly from the surface of a cell. Exosomes and ectosomes use different machinery for their release and have different protein markers, but they appear to have many overlapping functions that are poorly differentiated in many respects. In addition to these two types of actively secreted EVs, various membranous components released from cells, such as blebs following apoptosis, can be released from the cell and make up a fraction of the circulating EVs present in the body, but are not of a specific signalling function.

|

|

|

Source: Edison Investment Research

|

The most well studied role of EVs in biology is in the activation and modulation of the immune response.1 EVs released from antigen-presenting cells can stimulate T-cells and sensitise them to a particular antigen. Additionally, cancer cells can release EVs, which can result in an immune response against them. Beyond just being carriers for antigen presentation, all types of EVs can deliver RNA to recipient cells and modulate their gene expression, which can in turn modulate immune responses.2 EVs also have a defined role in metabolic and cardiovascular diseases, mediated by the exchange of RNA between pancreatic cells, fat cells, muscle and liver.3 These signalling pathways are thought to be important for a range of metabolic disease, including atherosclerosis, diabetes-related cardiovascular disease (CVD) and metabolic adaptation associated with heart failure. Additionally, EVs isolated from mesenchymal stem cells (MSCs) can replicate some of the anti-inflammatory properties of the stem cells themselves.

Clinical applications of naive EVs

EVs have been investigated for a range of potential therapeutic and diagnostic uses. As mentioned above, they are being investigated as drug delivery vehicles (more below), but the naïve (unmodified) particles have also been studied for potential applications. EVs can be isolated from all biological fluids, which makes them attractive as a potential diagnostic. Most of this research has focused on the isolation of EVs from cancer cells as part of a liquid biopsy. These EVs can carry genetic material that is indicative of particular cancer types, and can even be used to identify cancer-driving mutations in genes such as KRAS.5

Naïve EVs have also been investigated as potential therapeutics. In many cases, these particles have been investigated as an alternative to cell therapies. The EVs from a particular cell type carry many of the same functional characteristics as the parent cell, but have a therapeutic profile more similar to traditional (eg small molecule) therapeutics. Unlike cell therapies, EVs have a more well-defined retention time in the body and can achieve a much wider distribution into tissue. In one application, the immunomodulatory aspects of EVs have been harnessed for the treatment of graft versus host disease (GvHD). One study used EVs isolated from MSCs to treat a patient, and found a significant reduction in cytokine levels and alleviation of patient symptoms.6 Additionally, MSC-derived exosomes have been used to improve outcomes following ischemic injuries in animal studies.7 There have also been a range of different studies investigating the potential of using cancer-derived EVs as cancer vaccines, given their known capacity to induce immune responses, although success in this field has been limited (as with other cancer vaccine programmes). There are multiple ongoing clinical studies investigating the therapeutic potential of naïve EVs, but these are predominantly investigator sponsored.

Engineered EVs for drug delivery

Engineered EVs are those that were modified either pre- or post-isolation and there has also been significant investment into developing such EVs as a drug delivery device. They are attractive in many respects for this application, but as yet no products have been approved based on this principle. EVs can carry a range of different payloads, ranging from small molecules to DNA, making this a versatile platform for therapeutic development. There is one ongoing clinical programme investigating therapeutic engineered EVs for this application, with additional programmes entering the clinic in the near term (see below).

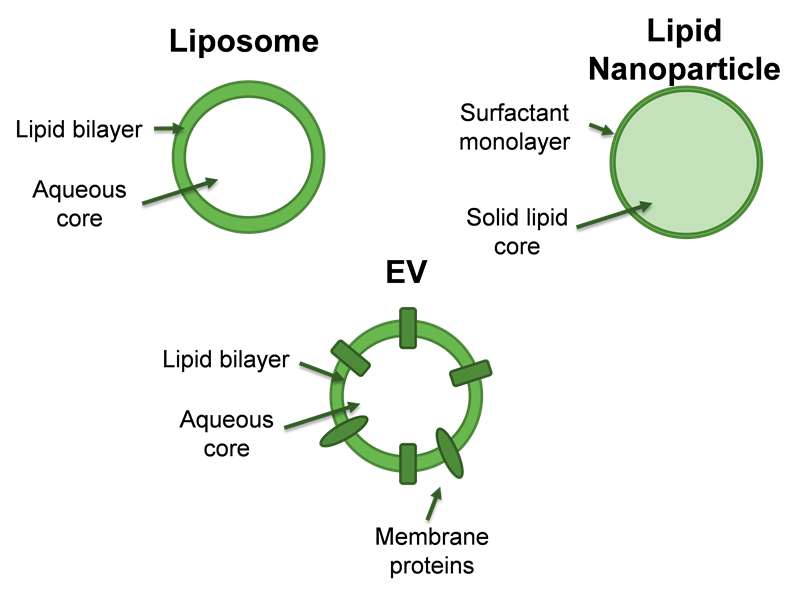

EVs share many characteristics with other drug delivery mechanisms. They are composed of a lipid bilayer, making them structurally similar to liposomes, which have a long history of drug delivery research. Simple liposomes are scavenged by the immune system, so attempts have been made to develop so-called stealth liposomes that are PEGylated and can avoid detection. The main applications that have been found for liposomes in drug delivery have been for chemotherapeutic agents (for example Onivyde, liposomal irinotecan, Ipsen), where they can provide improvements to tolerability.

Exhibit 3: Lipid-based drug delivery mechanisms

|

|

Source: Edison Investment Research

|

Lipid nanoparticles (LNPs) are another drug delivery technology that has recently gained prominence. The Pfizer and Moderna COVID-19 vaccines utilise LNPs. These particles are composed of a combination of lipids and surfactants, but ones that are not found naturally in the body. The particle is composed of a solid lipid core that contains the drug or therapeutic of interest, which is surrounded by a single layer of surfactant. This type of structure fuses more readily with cells than liposomes. Cell fusion is especially important for the delivery of nucleotide therapeutics (gene therapy, RNAi, mRNA, etc). LNPs have gained prominence in this space and are positioned as an alternative to viral vectors, which have issues of immunogenicity.

EVs are attractive as an alternative to these technologies because they are ultimately of a biologic source, as opposed to synthetic liposomes and LNPs. EVs can be loaded with drug either by inserting it into the particle’s lumen or by decorating the surface of the particle. Part of the appeal of EVs is that they are evolutionarily designed to deliver payloads into cells in a targeted fashion, and if this natural process can be co-opted it could provide a pathway for targeted drug delivery. EVs naturally contain targeting molecules that encourage their uptake by targeted cells. By controlling the proteins incorporated into the particle, this could potentially be used to direct them in the body to other specific tissues. Because this composition is closer to that of endogenous cells, the hope is that EVs will be more stable in circulation, but this appears to be a feature of the cell of origin.8

EV programmes in development

There are a number of different ongoing development programmes researching both naïve and engineered EVs in therapeutics for the treatment of a range of diseases. These programmes are generally early stage, with the vast majority in preclinical development. We believe Exopharm is well positioned to take advantage of the increasing prominence of this class of therapeutic so, while Exopharm may compete with these other companies (many of which may also be seeking to out-license their IP or technologies), we view the general development of this field as a positive for all involved. A selection of such companies is presented in Exhibit 4, but this list is not exhaustive.

There are also a large number of other small exosome companies and regenerative medicine clinics promoting the use of various products and services. EVs are offered by these clinics in a similar fashion to how stem cell treatments have been offered, with varying degrees of scientific basis and largely outside FDA oversight. The services performed at these clinics are ‘procedures’ (and are not therapeutic drug candidates) and not directly subject to FDA regulation.

The most advanced therapeutic development programme is exoIL-12 at Codiak Biosciences, which to our knowledge is the only engineered EV candidate in Phase I testing. The product uses exosomes decorated with IL-12 on the surface intended to drive anti-tumour immune responses. The company has reported data form health volunteers and is beginning to test the product in patients with cutaneous T-cell lymphoma (CTCL).

All of the other programmes currently in development for EV therapeutics are in preclinical stages of development. They are being developed for a range of different disorders and are a mix of both engineered drug delivery programmes and naïve EV programmes. In general, we believe the focus of research is shifting towards engineered EVs as the leading application for this technology.

Exhibit 4: Selection of companies involved in developing EV products

Company |

Type of EV |

Stage |

Application |

Codiak Biosciences |

Engineered |

Phase I |

Cancer |

Evox |

Engineered |

Preclinical |

Rare diseases |

Capricor |

Naïve |

Preclinical |

Duchenne muscular dystrophy |

ReNeuron |

Unspecified |

Preclinical |

Neurodegeneration, oncology, COVID-19 |

Avalon Globocare |

Unspecified |

Preclinical |

Unspecified |

ILIAS Biologics |

Engineered |

Preclinical |

Sepsis, inflammatory disease |

Carmine Therapeutics |

Engineered |

Preclinical |

Genetic diseases |

Aegle Therapeutics |

Naïve |

Preclinical |

Epidermolysis bullosa |

Aruna Bio |

Engineered |

Preclinical |

Stroke |

Anjarium |

Engineered |

Preclinical |

Unspecified |

Brainstorm |

Naïve |

Preclinical |

COVID-19, ARDS |

Exopharm |

Naïve and engineered |

N/A |

Manufacturing and development |

ExoCoBio |

Naïve |

N/A |

Cosmetics, manufacturing |

Source: Company websites and documents

Additionally, there have been some high-profile licensing deals of EV technology to major drug developers. Codiak has signed two deals: in January 2019 it announced a deal with Jazz Pharmaceuticals to develop novel cancer therapeutics using Codiak’s platform (upfront, US$20m in preclinical milestones, US$200m in other milestone for each of five targets, tiered royalties), although one of these programmes has since been discontinued. In June 2020 Codiak announced a research collaboration with Sarepta Therapeutics for five CNS targets (US$72.5m in upfront and near-term payments, plus research funding, undisclosed milestones and future royalties).

Evox has also signed two deals: it entered into a collaboration with Takeda for five rare disease targets (US$44m in upfronts and research support, US$882m in other potential payments, tiered royalties) and in June 2020 it announced another collaboration with Eli Lilly to develop brain-targeted, nucleotide-based drugs (US$20m upfront, US$10m convertible bond, up to US$1.2bn in milestones, and tiered royalties up to low double digits). The Exopharm business model is predicated on signing similar licensing deals for its platform, so we view it as encouraging that there has been interest from these major drug developers in this therapeutic area.

LEAP is the company’s proprietary technology for the isolation and purification of EVs. This purification platform is in many aspects the company’s core intellectual property, and has motivated much of its current and past research and development activities. It wholly owns the technology following the purchase in 2018 from a holding company (Altnia Operations) from which it was previously licensed. It has a royalty agreement with Altnia under which Altnia is entitled to 3% of sales and 10% of non-sales income (eg milestone fees).

LEAP is a chromatographic purification technique that uses a column filled with a specially designed ion exchange resin that has the capacity to capture EVs. An ion exchange resin is a solid substrate that is decorated with a series of ionically charged groups that can attract oppositely charged molecules in solution. In the case of LEAP, the resin is negatively charged (anionic) and binds to positively charged sites on the surface of EVs. In general, lipid bilayers like those present in EVs are negatively charged and should repel the negatively charged LEAP resin. However, the spacing between negatively charged groups on the resin is carefully controlled to interact with the sparce binding sites on EVs and avoid charge-charge repulsion (Exhibit 5). There are multiple potential interactions between the resin and EVs, but we expect the most common to be salt bridges with proteins. After EVs are bound, other components of the mixture can be washed away, and subsequently the EVs can be eluted in a purified fraction.

Exhibit 5: How the LEAP resin works

|

|

Source: Edison Investment Research, AU2019289287. Note: Not to scale. Only ionic interactions with proteins depicted.

|

One of the benefits of column chromatography is its scalability. Increased throughput can generally be achieved as simply as making a larger column. Moreover, this scalability makes it economically feasible to market smaller versions of the product for individual use for instance.

LEAP can be used in the isolation of EVs from any source: animal, human, bacterial, cancer, etc. The product has been used to purify EVs from human tissue and from tissue culture sources. For instance, it was previously used in the Phase I study (PLEXOVAL II) of the company’s platelet derived EV product Plexaris (currently deprioritised). However, a detailed account of the products manufactured by this purification method has not been published publicly, although we expect that these details are shared with potential partners.

There are several other methods that are currently employed to purify EVs. In a laboratory setting, EVs are typically purified using ultracentrifugation, subjecting the material to over 100,000 g, but this is only applicable on a very small scale, and yields are low because such g-forces can be destructive. Other chromatographic techniques can be utilised for larger-scale preparations, such as size exclusion chromatography (which separates particles based on size) and immunoaffinity chromatography (which uses antibodies to bind targeted biomarkers on EVs). Size exclusion chromatography only sorts particles by size, so similarly sized objects such as lipoproteins or viruses will contaminate the EV fraction. Affinity chromatography relies on the use of antibodies bound to the resin, which can be expensive to produce. These techniques have some limitations, which leads Exopharm to believe that it has a superior process for manufacturing on a commercial scale. We are unaware of any other companies developing ion exchange resins for EV purification. The company has filed for patents that extend until 2036 and beyond, although there are likely to be means for a competitor to develop a similar technology without infringing such patents.

There are multiple potential applications for LEAP. The most obvious is for manufacturing an EV-based therapeutic product. However, for regulatory reasons, LEAP must also have been used in the clinical trials supporting the approval of this hypothetical product. The path forward for the technology in this instance is for LEAP to be licensed to a company interested in developing EVs for a potential indication. This would provide some shorter-term cash flow (likely in the form of upfront and milestone payments) with the potential for longer-term royalty revenues.

In June 2020, the company in-licensed two technologies aimed at completing its portfolio to provide all the tools necessary to develop custom EV-based therapeutics. These technologies are meant to complement the LEAP product by addressing other facets of EV development important for therapeutic research. In both cases, EVPS and LOAD are experimental technologies that have only been tested in the laboratory (ie not yet in human trials). However, we consider the scientific rationale for each technology to be robust.

EVPS was licensed from Santa Clara University and was patented in September 2020. It is a method of producing EVs with specific proteins on the surface. These proteins can potentially be applied for any purpose, for instance, as antigens used in an EV-based vaccine. However, most of the interest in controlling protein expression on the surface of EVs has been driven by interest in controlling their tissue targeting for the purpose of drug delivery. Controlling protein expression on EVs is a very important component needed for the development of targeted EV therapeutics. Researchers at Santa Clara University discovered that the vesicular stomatitis virus G (VSV G) protein is preferentially trafficked to exosomes as they are generated and is present on their surface after they are released from cells.9 The researchers were then able to express a modified version of this protein in immortalised human cells (HEK293 cells) and obtain EVs expressing this custom protein. This technique has not yet been used for tissue-specific targeting, but is considered an essential component of the future development of EV targeting surface proteins. Many of the other companies developing engineered EVs have similar platforms for expressing custom proteins on the particle surface. For instance, Codiak uses a modified version of the protein PTGFRN to direct proteins to the EV surface. There is likely only a select number of protein tags that will be discovered to be useful in this application, so we expect there to be a limited number of companies that obtain IP in this space.

The LOAD technology is based on research performed at State University of New York, Buffalo, into the trafficking of RNA into EVs. Delivery of RNA molecules to other cells is one of the primary methods by which signals are transmitted by EVs. Researchers found that the RNA strands that were trafficked to EVs in this manner carried common sequences they termed EXO-Codes. These codes could be linked to other nucleotides, allowing the genetic content of these vesicles to be expanded or modified. The scientific details of this platform are outlined in the patents on the technology. Other companies have similar technology for loading RNA into EVs, such as Evox’s CORRECT platform. This technology is potentially useful for the development of EV-based genetic therapies. RNA interference (RNAi) has recently gained prominence as a therapeutic modality for the treatment of a range of genetic disorders, but these are generally limited to disorders of a hepatic origin because of difficulties in targeting non-liver tissue with these nucleotide therapeutics. The ability to address extra-hepatic targets is in many ways a holy grail of RNAi. EVs, on the other hand, can naturally target a range of tissues, and there is potential to have greater control with technologies like EVPS (although this is currently untested). LOAD and EVPS could therefore be an interesting platform for the development of novel RNA-based therapeutics.

Business strategy and financials

Currently, Exopharm’s sole business aim is out-licensing its technology. The company was previously focused on its own proprietary naive EV development programmes, and these programmes culminated in several development-stage products (eg Plexaris and Cevaris). However, it recently (April 2021) shifted its focus to seek partners for the further development of these products. The company has stated the intent to potentially develop some engineered EV products in the future, but its near term operational goal is rather to provide its platform as a solution to other companies. Major pharmaceutical companies have shown interest in EV technology, as evidenced by the large platform licensing deals signed by Codiak and Evox. There is potential for other pharmaceutical companies to be interested in investing in an otherwise unlicensed platform like Exopharm’s.

These changes should help Exopharm preserve cash as it seeks a partner for further development of its IP. Its R&D spend for 2020 was A$2.98m, and we expect this to reduce significantly going forward with the new business model. Net loss for the period was A$5.27m. The company ended March 2021 with A$5.1m in cash and also reported a cash outflow of A$2.9m for the quarter, which is similar to prior periods. This cash balance was subsequently supplemented by a A$12m offering (gross, 16.7m shares at A$0.72) completed in April 2021, so there is no need for financing in the near term. Exopharm reported revenue of A$2.66m for FY20, the vast majority of which was an Australian government reimbursement for clinical research. A$2.1m of this R&D payment reimbursement is still incoming, which will also defray some near-term costs. The company can claim up to 43.5% of R&D costs under the Australian government’s R&D tax incentive programme.

Exopharm has a unique risk profile owing to its strategy focused on out-licensing its technology. This strategy allows it to focus on near-term value generation through such out-licensing deals, and to avoid the risks associated with clinical development. However, the cost of this is that the company has given up much control over its fate and will be dependent on finding partners, which cannot be guaranteed. We believe that with pared-down operations, it will be able to subsist for a longer period in order to secure a partnership, but in the process, it has given up much of its leverage and has no other active avenues for growth. For instance, a potential partner could wait for the company to go bankrupt and purchase the technology at fire sale prices. These factors may affect Exopharm’s ability to execute on a deal.

EVs are an interesting technology for drug delivery, but still very experimental and only in the very early stages of clinical study. Much of this interest has been focused on the potential for these particles to deliver therapeutics in a tissue-specific manner, but this has not been demonstrated clinically yet. If EVs fail to deliver on this promise, major drug companies may lose interest in developing this technology, and the desire to license a platform like the one offered by Exopharm may dry up. Therefore, in many respects, Exopharm’s fate is tied to the success of other developers in the EV space.

However, if EVs are established as a useful drug delivery technique, Exopharm will face competition from other EV companies for potential licensing deals. There are multiple other companies offering the same basic suite of technologies for targeting EVs and loading them with therapeutics. Exopharm’s EVPS and LOAD technologies are still early stage and have undergone only limited testing. The company will need to perform additional proof-of-concept studies with these technologies to consolidate their potential utility to partners.

Finally, Exopharm will need to continue to finance its operations while looking for partners. Pro forma, it has approximately A$17m in cash (A$5m March 2021 + A$12m offering), which is approximately six quarters of cash at earlier spending levels. We expect the pared-down operations to extend this but not indefinitely, and the company will need to secure additional capital in the near term. If it is unable to close a licensing deal before that time, it may need to seek this cash on the capital markets, which may lead to substantial dilution.

|

|

|

|

|

|

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

General disclaimer and copyright This report has been commissioned by Exopharm and prepared and issued by Edison, in consideration of a fee payable by Exopharm. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2021 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person. United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |