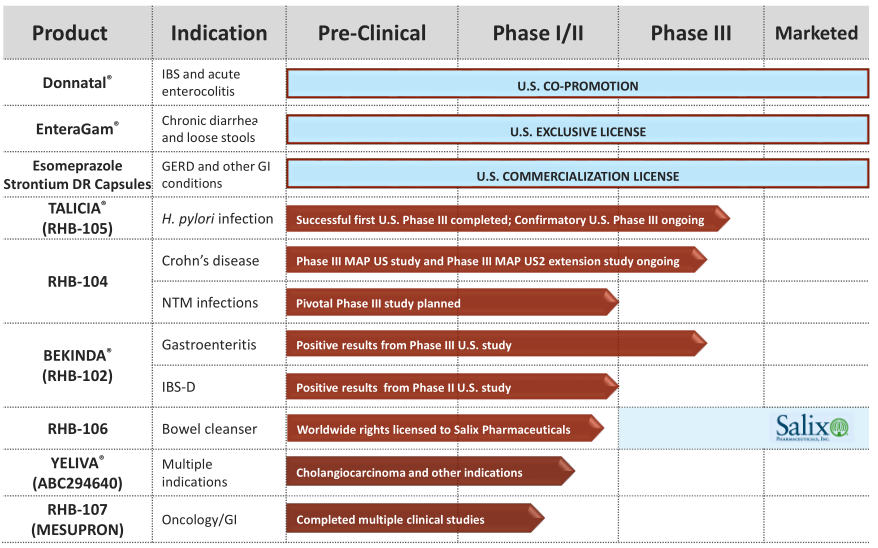

RHB-104 for CD treatment and NTM infections

RHB-104 offers potential new approach in CD

RHB-104 is a patented combination of three antibiotics (clarithromycin, rifabutin and clofazimine) in an oral capsule for the treatment of CD. The product is in Phase III development for CD, an area where current therapies have limited efficacy and pronounced side-effects, and are often very costly. CD is characterised by inflammation of the GI tract and symptoms include persistent diarrhoea, abdominal pain, rectal bleeding, weight loss and fatigue. An increasing amount of data supports the link between MAP infection in CD patients and RedHill believes it could induce and prolong remission time by treating the infection. This idea has an interesting background and has previously been explored in several clinical trials by other parties, such as a large Phase III trial funded by Pharmacia/Pfizer. In our initiation report, we reviewed the MAP hypothesis in CD, existing clinical data and RHB-104’s fit in the current landscape.

The new ongoing Phase III trial was initiated in moderate to severe CD and is now fully enrolled (since November 2017) with 331 patients. Two previous DSMB reviews (safety in December 2016; safety and efficacy in July 2017) recommended the continuation of the study without modifications. Top-line results are expected in mid-2018. To gather as many insights as possible, the company has also initiated open-label extension study to assess the safety and efficacy in those patients who remained with active CD after the treatment in the original trial. In addition, two other small studies (n = 20 each) are planned to evaluate RHB-104’s efficacy in newly diagnosed and treatment-naïve patients. RedHill also expects that a second randomised Phase III study in CD will be needed before the regulatory application.

According to the Crohn's & Colitis Foundation of America (CCFA), CD affects up to 700,000 Americans (Ulcerative Colitis is a similar number) with c 30k new cases every year, most of whom are diagnosed by the age of 35. In Europe, there are an estimated 1.6 million CD sufferers with 78k new cases every year. There is no cure for CD, although a variety of immunomodulating and immunosuppressive agents are commonly used to control symptoms. Many of these are associated with significant failure rates, side effects and safety issues (J&J's Remicade has a black box warning on serious opportunistic infections like tuberculosis). The cost per patient ranges from $300-400 per year for the cheaper generic aminosalicylates, to in excess of $20k per year for biologics (anti-TNFs such as AbbVie's Humira, UCB's Cimzia and J&J's Remicade and Simponi; or integrin-receptor antagonists such as Biogen's Tysabri and Takeda's Entyvio; source: GoodRX.com). The value of the global CD drug market is projected to be $7.9bn by 2020 (EvaluatePharma).

RHB-104 for hard-to-treat NTM infections

While CD is the primary indication for RHB-104, RedHill has decided to explore it in the treatment of NTM infections, which we now add to our NPV model. The Phase III trial is due to start in mid-2018 (Exhibit 4) and RedHill plans to position RHB-104 as a first-line treatment for pulmonary NTM infections, specifically for those caused by Mycobacterium avium complex (MAC). RedHill believes that a single pivotal trial could be sufficient, but this depends on the feedback from the FDA. The rationale for RedHill to test RHB-104 in NTM infections arises from existing evidence that MAC is susceptible to all of the antibiotics in RHB-104 (clarithromycin, clofazimine and rifabutin). In addition, clarithromycin is a macrolide class antibiotic and macrolides are considered a cornerstone in the anti-NTM regimen. Pulmonary NTM caused by MAC remains an unmet medical need with no standard of care. The FDA has granted RHB-104 QIDP for the treatment of NTM infections earlier in 2017. NTM infections are also an orphan disease.

Exhibit 4: RHB-104 clinical trial design

Trial |

Stage |

Trial design and upcoming events |

RHB-104 (clarithromycin, clofazimine and rifabutin) |

Phase III |

■

Study to start in mid-2018

■

Study design (pending FDA feedback) – n=100; double-blind, placebo-controlled Phase III study in newly diagnosed or recent repeat culture positive non-cavitary MAC disease; 1:1 randomisation RHB-104 vs placebo; six-month treatment for primary efficacy end point with continued follow-up treatment for an additional 12 months

■

Primary end point – sputum culture conversion at six months with demonstration of clinical significance

|

NTM are mycobacteria prevalent in soil and water and are defined as any mycobacterial pathogen other than Mycobacterium tuberculosis (the cause of tuberculosis) or Mycobacterium leprae (the cause of leprosy). This group encompasses more than 140 species of mycobacteria, which can infect various organs. The infections are difficult to diagnose, difficult to treat and it has been suggested that the prevalence rate is more common than tuberculosis in the industrialised world.

Pulmonary NTM infection is a chronic disease, characterised by nodules in the lungs, fibrosis and progressive lung destruction. If left untreated, it could lead to respiratory failure within just a few years. As with tuberculosis, the treatment is complicated, with some patients receiving antibiotics for over two years until they are culture-negative. NTMs share many characteristics with M. tuberculosis that make the bacteria difficult to differentiate. Molecular techniques are needed to distinguish tuberculosis from NTMs, which is difficult to access in less developed countries. Although NTMs cause a spectrum of diseases that can mimic tuberculosis, typically tuberculosis drug regimens are not effective, which results in poor treatment outcomes.

Gathering epidemiology data is challenging, but it is now thought that NTM-associated disease is much more common than previously thought: more common than TB in the industrialised world and likely increasing in prevalence globally (emedicine.com). In the US, there were approximately 86k NTM patients in 2010, a number that is estimated to be growing at a rate of 8% annually. Incidence rates are much lower. The reports on incidence of pulmonary NTM vary substantially from 5.6/100,000 in the US to 0.2-6.1/100,000 in Europe. Pulmonary manifestations account for 80-90% of NTM associated disease and around 80% of pulmonary NTM infections in the US are associated with MAC., A recent study found the incidence of pulmonary NTM in Japan to be 14.7/100,000 where MAC is the cause of around 89% of cases.

Difficult diagnostics and treatment are further confounded by lack of research in the area. Currently, NTM infections are treated with generic antibiotics (clarithromycin, azithromycin, rifampin, rafabutin, rifapentine, ethambutol) and only a few clinical trials are ongoing. Insmed is developing a new formulation of amikacin (Phase III trial ongoing) for the treatment-refractory NTM infections, while RedHill's program is targeting first-line treatment, which is a larger patient group (Exhibit 5). Savara is developing an inhaled formulation of recombinant human granulocyte-macrophage colony stimulating factor (GM-CSF) for NTM infections including MAC, currently recruiting patients to Phase II trial. Novoteris is also testing a non-antibiotic treatment, nitric oxide, which is currently being tested in Phase II for NTM infections including MAC.

Exhibit 5: Competitive landscape

Company |

Product |

Phase of development |

Notes |

Insmed |

Liposomal amikacin for inhalation |

Phase III [NCT02344004] |

■

A randomised, open-label, multi-centre study of liposomal amikacin for inhalation (lai) in adult patients with nontuberculous mycobacterial (ntm) lung infection caused by MAC that are refractory to treatment

|

Savara |

Inhaled molgramostim (recombinant human Granulocyte-Macrophage Colony Stimulating Factor; rhGM-CSF) |

Phase II [NCT03421743] |

■

Not yet recruiting (enrolment expected to complete Q318)

|

Novoteris |

Nitric oxide 0.5 % / nitrogen 99.5 % gas for inhalation |

Phase II [NCT03331445] |

|

RHB-104 in MS

In addition to CD, RedHill has also generated interesting positive data with RHB-104 in MS questioning the conventional view that MS is purely an autoimmune disease. CNS indications are not within RedHill’s focus; therefore, the company has not allocated capital to initiate further trials. CD and NTM are the two priority indications for RHB-104, while the progress in MS will depend on insights from the ongoing Phase III for CD and potential interest from partners.

In the past, MAP has been associated with diseases like type 1 diabetes, Hashimoto’s thyroiditis, sarcoidosis and MS. MS is an inflammatory, neurodegenerative disease where a person’s own immune system attacks the neurons in the central nervous system, leading to a variety of disabling symptoms that usually worsen over time. It has been proposed that a molecular mimicry between MAP proteins and human proteins could induce autoimmune pathologies and, in the case of MS, there could be similarities between MAP proteins and human anti-myelin basic protein (MBP), interferon regulatory factor 5 (IRF5) or gamma T cells. RedHill's proof-of-concept Phase IIa study (CEASE-MS) of RHB-104 in relapsing-remitting multiple sclerosis (RRMS) delivered final results in December 2016 and echoed the positive interim findings earlier in 2016. RHB-104 was evaluated as an add-on therapy to IFN-beta1a in an open-label, single-arm trial of 18 RRMS patients (17-patient data used for modified intent-to-treat analysis; 10-patient data used for per protocol analysis) who were treated for 24 weeks in combination with interferon beta-1a and then with interferon beta-1a only. The data in December 2016 showed that the annualised relapse rate (ARR, one of the most common end points in late-stage trials in the industry) at 24 weeks was 0.29 in the modified intent-to-treat (mITT) population and 0.0 in the per-protocol (PP) population, comparing favourably with data published for standalone IFN-beta therapies Avonex (Biogen) 0.67 and Rebif (Merck Serono and Pfizer) 0.87-0.91. Another end point was the relapse rate during the study. A total of 93% of the mITT patient population and 100% of the PP patient population were relapse-free at 48 weeks, which also compares well with Rebif alone (75%) and Avonex alone (63%).