Company description: Mittelstand machine-tool maker

Diskus Werke is a systems provider with three integrated business units, comprising Machine Tools, Tools & Components, and Production (contract manufacturing). The company had a turnover of €218m in 2016. It is long-established, having been founded in 1911. Despite its small size it is a world leader in its segments and supplies critical production equipment to a number of global industries, in particular for motor vehicle manufacture. It is majority owned by a family who provide much of the members of the supervisory board. It operates globally but manufactures its products solely in Germany. It is developing a contract manufacture business using its own equipment to produce parts for its established customers. The group embraces a number of operating subsidiaries that are each responsible for a distinct product group.

Revenues by segment/division

Exhibit 1: Revenues by segment 2016

|

Exhibit 2: Revenues by geography 2016

|

|

|

|

|

|

Exhibit 3: Revenue progression

|

Exhibit 4: Net profit progression

|

|

|

|

|

|

Exhibit 1: Revenues by segment 2016

|

|

|

|

Exhibit 3: Revenue progression

|

|

|

|

Exhibit 2: Revenues by geography 2016

|

|

|

|

Exhibit 4: Net profit progression

|

|

|

|

Products, structure and strategy

The core of Diskus Werke’s business is the manufacture and sales of machine tools. This is supported by customary spares and service activities although its equipment does not require proprietary consumables. It is developing a contract manufacturer business to produce and provide end parts which allow its customers the option of avoiding direct investment in the requisite machinery. The key to Diskus Werke’s strategy is to leverage is competencies across all parts of the metal-working process.

OEM

Diskus Werke has the capacity to manufacture equipment for every stage of the parts machining process. Its machine tools can be sold as individual standalone items but the group’s key competitive strength is to offer integrated systems combining machine tools from two or more of its production subsidiaries. These can then work the raw part with none of the loss of time and precision involved in transferring the part between separate machine tools. The ModuLine integrated process combines all the processes needed to machine an individual part. A proprietary shuttle system moves parts from one tool to another. These are usually designed to meet the specific requirements of individual customers.

Six separate subsidiaries manufacture each type of machine tool mostly at a single, different location. All are in Germany. In September 2016 the group opened a new plant built at a cost of €6m at Dietzenbach. As well as headquartering the group’s central operations, it has manufacturing capacity where subsidiary Diskus Werke Schleiftechnik produces grinding machinery and subsidiary Pittler T&S makes turning, milling and skiving machinery.

Contract manufacture

Contract manufacture is a fast growing business for the group. Revenue from the area has only been broken out separately since 2015 (11% of total revenues in 2016). Fröhlich CNC Production addresses the commercial vehicle market. It is suffering from poor capacity utilisation in its hubs business which took it into the red in 2016. Diskus Werke aims to offer customers the contract manufacture of components as a service. At present this business serves the automotive industry, both passenger and commercial vehicles.

By contrast, Diskus Werke’s home-grown contract manufacturing subsidiary, DVS Production which addresses customers in the passenger car segment is healthily profitable on sales of €13m in 2016. It recently secured a contract for several million units of epicyclic gears. In 2016 it achieved a pre tax profit margin of 12.7%, significantly above levels in the tool manufacturing subsidiaries which we estimate at an underlying 7%.

Metal forming – the heart of the product

Diskus Werke makes equipment to process metal forgings into usable components. The metal involved is predominantly steel but the process steps are common to all major metals. There are a number of quite distinct individual steps in the process and Diskus Werke makes machinery for all of the mechanical parts needed. The processes go back into the earliest history of metal-working, although they have been enormously refined over the years with advances in metallurgy and other technologies. Because of the robustness and precision of the final part required it is most unlikely that this technology will be replaced, either by new material or new manufacturing processes. Each individual step is critical to the manufacturing process.

We describe the process in full for gear making equipment. It varies somewhat for the manufacture of other parts although the basic principles hold good.

1.

The raw part is forged into approximately the shape that is required. The part that emerges is still relatively soft.

2.

The part is “green turned” into a more exact shape. Machinery from Diskus Werke’s Pittler subsidiary performs this step.

3.

It is then power skived (pared) to create the essential form required by its purpose, typically gear teeth. Machinery from Diskus Werke’s Präwema subsidiary performs this.

4.

The part is then hardened by thermal processes. This is undertaken by the part manufacturer and uses equipment that does not form part of Diskus Werke’s range. Given the entirely different type of metallurgical and technological know-how needed, this is and is likely to remain a quite separate area.

5.

The now hardened part is machined in two steps: 1) bore ground; and 2) bore honed to create a bore that allows the part to be mounted into the complete assembly and to turn freely. Machinery from Diskus Werke’s Buderus Schleiftechnik subsidiary performs this.

6.

Finally the part is ‘gear honed’ whereby the crucial operating shapes are perfected to allow precise interoperation with other parts. Machinery from Diskus Werke’s Präwema subsidiary performs this.

7.

The part can then be washed and installed into the sub-assembly required.

Sales and service

Diskus Werke has its own sales and service operations in its main markets: Germany; Plymouth in the US; Pune in India. In China sales are conducted out of Shanghai and service from a separate location in Shenyang. The group has sales agencies in a number of countries including Brazil, Argentina, the UK, Spain, Italy, Sweden, Turkey and Russia.

The market, clients and customers

One of the striking features of Diskus Werke’s business is the disparity between a very specific small addressable market for its products and the scale of its customers’ industries.

Exhibit 5: Segmentation of Diskus Werke’s market 2016

|

|

Source: Company data and Edison estimates

|

Diskus Werke stands out as being the only company in this sector that supplies all segments, providing scale, market access and intelligence, and long-term relationships with its clients. Most important, though, is that Diskus Werke’s ability to address a broad range of segments is supported by its key product advantage of being able to offer fully integrated, modular systems.

Competition

Diskus Werke leads most segments it operates in. Its competitors are overwhelmingly small, privately owned companies on which data is almost completely unavailable. Unless stated, they are German companies. It can be inferred that Diskus Werke’s leadership looks reasonably secure, based on information provided in the company’s 2012 prospectus.

■

Hard grinding and turning of gears. Diskus Werke’s Buderus Schleiftechnik leads ahead of EMAG Holding and Schleifring.

■

Surface grinding. Diskus Werke’s Diskus Schleifmaschinen leads ahead of Melchiorre (Italy) and Supfina Grieshaber.

■

Lathes for 600m to 1,600m. Diskus Werke’s Pittler leads along with MAG Hessap

■

Honing and milling of gear wheels. Diskus Werke’s Präwema has clear market leadership over Fässler (Switzerland) which only produces honing equipment and Profilator, which only produces milling machines.

Diskus Werke’s customers are focused on a relatively small number of industries.

Clients

Diskus Werke’s customers are mainly major industry leaders in its target industries. They operate globally although there is something of a bias toward European and German firms.

■

Passenger vehicles: The presence of two major Indian manufacturers is noteworthy

BMW, Fiat, Volvo, Toyota, Hyundai, General Motors, Ford, Getrag (parts), Magna (parts), Mercedes Benz, Tata, Mahindra, Lexus, Audi, SEAT, Volkswagen, Harley-Davidson, Miba, Getrag Ford Transmissions (parts).

■

Commercial vehicles: European names predominate but Caterpillar is an important US reference Mahle (Components), Scania, Steyr, Zahnradfabrik Friedrichshafen (Components), Volvo, Mercedes Benz, Caterpillar, Daimler, Claas, Knorr-Bremse (Components), MAN.

■

Machine tools: ThyssenKrupp, Voith, Schaeffler Group, Rexroth, Liebherr, FibroGSA, Siemens, Flender, Heidelberger Druckmaschinenen VEM.

■

Aerospace and other: Rolls-Royce, General Electric, EADS, MTU, Snecma.

Customer industries

In Exhibit 5 and in this section we show Diskus Werke’s revenue breakdown by customer industry in 2016 and discuss these in turn.

Exhibit 6: Diskus Werke sales by customer industry 2016

|

|

|

|

Diskus Werke’s dominant customer group is in the “drive train” segment; in practice, automotive manufacturers. Gears and shafts are the principal parts manufactured on Diskus Werke equipment. The key driver is the level of investment by the automotive industry globally. Reliable statistics on investment are hard to come by, but the volume of production provides a worthwhile proxy. Practically all automotive vehicles require parts that can only be made by the type of machine that Diskus Werke manufactures, above all gears. There have been no material changes in the machine engineering content of automotive vehicles so there is a fairly direct relationship between vehicle production capacity and the installed base of relevant tools.

Exhibit 7: World vehicle production (cars and commercials)

|

|

|

|

By the standards of such a mature industry, automotive globally has enjoyed healthy growth in recent years. This has been mainly due to the expansion of production in China and other, to some extent, related areas in Asia-Pacific. China is now by far the largest single national market accounting for 30% of the total. The growth in 2016 for China and Other Asia offsets declines or slower growth in other world regions (see Exhibit 7)

Exhibit 8: Regional trends in production

|

|

2012 |

2013 |

2014 |

2015 |

2016 |

Germany |

|

-8.1% |

-7.0% |

4.6% |

5.5% |

0.5% |

Other EU |

|

-6.6% |

-6.8% |

5.6% |

15.3% |

4.3% |

Other Europe |

|

4.6% |

2.2% |

-7.7% |

-17.0% |

-0.8% |

N America |

|

17.2% |

22.4% |

10.3% |

8.8% |

1.2% |

S America |

|

-0.6% |

6.1% |

-11.4% |

-34.3% |

-10.6% |

China |

|

4.6% |

20.1% |

23.1% |

11.1% |

14.5% |

Japan |

|

18.4% |

14.7% |

-1.7% |

-3.7% |

-0.8% |

Korea |

|

-2.0% |

-2.9% |

-0.8% |

0.8% |

-7.2% |

Other Asia |

|

9.1% |

4.5% |

-6.0% |

-0.3% |

5.2% |

Other |

|

5.3% |

12.4% |

22.7% |

33.5% |

7.9% |

|

|

|

|

|

|

|

World |

|

5.5% |

9.3% |

6.5% |

4.0% |

4.5% |

Because companies operate globally, Diskus Werke’s long-established clients are well positioned to benefit from the huge expansion of the automotive industry in China.

Gear systems are frequently a vital component of machine tools. As with automotive, it is highly unlikely that this will be affected significantly by technological change. The end markets that drive demand for individual machine tools are so varied that it is practically impossible to identify a single aggregate worth tracking more precise than world economic growth.

Exhibit 9: World machine tool production

|

|

|

|

As with automotive, China has been a major driver of growth although this has been far more volatile in the machine tool industry with a sharp correction in 2013, which was also experienced in Japan.

Exhibit 10: Trends in German machine industry business

|

|

|

|

Trends in the domestic machine tool industry have been relatively healthy recently. It is worth noting that the industry depends heavily on export sales so that what appear as domestic sales in Diskus Werke’s reporting are in practice driven by international sales by its customers.

Another customer group for Diskus Werke are aero-engine manufacturers. Unit production by Diskus Werke customers is far lower than in automotive but the equipment is very highly specified for use in the extreme operating environment and the necessary safety requirements.

The record over the past few years has been relatively volatile. In 2014, turnover saw a drop of 7% spread across all regions. This would have been worse but for a strong final quarter as the first half dropped 11.5%. Weaker sales and cost increases resulted in a sharp 36% fall in EBIT.

Exhibit 11: Absolute EBIT

|

|

|

|

|

|

|

Exhibit 11: Absolute EBIT

|

|

|

|

|

|

|

|

|

Sales returned to healthy growth in 2015 with a 24% surge that took the total to record levels. Top line growth continued in 2016 with a corresponding benefit to profits with EBIT up 55% to €14m albeit short of record levels. This allowed the dividend to be more than doubled to €0.21 from €0.10 in the three preceding years.

Top line growth moderated to 10% in 2016 but the boost to profitability was more than offset by the onset of severe losses at three subsidiaries (Pittler, Diskus Werke Schleiftechnik and Fröhlich). Pittler T&S saw sales fall 7% to €19.4m and the problem was magnified by loss-making contracts. No further detail was given but we observe that the subsidiary is working on an innovative networked production system for wheel hubs. Pre tax loss ballooned from €0.1m to €1.9m. Turnover slumped 16% to €15m at Diskus Werke Schleiftechnik leading to a turnaround from profits of €0.3m to a loss of €2.0m. The commercial vehicle contract manufacturing subsidiary Fröhlich recorded a 26% improvement in turnover to €15.3m but losses rose from €0.2m to €2.3m. This was ascribed to low capacity utilisation in the wheel hub segment. The incremental burden of €6m or so at these three subsidiaries eliminated what would otherwise have been a healthy gain in EBIT and the group total fell 18% to €11.4m.

EPS fell by one third to €0.52 and the dividend was cut modestly from €0.21 to a still well-covered €0.20. The company appears to calculate EPS directly from the net profit without taking minorities into account. The damage was further magnified at the attributable level to a fall of 60% by a large minorities charge of €2.5m.

Balance sheet and cash flow

At end 2016 Diskus Werke had net debt of €57m. Net cash flows, at €3.4m, were positive (a negative €0.8m in 2015), in spite of increased capex (€11.4m vs €7.8m, influenced by the new plant at Dietzenbach).

The fall in financial costs has gone some way to compensating for the decline in operational profitability. With debt/equity around 50% there is clearly some leverage in this respect.

Exhibit 13: Financial charges

|

|

|

|

|

|

|

Exhibit 13: Financial charges

|

|

|

|

|

|

|

|

|

The drop from the high levels of bank debt in 2012 and 2013 when debt/equity reached 66% was achieved by a sharp reduction in working capital requirements which was cut by €9m in 2014. The equity ratio is just above 50% which is entirely comfortable.

Outlook

The group’s budget for 2017 anticipates growth in both sales and profits. As the order book at end 2016 was 2% up on the level the year before at €125m, this will have made for a reasonable start to the year but it appears that forward visibility has been declining; 2013 turnover was 75% covered by the order book at end 2012 and this ratio has fallen every year since then. In the 2016 annual report the budget target was described as ambitious but achievable. There was no statement as to measures taken to eliminate the burden from the three loss-making subsidiaries. However, with appropriate caveats, management, in its annual report published 22 June 2017, indicated a 2017 target for sales of €220m and an EBIT margin of 7%.

By 2020 the group aims to boost contract manufacturing to 20% and the tool business to 20% of total turnover at the expense of the share of products, whose contribution is slated to fall to 60%. This suggests that confidence in the area is undimmed by the losses at Fröhlich.

Catalysts and sensitivities

We would foresee the following as significant factors in the development of results and sentiment.

■

Firm news on improvements at 2016’s problem subsidiaries would give a very substantial fillip. Bringing them back to breakeven alone would restore EBIT margin towards the levels of 8-9% recorded in 2011 and 2012. Full turnaround to the levels of profitability of other subsidiaries would take the group margin to 10% or above.

■

Provided that the losses at Fröhlich prove to be non-structural, news of wins in the contract manufacturing sector would be especially well received given the far higher profit margins being achieved in this area.

■

The global level of car production will have a major impact. Possibly the most important imponderable is the extent to which the Chinese market holds onto or extends the huge gains of recent years. As it is now the most important single national market the leverage is accordingly great. The risk that the heavily cyclical US market might start to turn down is less important in a global context but given its value to German car exporters this might be damaging.

■

The trend towards all electric vehicles is a negative for Diskus Werke’s business although it would take a long time for this to feed through to results. All electric vehicles do not need gearboxes, but do require an e-powertrain which uses around 30% of the parts compared to traditional gearboxes.

Management, organisation and corporate governance

The company is in practice privately held as part of the Rothenberger family interests.

One of the three members of the management board is a member of the family, Bernd Rothenberger. Family members account for half of the six members of the supervisory board.

Ownership of the company is overwhelmingly in the hands of the Rothenberger family: the family investment holding company Rothenberger 4XS owns 66%, the interests of Günter Rothenberger own a further 18%. Three private companies, FWI Fritz Werner Int., MF Heid and Pittler MF hold 15% together. At 0.42% the free float is extremely small. There appears to be no reason to expect this to alter in the foreseeable future.

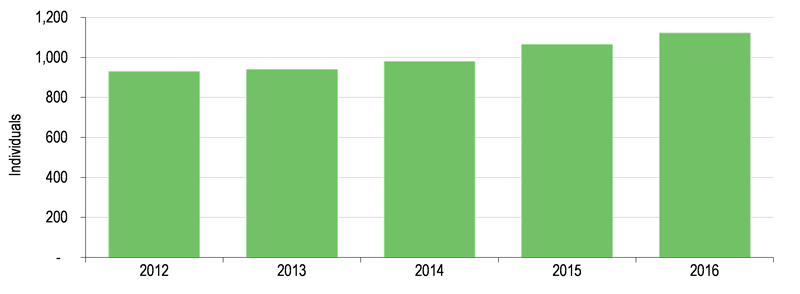

Headcount

Diskus Werke is heavily focused on developing and retaining highly qualified personnel. Some 10% of the staff has higher education qualifications eg engineers. It has steadily expanded headcount to meet current and anticipated growth.

Exhibit 15: Diskus Werke group average headcount

|

|

|

|

Exhibit 16: Financial summary

Year end December (€m) |

2012 |

2013 |

2014 |

2015 |

2016 |

P&L Items |

|

|

|

|

|

Turnover |

165,859 |

169,514 |

160,498 |

199,153 |

218,440 |

Materials |

-73,719 |

-67,894 |

-62,888 |

-98,437 |

-100,274 |

Payroll |

-50,524 |

-52,682 |

-56,164 |

-62,147 |

-66,635 |

Depreciation |

-8,775 |

-8,249 |

-9,589 |

-9,346 |

-9,502 |

EBITDA |

23,537 |

22,265 |

18,610 |

23,351 |

20,948 |

EBIT |

14,762 |

14,016 |

9,021 |

14,005 |

11,445 |

Financial cost |

-4,295 |

-4,035 |

-3,306 |

-3,146 |

-3,000 |

Tax |

-3,814 |

-4,018 |

-2,216 |

-3,823 |

-3,367 |

Net profit |

6,628 |

5,938 |

3,481 |

7,576 |

5,078 |

Minorities |

-1,356 |

-1,431 |

-2,890 |

-964 |

-2,508 |

Balance sheet items |

|

|

|

|

|

Equity |

105,067 |

109,266 |

110,893 |

117,248 |

120,572 |

Total assets |

210,989 |

213,426 |

200,402 |

218,088 |

229,664 |

Intangible assets |

40,281 |

37,753 |

34,743 |

31,305 |

28,612 |

Tangible assets |

41,661 |

44,987 |

47,078 |

48,906 |

53,450 |

Investments |

6,649 |

6,944 |

7,130 |

6,913 |

6,682 |

Raw materials |

22,588 |

21,550 |

21,690 |

22,796 |

24,346 |

WIP |

28,799 |

19,856 |

23,803 |

28,481 |

30,271 |

Finished goods |

19,831 |

20,352 |

15,346 |

23,433 |

24,357 |

Prepayments made |

1,741 |

116 |

303 |

265 |

1,776 |

Prepayments received |

-24,529 |

-11,550 |

-22,774 |

-22,497 |

-24,467 |

Debtors |

56,585 |

56,922 |

57,584 |

65,317 |

66,502 |

Minorities |

14,521 |

14,514 |

16,466 |

23,327 |

23,864 |

|

|

|

|

|

|

Bank debt |

69,594 |

70,065 |

54,207 |

59,173 |

63,963 |

Net debt |

66,902 |

65,502 |

49,892 |

55,150 |

56,551 |

Trade creditors |

7,722 |

8,415 |

11,041 |

15,209 |

15,499 |

Operational items |

|

|

|

|

|

Order inflow |

175,062 |

150,108 |

164,376 |

211,115 |

221,319 |

Order book |

126,323 |

106,917 |

110,816 |

122,778 |

125,703 |

Average headcount (units) |

931 |

942 |

982 |

1,067 |

1,124 |

Share items |

|

|

|

|

|

EPS (€) |

0.68 |

0.61 |

0.36 |

0.78 |

0.52 |

NAVPS (€) |

10.86 |

11.29 |

11.46 |

12.12 |

12.46 |

Shares in issue (m) |

9.68 |

9.68 |

9.68 |

9.68 |

9.68 |

DPS (€) |

0.10 |

0.10 |

0.10 |

0.21 |

0.20 |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 295 Madison Avenue, 18th Floor 10017, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Edison, the investment intelligence firm, is the future of investor interaction with corporates. Our team of over 100 analysts and investment professionals work with leading companies, fund managers and investment banks worldwide to support their capital markets activity. We provide services to more than 400 retained corporate and investor clients from our offices in London, New York, Frankfurt and Sydney. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Any Information, data, analysis and opinions contained in this report do not constitute investment advice by Deutsche Börse AG or the Frankfurter Wertpapierbörse. Any investment decision should be solely based on a securities offering document or another document containing all information required to make such an investment decision, including risk factors. Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Deutsche Börse AG and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |

|