Company description: From strength to strength

paragon was established by founder and major shareholder, Klaus Dieter Frers in March 1988, originally as an industrial electronics subcontract manufacturer, but subsequently concentrating primarily on the automotive market. Exhibit 1 below highlights the group’s timeline:

Exhibit 1: Timeline of development/major milestones

|

|

Source: Edison Investment Research

|

The group has undergone six key phases: 1988-1995: start-up in industrial electronics; 1996-2000: entry into automotive electronics; 2001-2008: emergence as a systems supplier; 2009-2011: concentration on automotive; 2012-2015: expansion to higher-quality systems and adjacent markets; and 2016 on: optimisation of the operation. The approach has been to identify emerging trends and develop products ahead of OEMs. Acquisitions have also played a part, such as SphereDesign in February 2015, which expanded the group’s capability into digital cockpit displays.

The group is organised by product divisions and following a reorganisation at the start of 2017, the divisional structure is as shown in Exhibit 2, supported by a central manufacturing organisation, productronic, which provides efficiencies of scale in manufacturing and is charged to divisions based on utilisation rates.

Exhibit 2: paragon divisional structure (since 1 January 2017)

|

")

|

Source: Edison Investment Research

|

paragon operates a centralised, highly-automated manufacturing approach with products designed for ease of production from the outset, giving the company a competitive edge over many of its peers. While there appear to be many competitors, in reality very few participate in more than one or two specific product lines. Exhibit 3 shows the locations of paragon’s operations.

Exhibit 3: paragon global locations

|

|

|

|

As the graphic shows, the group has expanded beyond its traditional German roots with the Voltabox of Texas facility opened in July 2015 complying with the Buy American Act and providing some protection against US administrative changes. Likewise, the paragon Automotive Kunshan production facility was opened in autumn 2015 and has provided the group with local capability that has seen significant indigenous OEM wins.

In June 2017, the group reorganised its corporate structure at its German Voltabox subsidiary from a GmbH into a stock corporation (AG) and transferred the shares in the American subsidiary to the German subsidiary to provide greater strategic flexibility. Exhibit 4 highlights the new structure:

Exhibit 4: Updated corporate structure

|

|

|

|

Strategy of innovation to support global megatrends

Paragon has followed a strategy of evolution built upon strong principles of technology and innovation supporting megatrends with the purpose of enhancing the driving experience for passengers of modern cars.

Management philosophy key to success

Key to paragon’s approach is the management philosophy that has been instilled by the founder and CEO Klaus Dieter Frers since the group’s creation in 1988, whereby product development is guided through analysis of what the end user will require in the future. As the group has grown, the same approach to creativity has been fostered and enhanced, maintaining the family-owned agile and entrepreneurial culture, while benefitting from the larger corporate integration capability. In April 2014, the management board was expanded with the appointment of Dr Stefan Schwehr to the post of chief technology officer (CTO), responsible for development, sales, and customer management. The appointment allowed Mr Frers to concentrate on new growth segments and internationalisation.

The business invests in product innovation using a push principle, only taking products to the OEMs once working prototypes are available and patents filed. This keeps IP with paragon and allows it to maintain an advantage over competitors who tend to be more reactive. It also allows paragon to occupy lucrative market niches in the premium segment at an early stage. The group’s growth strategy can be summarised as follows:

■

Constant development of product innovations based on megatrends (product development)

■

Gaining new automotive manufacturers as customers (market penetration)

■

Tapping into new sales areas (market development)

■

Tapping into new submarkets with new product offers (diversification)

This growth strategy is built upon both the strong historic foundation and an inherent focus on cost efficiency with a design for manufacture approach undertaken from the start. This focus is shown in the rapid uptake in automation across the group, a key feature that will ensure bottom line growth also follows the top line.

A leading tier 1 partner of premium OEMs – diversifying the base

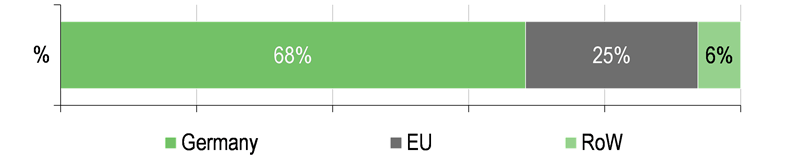

paragon’s innovative approach has allowed it to build a position as a leading tier one partner of premium OEMs, originally focused in Germany, but now expanded across the globe as shown in Exhibit 5 below:

Exhibit 5: paragon customer mix (H117 revenues)

|

")

|

|

|

While c 70% of the group’s revenues are derived from the German automakers VW Group, Daimler and BMW due to the historic uptake of enhanced features in the premium segment, the group has seen demand extend further through the OEM customer base as such features become more common across further model segments. For example, following the opening of the group’s Chinese production operation in 2015, there are several indigenous Chinese OEMs within the “other” segment such as GAC Motor, Changan and Sanden. In addition, the US auto manufacturers are responding to European quality by increasing their own comfort features increasing the opportunity with the likes of GM and Ford.

As a result of the rapid growth of the electromobility division, two of the strategic partners that paragon is supplying, Triathlon and Kiepe Electric now respectively account for 9% and 4% of group revenues from a standing start less than three years ago, showing the significant growth in this division, which now accounts for 14.5% of revenue in total in H117.

R&D investment key to approach and margin retention

With innovation a key component of paragon’s strategy, the group spends an above-average level on R&D, averaging c 10% of revenue pa over the past five years and reaching 14.8% in FY16. This compares to an average spend of mid-single percentages for other automotive electronics firms such as Hella, which intends to spend about 8% of sales on R&D. The group has a unique combination of capabilities across systems engineering, electronics, software, sensor chemistry and physics, as well as electromechanics, which positions it to develop products with unique selling points that OEMs demand. In return, paragon maintains significant IP and superior margin performance compared to typical peers in the automotive equipment supply chain.

paragon has also moved from a provider of simply components and products to a developer of entire systems, increasing the content per vehicle to many times that of a single product and becoming increasingly involved with development with OEMs as a strategic partner.

An emerging leader in electromobility – doing what it said it would do

Following the decision to directly enter the electromobility market through creation of its Voltabox subsidiary in 2013, the group has followed a clear strategy to expand into several niches of the electromobility market, focused on the capital goods segments with key strategic partners who already have established distribution networks and clients. This has seen the group deliver over >21MWh of energy capacity installed since 2013:

■

Local public transportation. This was the first subsector paragon entered and it secured an initial contract with Vossloh-Kiepe (now Kiepe Electric) in June 2013 to supply 42 backup power modules for trolley buses in Geneva and Lucerne providing combined battery, power management and electronics control with stringent automotive safety quality. This was subsequently extended in May 2014 when paragon’s US subsidiary, Voltabox of Texas, received a major order for battery packs, worth double-digit millions of dollars for the supply of backup power supply batteries for a new fleet of 200 electric trolley buses in Seattle and San Francisco, with initial production commencing in 2014 and contributing to growth in 2015 and 2016. In total, the group has supplied over 270 battery systems so far, equating to some 7.5MWh of installed capacity.

■

Intralogistics. paragon has focused on building out its presence in various segments of the intralogistics market through partnerships with key players in the sector.

•

Forklifts. In March 2015, paragon announced that it had entered into a strategic partnership for the European market with Triathlon Batterien in an exclusive agreement for the supply of lithium ion batteries for the intralogistics market. The key area here is forklift battery substitution replacing the traditional lead-acid batteries conventionally found in the warehouse environment. Triathlon is one of the leading providers in Germany of traditional lead acid batteries to this market and is driving the switch to Voltabox’s high performance lithium-ion batteries. The long-term agreement covers production of several thousand battery modules a year. Initial production of several hundred modules commenced in 2015 and since then has seen >2,500 battery modules delivered in total and over 7.5Mwh of capacity installed.

•

Automated Guided Vehicles (AGVs). The strategic partnership with Kuka’s robotics business announced in October 2016 was a key indication of the importance placed on electromobility globally. Kuka is a clear leader in the field of industrial automation and the partnership is for the group’s German Voltabox subsidiary to develop and supply batteries to power Kuka’s automated guided vehicle, which is used in areas such as automotive production. First deliveries of 96V batteries began in Q117 and we saw them on our Delbrück site visit. Given the increasing use of networked production via industry 4.0, we see this as another significant step forward for the group.

■

Mining equipment. paragon’s Voltabox of Texas subsidiary entered into a strategic partnership with Joy Global (subsequently acquired by Komatsu) in June 2016. Voltabox is to develop a range of smart battery systems for various mining equipment with first deliveries already made in Q217. This was the largest single electromobility contract won by the group and in the first stage the group will develop batteries for use in the underground mining equipment. This will be extended across all platforms through the long-term co-operation which will roll out a development programme over the next few years with significant revenue contribution from FY18. Given the size and power requirements in this segment it is a game changer for both paragon and Komatsu and sees the group partnered with a company that has global distribution in 20 countries.

With each strategic submarket opened up by paragon, there is a clear economic driver for participants to convert to lithium ion batteries from existing lead-acid battery sources and hence it tends to be a substitution process rather than new development. This significantly de-risks the uptake of the technology and hence provides greater visibility for the group than in mass market automotive areas. Where there are niche opportunities however, the group will participate such as the July 2015 €72m, six-year contract from a well-known German automotive OEM for battery packs to be used as starter motors within conventionally powered vehicles. Likewise, a development team of experienced experts has been established at the newly created facility in Aachen focused on drivetrain components including power electronics providing paragon with the full range of capabilities. The 48V lithium-ion mild hybrid technology developed by paragon holds additional potential for specific mass market applications.

Automation improving efficiency to drive margins

We recently visited the group’s Delbrück operations to witness first-hand the change since we first visited the site in 2015. There are several key observations we made that will ensure that paragon both has the necessary capacity to support the substantial growth requirements from its clients and to drive further margin accretion through increased efficiency:

Doubling of site footprint and increased workforce in place

Following the group’s 2016 capital raise, the group invested in expanding the footprint of the Delbrück site taking the total footprint of the group to c 25,000 square meters of production and storage facilities. At the same time the structure of the production line was improved along increasingly lean operational principles with a total of 21 production robots across the group by the end of 2016. This has enabled the throughput and capacity utilising existing workforce practices to increase substantially and has contributed to the group’s ability to rapidly scale up the business in-line with demand.

Automation the next stage of efficiency

While the group has utilised the concept of design for manufacture and cost from the outset, the introduction of the new automated production line for intralogistics at Delbrück provides the group with substantial future efficiency gains. Exhibit 6 below highlights management’s guidance on the key operational improvements that the line will provide:

Exhibit 6: Impact of highly automated electromobility production line for intralogistics

|

Manual |

Automated |

Cycle time in seconds (eg NMC modules) |

~575 |

311 |

Overall equipment effectiveness (OEE) |

90% |

>90% |

Limiting factors |

EOL tester, laser welding |

Defined cycle times |

Production capacity – modules/week (1 shift) |

~250 |

~415 |

Total capacity – modules/week (including US) |

~250 |

~830 |

Number of employees |

12 |

4 |

The introduction of increased automation in the electromobility division will provide paragon with greater flexibility as volumes ramp up and allow margins to significantly increase from the largely fixed cost base. The benefit of this can be seen in the electronics division, where the high degree of automation allows paragon to achieve divisional margins of c 15% vs group margins of 9% in 2016.

A scalable architecture at home and abroad

Importantly the group has designed the automated intralogistics line with growth and scalability in mind through a modular approach. The machines were provided by Aumann, with the first line commissioned in June and room for a second line already available as demand ramps up. Each line costs c €1.5m to install and commission.

With the knowledge gained at the Delbrück site, paragon could replicate the line in its Voltabox, Texas, facility as demand ramps up. Likewise, while the line currently supplies cylindrical and prismatic batteries, developments are in place to allow production of pouch cells, which would open up further market opportunities for the group. These developments highlight that the evaluation of the division is likely to continue.

")