Company description: Two novel classes of anti-cancer drugs

Kazia Therapeutics is an Australian biotechnology company focused on oncology drug development, listed on both the ASX (KZA) and Nasdaq (KZIA). It is developing GDC-0084, a brain-penetrant PI3K inhibitor licensed from Genentech, and a third-generation benzopyran drug, Cantrixil. A Phase IIa trial of GDC-0084 in GBM identified a higher MTD than previously reported by Genentech, and is treating an expansion cohort at the higher dose. Kazia is supporting investigator-initiated studies of GDC-0084 in breast cancer brain metastases and in the childhood brain cancer known as diffuse intrinsic pontine glioma (DIPG). It is also supporting a study of GDC-0084 in brain metastases from a range of solid tumor types that have genetic alterations of the PI3K pathway. A Phase I trial of Cantrixil in ovarian cancer is expected to report preliminary efficacy data from an expansion cohort in H219. The company’s product pipeline is summarized in Exhibit 1.

Exhibit 1: Kazia’s product pipeline

Drug candidate |

Indication |

Stage |

Next steps |

GDC-0084 |

GBM |

Phase IIa |

Report preliminary efficacy data from 20-patient expansion cohort in Q419. |

GDC-0084 |

Breast cancer brain metastases |

Phase II |

Progress update H219. Trial expected to complete in H221. |

GDC-0084 |

DIPG* |

Phase I |

Progress update H219. Trial expected to complete in H121. |

GDC-0084 |

PI3K-mutated brain metastases |

Phase II |

Initiate recruitment H219. |

Cantrixil |

Ovarian cancer |

Phase I |

Potential efficacy signals from 12-patient expansion cohort in H219. |

Source: Edison Investment Research. Note: DIPG: diffuse intrinsic pontine glioma.

Valuation: $64–103m, $10.27–16.50 per ADR

We value Kazia between $64m and $103m. We now consider a scenario where approval is obtained in 2024 after a single study as our base case, with a valuation under this scenario of $103m. Our alternative valuation of $64m models a potential approval in 2026 after a confirmatory pivotal study. Our base case valuation is equal to $16.50/ADR, or $15.85/ADR after diluting for options and convertible notes. Our valuation is based on a risk-adjusted NPV analysis, which includes net cash and our forecasts for GDC-0084 and Cantrixil, with probability of success of 10–25% to reflect the stage of development of each product.

Financials: Additional funds likely required in H2 CY19

Kazia had $4.1m cash at 31 December 2018 and also had a $2.2m R&D tax rebate receivable. It subsequently raised $1.8m through the sale of its Noxopharm shares. We expect the available funds to be sufficient to support operations into H2 CY19. We estimate that Kazia will need additional funds of $11–15m to finance the GDC-0084 Phase IIb GBM study. While the preliminary efficacy data from the GDC-0084 Phase IIa study is expected to read out in Q419, depending on the timing, funds may need to be raised in H2 CY19 before the GDC-0084 trial data are available.

Sensitivities

The key sensitivities for Kazia will be funding risk and the success of its lead drugs in clinical trials. A key question will be whether GDC-0084 works sufficiently well as a single agent in GBM to justify filing for approval after a single pivotal study, or whether a confirmatory Phase III trial (possibly in combination with radiotherapy or temozolomide) will be required for approval. Our base case scenario models a potential approval in 2024 after a single pivotal study. If a confirmatory trial is required, approval could be delayed to 2026 or later. While Kazia has fully funded the ongoing Phase IIa study of GDC-0084 in GBM, it would require additional funds of ~$11–15m for a Phase IIb trial, which could result in significant dilution of existing shareholders.

Improved tolerability of GDC-0084 in first line GBM

Kazia reported in early May that its Phase IIa study of GDC-0084 in patients with recently diagnosed GBM had determined that the MTD in this patient population is substantially higher than the MTD previously reported by Genentech (60mg/day vs 45mg/day). Genentech’s Phase I study was conducted in a sicker patient population with late-stage disease.

The safety and tolerability profile reported for GDC-0084 was encouraging. The dose-limiting toxicities in the Phase IIa study included mouth ulcers and elevated blood sugar (hyperglycemia), both of which are anticipated effects of the PI3K inhibitor class of drugs. Notably, Kazia did not observe any of the more serious side effects that are sometimes associated with this class of drugs, such as infections, liver toxicity or gastrointestinal problems.

A dose-expansion cohort of 20 patients is being recruited to gather additional safety and efficacy data at the 60mg dose.

If good tolerability is confirmed in the expansion cohort, Kazia will use the 60mg dose in its planned randomized Phase IIb study. This is a positive outcome, in our view, as the higher dose is likely to be more efficacious, thus improving the prospects for a positive result from the study.

GDC-0084 was developed by Genentech to target brain cancer

Kazia in-licensed GDC-0084 from Genentech in October 2016. The drug is an orally administered small molecule PI3K inhibitor that targets an important growth signaling pathway in cancer cells. The drug is also deliberately designed to be a moderately potent inhibitor of mammalian target of rapamycin (mTOR) kinase, to avoid the toxicity seen with drugs that are potent inhibitors of both targets. GDC-0084 was specifically developed to cross the blood-brain barrier and target GBM, which is an aggressive brain cancer for which there are few effective therapies. Abnormal PI3K signaling is associated with over 80% of cases of GBM.1

Higher doses inhibited tumor growth in Genentech Phase I

Genentech conducted a Phase I trial of GDC-0084 in patients with advanced disease, which confirmed it readily crosses the blood-brain barrier and led to dose-dependent inhibition of tumor growth. Seven of the eight patients treated at 45mg/day (the MTD identified by Genentech in patients with advanced disease) demonstrated levels of drug in the bloodstream that were associated with significant inhibition of tumor growth in preclinical models.

Exhibit 2 illustrates the tumor responses for the patients treated with GDC-0084 in Genentech’s Phase I study. The bars pointing upward from the zero baseline (x axis) in the exhibit represent how much the tumor grew, while the downward pointing bars represent tumors that shrank in volume over the period of treatment with GDC-0084. The upper red dotted line marks the 25% increase in tumor size (sum of product diameters) that is the maximum cut-off for stable disease according to the RANO2 response assessment criteria, while the lower red dotted line marks the 50% reduction in tumor volume that is the threshold for a partial response.

Although none of the patients reached the 50% reduction in tumor size that would qualify as a partial response, there was a clear dose response in terms of the impact on tumor growth, with much less tumor growth in patients treated at higher doses. For example, five of the six patients treated at the highest dose (65mg/day) achieved a best response of <25% tumor growth (the upper limit for stable disease in the RANO criteria), compared to only three of the six subjects meeting this criterion in the 45mg/day cohort. In this patient population, which has no effective treatments available, delaying disease progression by even a month or two would be a meaningful benefit.

The dose-response shown in Exhibit 2 highlights the potential importance of the higher MTD identified for GDC-0084 in recently diagnosed patients in Kazia’s Phase IIa study. It suggests that using the higher 60mg/day dose of GDC-0084 in the upcoming Phase IIb may inhibit tumor growth to a greater degree, and therefore may increase the chances of improving progression-free survival (PFS), thus meeting the primary endpoint of the study.

Exhibit 2: GBM patients in Genentech’s Phase I trial showed a trend to better disease control at higher doses of GDC-0084

|

|

Source: Wen et al. 2016 ASCO poster. Note: MTD was identified as 45mg (blue bars) in the Genentech study. The upper red dotted line marks the 25% increase in tumor size (sum of product diameters) that is the maximum cut-off for stable disease according to the RANO criteria.

|

Top-line data from expansion cohort expected Q419

Kazia is recruiting an expansion cohort of 20 patients who will be treated at 60mg/day. This second part of the study is designed to provide additional safety data and confirmatory efficacy signals and is expected to report top-line data in Q419. The subjects will undergo intensive monitoring to better understand the pharmacokinetic and toxicity profile of the drug, including the effect on major organs including the heart.

Kazia’s Phase II studies are being conducted in newly diagnosed (first-line) patients who have undergone surgery to remove the bulk of the tumor and a course of chemoradiotherapy to further reduce the tumor burden. Many patients will not have measurable tumors at the start of the study and so they will not be able to be assessed for tumor response (shrinkage) according to the RANO criteria. Therefore, we expect the key efficacy criteria to be PFS and overall survival (OS). FDG-PET brain scans will also be assessed to see whether they can predict PFS or OS.

GBM: An aggressive brain cancer with few effective treatments

GBM is the most common and most aggressive primary brain cancer. Approximately 11,500 patients are diagnosed with GBM each year in the US. GBM tumors are characterized by invasive and diffuse growth, which makes complete surgical removal difficult. Standard treatment for GBM entails surgical resection of the tumor followed by radiotherapy with concurrent chemotherapy with temozolomide (TMZ), followed by adjuvant chemotherapy with the same drug to treat the residual infiltrative component of the tumor. Despite this aggressive treatment, the disease invariably returns, resulting in a five-year survival rate of only 5%.3

Randomised Phase IIb in GBM the next step for GDC-0084

The company’s plan is for the Phase IIa study to be followed by a randomized Phase IIb study in 228 patients with recently diagnosed GBM (Exhibit 3), although this trial design could be modified after further discussions with regulators. The planned Phase IIb study will compare maintenance therapy with GDC-0084 vs standard-of-care TMZ in recently diagnosed GBM patients who have undergone standard therapy comprising surgery to remove the bulk of the tumor followed by a course of radiation therapy (XRT) combined with TMZ. After completing XRT, patients will be randomized to receive maintenance therapy with either GDC-0084 or TMZ to treat residual tumor cells and delay recurrence of the disease.

The study will target the 61% of GBM patients where tumor cells have an unmethylated MGMT promoter (which counteracts the cytotoxic effect of TMZ), as these patients receive only minimal benefit from treatment with TMZ and are in urgent need of more effective therapies. GDC-0084, which blocks the PI3K signaling pathway, is not affected by the methylation status of the MGMT promoter.

Exhibit 3: GDC-0084 Phase IIb design

|

|

Source: Kazia Therapeutics

|

Clinical trials that have PFS or OS as the primary endpoint can sometimes take a long time to complete. However, this is not expected to be the case for trials of the GBM patients that are the subject of Kazia’s studies. As Exhibit 4 shows, among five studies of GBM patients with an unmethylated MGMT promoter, the average median PFS was only 5.2 months and the median OS was 13.8 months. This indicates that a study in this patient group will be relatively quick to conduct, with PFS data expected to mature less than six months after the completion of recruitment.

Exhibit 4: Overall survival and PFS in GBM with unmethylated MGMT promoter treated with radiotherapy plus TMZ

|

Median overall survival (months) |

Median PFS (months) |

PFS at 6 months |

2-year survival rate |

Hegi et al NEJM 2005 |

12.7 |

5.3 |

40% |

14% |

Nabors et al, Neuro-Oncology 2015 |

13.4 |

4.1 |

N/A |

N/A |

Gilbert et al, JCO, 2013 |

14.0 |

5.7 |

N/A |

N/A |

AVAGLIO ASCO, 2013 |

14.6 |

5.8 |

N/A |

N/A |

RTOG-0825, ASCO, 2013 |

14.3 |

N/A |

N/A |

N/A |

Average |

13.8 |

5.2 |

|

|

Source: Edison Investment Research; Hegi et al N Engl J Med 2005;352(10):997-1003; Nabors et al. Neuro-Oncology 2015 17(5):708-717; Gilbert et al. J Clin Oncol 2013 31(32):4085-4091. Note: RTOG = Radiation Therapy Oncology Group

Revised accelerated approval scenario could see GDC-0084 launched in 2024

There are no effective therapies for GBM in patients whose tumor cells have an unmethylated MGMT promoter. Therefore, if the Phase IIb trial shows a meaningful improvement in PFS or OS in these patients, there is a good prospect that it could be eligible to seek approval based on the single pivotal Phase II study, rather than waiting for completion of a confirmatory Phase III trial before filing for approval. Therefore, we model timelines for the approval of GDC-0084 following a single pivotal Phase IIb study and for a scenario of approval following a confirmatory Phase III trial.

With top-line data from the GDC-0084 expansion cohort expected in Q419, we have revised our trial timelines. We now model a pivotal Phase IIb study commencing in Q220 and reporting top-line data in Q4 CY22 (vs Q3 CY21) with a market launch in Q2 CY24 (vs Q2 CY23), as shown in Exhibit 5.

Exhibit 5: Revised clinical trial and timeline for GDC-0084 approval following a pivotal Phase IIb study

|

|

Source: Edison Investment Research

|

Under our second scenario, which assumes that two efficacy studies are required before filing for approval of GDC-0084, we now model a shorter confirmatory study (2.5 years vs three years), with the potential market launch date unchanged at Q4 CY26, as shown in Exhibit 6.

Exhibit 6: Revised clinical trial and approval timeline for GDC-0084 under two-trial scenario

|

|

Source: Edison Investment Research

|

In its presentation to the Biotech Showcase in January, the company referred to the upcoming randomized trial of GDC-0084 in GBM as a registration study, which indicates it may be designed to support an application for full regulatory approval in this indication. This has prompted us to adopt the single pivotal study scenario in our base case valuation model (our base case previously assumed that two efficacy studies would be conducted before filing for approval).

We now evaluate the two-trial model as an alternative valuation scenario rather than the base case.

GDC-0084 joins NCI-sponsored brain metastases study

Kazia announced in May that it has entered into a collaboration with the Alliance for Clinical Trials in Oncology, a US-based cancer research network that is sponsored by the National Cancer Institute (NCI), to study GDC-0084 in the treatment of brain metastases (cancer that has spread to the brain from a primary tumor elsewhere in the body).

The Alliance study is expected to recruit around 150 patients with brain metastases in an open-label Phase II study. Patients with genetic alterations in the PI3K pathway will be treated with GDC-0084, and it is expected that around 50 patients will fall into this group. Patients with other genetic mutations will be allocated to receive either abemaciclib (Verzenio, Eli Lilly), a CDK inhibitor approved for certain forms of breast cancer, or entrectinib (Genentech) a Trk/ALK inhibitor undergoing FDA priority review for solid tumors that are positive for NTRK or ROS1 gene fusions.

The study is expected to start recruiting patients in H219 and to take around two years to complete.

Brain metastases are quite common; according to estimates from the American Brain Tumor Association, there are around 200,000 new cases of brain metastases in the US each year.4 Treatment options for brain metastases are limited, as, unlike GDC-0084, many anti-cancer drugs do not cross the blood-brain barrier.

Kazia’s announcement did not spell out whether there is any limitation on the type of primary tumor that will be included in the study, but we note that lung, breast, colorectal, melanoma and renal cancers account for the majority of people diagnosed with brain metastases.5

The Alliance study is in addition to the company’s ongoing study in patients with breast cancer brain metastases, in collaboration with the Dana-Farber Cancer Institute. One of the advantages of the new study is that it will generate data in patients with a range of different tumor types who have been treated with GDC-0084.

Kazia will support the study including by providing GDC-0084 drug as well as a financial grant (we model Kazia providing $0.4m of financial support).

We leave our modelling of the market potential of GDC-0084 in brain metastases unchanged. Our model is based on the treatment of brain metastases in patients with HER2-positve breast cancer as an illustrative indication. We may look to revise this assumption, depending on the outcome of the Alliance study.

There will soon be four GDC-0084 clinical trials underway

Once the Alliance study in brain metastases is underway, there will be four ongoing clinical trials of GDC-0084 in cancer patients, as shown in Exhibit 7. In addition to the GBM and Alliance studies described above, Kazia is collaborating in two other investigator-led trials of GDC-0084.

The first of these is a Phase II trial in collaboration with the Dana-Farber Cancer Institute to investigate GDC-0084 in combination with Herceptin in women with HER2-positive breast cancer who have developed brain metastases. Genentech showed that GDC-0084 improves survival in this indication in animal studies and the recent approval of Novartis’s alpelisib (Piqray, previously known as BYL719) validates targeting PI3K in breast cancer.

The second collaboration is with St Jude Children’s Research Hospital in a Phase I study of GDC-0084 in the aggressive childhood brain cancer DIPG. Although the number of patients with this disease is small, the lack of approved treatments for this aggressive cancer could open pathways to an accelerated approval or Breakthrough Designation. Approval could also earn a valuable FDA pediatric priority review voucher.

Exhibit 7: Ongoing and planned clinical trials with GDC-0084

Sponsor |

Phase |

Indication |

Clinicaltrials.gov identifier |

Kazia Therapeutics |

II |

Glioblastoma |

NCT03522298 |

Dana-Farber Cancer Institute |

II |

Breast cancer brain metastases (with Herceptin) |

NCT03765983 |

Alliance for Clinical Trials in Oncology |

II |

Brain metastases |

(TBA) |

St Jude Children’s Research Hospital |

I |

DIPG (childhood brain cancer) |

NCT03696355 |

Source: Kazia Therapeutics

First PI3K inhibitor approval in solid tumors

The PI3K signaling pathway plays a crucial role in cellular proliferation, metabolism, survival and apoptosis (programmed cell death). PI3K signaling is initiated by receptor tyrosine kinases or G-protein coupled receptors located at the cell surface, and by some oncogenic proteins such as Ras.

The PI3K pathway is frequently overactivated in cancer. This can occur through a variety of mechanisms including mutation and amplification of genes in the pathway, or by loss of function of the tumor suppressor PTEN, which is a negative regulator of PI3K signaling.

Of particular relevance to Kazia, the PI3Kalpha inhibitor alpelisib (Piqray, Novartis) was approved by the FDA on 24 May 2019 for treating patients with hormone receptor-positive, HER2-negative breast cancer, whose tumors carried mutations in the PIK3CA gene. In the Phase III Solar-1 study, adding alpelisib to standard fulvestrant hormone therapy almost doubled PFS (11.0 months vs 5.7 months, hazard ratio=0.65, p=0.0013) in patients with PIK3CA mutations. This is the first example of a PI3K inhibitor being approved for treating solid tumors (vs blood cancers).

The first three PI3K inhibitors that were approved all target hematological cancers (cancers of the blood cells). Idelalisib (Zydelig, Gilead Sciences) was first approved by the FDA in 2014 and is approved to treat several types of leukemia and lymphoma. Idelalisib is a selective inhibitor of the delta isoform of PI3K (PI3Kδ). A second PI3K inhibitor copanlisib (Aliqopa, Bayer), was approved for treating lymphoma in September 2017, whereas a third, duvelisib (Copiktra, Verastem) was approved for treating two types of leukemia and lymphoma in October 2018.

The approvals of these four drugs provide validation for PI3K as a target for anticancer drug development. However, none of those drugs was designed to cross the blood-brain barrier, whereas GDC-0084 was specifically designed to do just that. To the best of our knowledge, Kazia is the only company that is developing a PI3K inhibitor in GBM.

Encouraging efficacy in Cantrixil dose-escalation study

Kazia’s second drug in clinical development, Cantrixil, is being developed to target ovarian cancer, and potentially other cancers that have spread to the abdominal cavity. Cantrixil is a third-generation benzopyran drug that was the product of an in-house discovery program. Cantrixil is delivered by infusion into the abdominal cavity (intraperitoneal administration), which increases the exposure of abdominal organs, including the ovaries, to the drug. The company initiated a dose escalation Phase I study of Cantrixil in December 2016. The study recruited women with ovarian, fallopian tube or primary peritoneal cancer who had failed at least two prior lines of therapy, including standard platinum-based therapy (eg cisplatin, carboplatin or oxaliplatin).

Kazia presented a poster summarising the safety and efficacy of data from the dose escalation cohorts of the Phase I study of intraperitoneal Cantrixil (TRX-E-002-1) at the American Association for Cancer Research (AACR) conference held from 29 March to 3 April 2019 in Atlanta, Georgia. In total, 11 subjects were treated with Cantrixil at doses ranging from 0.24mg/kg to 20mg/kg. Nine subjects received at least three doses (ie one full cycle) and were evaluated for efficacy.

The study identified the MTD as 5mg/kg. The main side effects were gastrointestinal, with abdominal pain and fatigue the most common drug-related observations, although generally not dose limiting. Treatment centres have strategies in place to manage side effects such as pain, nausea and vomiting, but they were not used in this study because the investigators did not want to mask any adverse events.

Cantrixil also showed encouraging signs of anti-cancer efficacy. Five of the nine subjects (56%) who had received at least three weekly doses (one cycle) of Cantrixil achieved stable disease when evaluated six weeks after treatment commenced (Exhibit 8).

The five subjects with stable disease at the end of the six-week Cantrixil monotherapy treatment period went on to receive Cantrixil in combination with a range of chemotherapy agents. At the end of the 24-week study period, three of the five had developed progressive disease, one remained stable and one had gone on to experience a partial response, as detailed below.

Exhibit 8: Tumor evaluation of Cantrixil dose-escalation cohorts

|

|

Source: Kazia Therapeutics

|

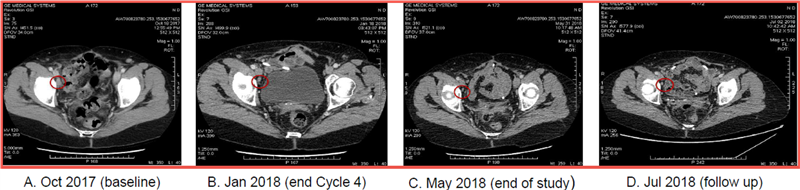

Exhibit 9 shows the progressive tumor reduction in the patient (subject 03-002) who went on to experience a partial response when treated with Cantrixil in combination with paclitaxel after completing Cantrixil monotherapy treatment.

This subject experienced substantial tumor shrinkage during the six-week period when she was treated with Cantrixil at 2.5mg/kg as a monotherapy. At the completion of Cantrixil monotherapy the patient subsequently received six cycles (18 weeks) of treatment with 2.5mg/kg Cantrixil combined with paclitaxel. The tumors continued to shrink and 12 weeks after entering the study the patient had achieved a partial response. The response was ongoing at the end of the 24-week follow-up period when the patient exited the study. Exhibit 9 also shows that the tumor shrinkage was maintained at a further assessment two months after the end of the study.

Exhibit 9: Progressive tumor reduction over an extended period observed in one patient

|

|

Source: Kazia Therapeutics.

|

Recruitment of Cantrixil expansion cohort well advanced

Kazia is recruiting a 12-patient expansion cohort that is being treated with Cantrixil monotherapy at the MTD of 5mg/kg. As of March 2019, nine of the 12 patients had been recruited. Kazia expects to fully recruit the expansion cohort in Q219 and report initial efficacy data in H219.

The 56% of subjects with stable disease at the end of the 6-week monotherapy treatment period and the substantial reduction in tumor size seen in one patient receiving combination therapy are encouraging signs that Cantrixil may inhibit tumor growth. However, it is not yet clear whether the efficacy is sufficient for it to be a commercially successful product. The expansion cohort will provide additional data to help assess the safety and potential efficacy of Cantrixil.

Future options for Cantrixil: First- or second-line combinations

Kazia’s overall business strategy is to in-license drug candidates then add value by conducting early- to mid-stage clinical development, before out-licensing or selling the program to a partner that would conduct late-stage development.

Therefore, we expect the company to seek a partner for late-stage development of Cantrixil. Depending on the level of interest from potential pharma partners and on Kazia’s available financial resources, it could also seek a partner for the next stage of Cantrixil development. Another option would be for Kazia to conduct a small study if there is a particular question that potential pharma partners want to have addressed before they commit to a transaction.

Cantrixil has shown encouraging signs of efficacy as a single agent and good tolerability when used in combination with standard second-line therapies. These two factors mean Cantrixil is likely to be well suited to use in combination therapy.

If the data from the expansion cohort are sufficiently encouraging and there is enough interest from potential partners, we suspect the likely next step would to be to test Cantrixil in combination with the investigator’s choice of standard chemotherapy drugs in either a first- or second-line setting.

High unmet need in ovarian cancer

Ovarian cancer accounts for 22,400 new cases and 14,100 deaths in the US each year, with a five-year survival rate of 47%. Worldwide, there are an estimated 239,000 new cases and 152,000 deaths annually according to the International Agency for Research on Cancer with the highest rates coming from developed countries. The majority of those diagnosed already have distant metastases, which is associated with a 28.9% five-year survival rate (see Exhibit 10).

Exhibit 10: Ovarian cancer statistics

Stage |

% of cases |

Five-year survival |

Localized (confined to primary site) |

15% |

92.5% |

Regional (spread to regional lymph nodes) |

20% |

73.0% |

Distant (metastatic) |

60% |

28.9% |

Unknown* |

6% |

25.1% |

Source: National Cancer Institute, Surveillance, Epidemiology and End Results Program. Note: *Unknown= stage of disease at diagnosis not recorded

Patients who present with ovarian cancer are typically treated with surgery followed by a platinum-based chemotherapy (such as paclitaxel and carboplatin). Unfortunately, around 70% of patients relapse in the first three years following therapy,6 although this is expected to improve, especially among the 10% of ovarian cancer patients with BRCA mutations, with the approval of the PARP inhibitor niraparib by the FDA as a maintenance therapy. PARP inhibitors are also used in those with BRCA mutations in later lines of therapy.

The situation is dire for patients who are platinum refractory or who become platinum resistant (a condition that eventually occurs to all surviving platinum-sensitive patients following repeated platinum courses). The current standard of care for platinum resistant or refractory patients is either PEGylated lysosomal doxorubicin (PLD, FDA approved in 1999) or topotecan (FDA approved in 1996), both of which typically have shown a response rate of 10–15%, PFS of approximately 3.5 months and OS of 12 months in large trials.7 This segment of the ovarian cancer population continues to be an unmet medical need and would likely be a key target for Cantrixil.

The key sensitivity for Kazia will be the success of its two lead drugs in clinical trials. A crucial question regarding GDC-0084 will be whether it works sufficiently well as a single agent in adjuvant therapy to receive approval based on a single pivotal study. In this regard, it is encouraging to note that Avastin was granted accelerated approval in 2009 for treating recurrent GBM based on the response rates observed in 141 patients. If GDC-0084 needs to be used concurrently with radiotherapy or with TMZ in order to deliver sufficient efficacy in GBM then one or more additional efficacy trials may be required, delaying potential launch until 2026 vs 2024 under a single pivotal study approval scenario. There is also a significant risk that GDC-0084 may not provide sufficient benefit to justify approval either as a single agent or combination therapy.

Although Kazia is approaching the final stages of the Phase IIa study of GDC-0084 in GBM, we estimate it would require additional funds of ~$11–15m for the randomized Phase IIb trial. This could result in significant dilution of existing shareholders given the current market capitalization of ~$15m.

Our valuation includes revenues from the development of two drugs in four disease indications, as well as (risk-adjusted) upfront and milestone payments for two licensing deals. While each of these targeted indications is supported by the current preclinical efficacy studies and evidence of a dose response in the GDC-0084 Phase I trial, the company may not ultimately pursue development of the drugs for all of these indications. In contrast, ongoing preclinical efficacy studies could identify additional disease indications that should be investigated in clinical trials. While we believe the drug development timelines used in our forecasts are achievable, at this early stage it is hard to accurately predict how long it will take to get the drugs to market.

As explained on page 6, we have swapped the GDC-0084 development programs that we model for our base case and alternative valuation scenarios for Kazia. We have also adjusted our valuation range to reflect our revised timelines for clinical development of GDC-0084 in GBM. Our revised valuation range is $64–103m (vs $64–111m), with the upper end of the range now representing our base case scenario.

Our base case valuation of $103m models a GDC-0084 market launch in 2024 following a single pivotal study. The valuation is slightly lower than in our previous report, which modelled a launch one year earlier, in 2023. Our valuation is equivalent to $16.50/ADR and $15.85/ADR after diluting for options and convertible notes. Kazia’s primary listing is on the ASX under the code KZA; each NASDAQ-listed ADR represents 10 ordinary shares. Our undiluted base case valuation equals A$2.17 per ASX-listed ordinary share at current exchange rates.

Our base case valuation assumes a 40% likelihood that GDC-0084 is out-licensed to a marketing partner in 2023 after reporting positive PFS data from the Phase IIb trial in a deal that includes $40m upfront and $120m in clinical and regulatory milestone payments. We also assume Kazia pays a royalty of 10% of net sales to Genentech and that global sales for GBM reach $1,050m in 2030.

Exhibit 11 shows our base case market assumptions for GDC-0084 and Cantrixil and the contribution of product royalties and milestone payments to the rNPV. We have offset the risk-adjusted trial cost against milestone revenue for each drug, rather than against royalty revenue. This understates the contribution of the milestone payments to the rNPV and overstates the contribution of royalties.

Exhibit 11: Kazia base case valuation (assumes approval after a single GDC-0084 pivotal trial)

|

Likelihood (%) |

rNPV ($m) |

rNPV/

ADR ($) |

Assumptions |

GDC-0084; GBM |

25% |

40.2 |

6.46 |

Global peak sales* of $1,050m from GBM (11,500 US cases/year, 61% unmethylated MGMT** promoter, 80% penetration); pricing of $50k. Global sales 2x US sales; launch 2026; assumes receives 20% royalty on sales, pays away 10% royalty to Genentech. |

GDC-0084; brain metastases in HER2+ breast cancer |

20% |

11.7 |

1.88 |

Global peak sales of $600m (233,000 US breast cancer cases/year, 37% HER2+, 7% develop brain metastases, 50% penetration); pricing of $50k. Global sales 2x US sales; launch 2026; assumes receives 20% royalty on sales, pays away 10% royalty to Genentech. |

GDC-0084; DIPG |

20% |

0.9 |

0.14 |

Global peak sales of $45m (275 US DIPG cases/year, 80% penetration); pricing of $50k. Global sales 2x US sales; launch 2026; assumes receives 20% royalty on sales, pays away 10% of royalty to Genentech. |

Ovarian and other abdominal cancers: Cantrixil |

10% |

22.2 |

3.57 |

Global peak sales of $680m from ovarian cancer (14,300 US deaths/year, 30% penetration) and bowel cancer (50,300 US deaths, 25% develop malignant ascites, 20% penetration); pricing of $50k. Global sales 2x US sales; launch 2025; assumes receives 15% royalty on sales, pays away 5% of revenue to Yale. |

GDC-0084 milestones |

|

18.6 |

2.99 |

Assumes potential licensing upfronts and milestones total $160m ($147m net of payments to Glioblast and Genentech; $48m after risk adjustment). |

Cantrixil milestones |

|

15.8 |

2.55 |

Assumes potential licensing upfronts and milestones total $140m ($23m after risk adjustment); assumes 5% of upfront and milestone payments paid away to Yale. |

SG&A |

|

-9.2 |

-1.49 |

|

Portfolio total |

|

100.1 |

16.10 |

|

Noxopharm options book value |

|

0.2 |

0.02 |

|

Net cash at end FY19e |

|

2.4 |

0.38 |

|

Enterprise total |

|

102.6 |

16.50 |

|

Source: Edison Investment Research. Note: *Peak sales in actual dollars in forecast year. **MGMT: methylguanine-DNA methyltransferase gene. We assume the addressable markets grow at 4% per year. Launch dates listed are calendar years (in some cases the launch will be in the financial year following the calendar year stated).

We have also valued Kazia under an alternative accelerated approval scenario for GDC-0084, which assumes a market launch in 2026 and that Kazia receives a lower 15% royalty rate and a smaller $20m upfront payment due to the need for the partner to complete an confirmatory efficacy study before filing for approval, with other deal terms the same as for the accelerated approval base case scenario. Exhibit 12 shows that requirement for a confirmatory pivotal study for GDC-0084 would reduce our valuation for Kazia to $64m or $10.27/ADR (undiluted).

Exhibit 12: Kazia alternative valuation scenario (assumes confirmatory GDC-0084 pivotal trial required)

|

Likelihood (%) |

rNPV ($m) |

rNPV/

ADR ($) |

Assumptions |

GDC-0084 – GBM |

25% |

13.8 |

2.22 |

As per Exhibit 11, except 2026 launch (vs 2024) and 15% gross royalty on sales (vs 20%). |

GDC-0084 – brain metastases in HER2+ breast cancer |

20% |

5.8 |

0.94 |

As per Exhibit 11, except 15% gross royalty on sales (vs 20%). |

GDC-0084; DIPG |

20% |

0.4 |

0.07 |

As per Exhibit 11, except 15% gross royalty on sales (vs 20%). |

GDC-0084 milestones |

|

14.4 |

2.31 |

Assumes potential licensing upfronts and milestones total $140m ($127m net of payments to Glioblast and Genentech; $38m after risk adjustment). Milestones received later than base case (final milestone in 2026 vs 2024). |

GDC-0084 total |

|

34.5 |

5.54 |

|

Remainder of portfolio |

|

26.9 |

4.32 |

|

Portfolio total |

|

61.3 |

9.87 |

|

Noxopharm options book value |

|

0.2 |

0.02 |

|

Net cash at end FY19e |

|

2.4 |

0.38 |

|

Enterprise total |

|

63.9 |

10.27 |

|

Source: Edison Investment Research. Note: Launch dates listed are calendar years.

Kazia had $4.1m cash plus an $2.2m R&D tax rebate receivable at 31 December 2018. It has subsequently raised $1.8m (before costs) through the sale of its shareholding in Noxopharm. We expect the available funds to be sufficient to support operations into H2 CY19. While the preliminary efficacy data from the GDC-0084 Phase IIa study are expected to read out in Q419, depending on the timing, funds may need to be raised in H2 CY19 before the trial data are available. We estimate Kazia will need additional funds of $11–15m to finance the GDC-0084 Phase IIb GBM study.

We have revised our FY20 financial forecasts to include an $0.2m contribution to the Alliance collaborative study, plus a further $0.2m contribution in FY21.

Exhibit 13: Financial summary

|

|

US$000s |

2016 |

2017 |

2018 |

2019e |

2020e |

Year end 30 June |

|

|

AASB |

AASB |

AASB |

AASB |

AASB |

PROFIT & LOSS |

|

|

|

|

|

|

|

Sales, royalties, milestones |

|

|

0 |

0 |

0 |

0 |

0 |

Other (includes R&D tax rebate) |

|

|

2,786 |

6,508 |

9,872 |

2,336 |

2,372 |

Revenue |

|

|

2,786 |

6,508 |

9,872 |

2,336 |

2,372 |

R&D expenses |

|

|

(7,519) |

(8,463) |

(7,428) |

(6,998) |

(7,382) |

SG&A expenses |

|

|

(3,301) |

(5,761) |

(6,181) |

(3,300) |

(3,563) |

Other |

|

|

0 |

0 |

0 |

0 |

0 |

EBITDA |

|

|

(8,034) |

(7,716) |

(3,737) |

(7,961) |

(8,573) |

Operating Profit (before GW and except.) |

|

|

(8,110) |

(7,806) |

(3,897) |

(7,961) |

(8,573) |

Intangible Amortization |

|

|

(1,003) |

(62) |

(1,016) |

(1,108) |

(997) |

Exceptionals |

|

|

(432) |

0 |

0 |

0 |

0 |

Operating Profit |

|

|

(9,546) |

(7,868) |

(4,912) |

(9,069) |

(9,570) |

Net Interest |

|

|

308 |

(392) |

91 |

45 |

24 |

Pre-Tax Profit (norm) |

|

|

(8,805) |

(8,260) |

(4,822) |

(10,544) |

(9,546) |

Pre-Tax Profit (reported) |

|

|

(9,237) |

(8,260) |

(4,822) |

(9,024) |

(9,546) |

Tax benefit |

|

|

0 |

151 |

232 |

0 |

0 |

Profit After Tax (norm) |

|

|

(8,805) |

(8,109) |

(4,590) |

(10,544) |

(9,546) |

Profit After Tax (reported) |

|

|

(9,237) |

(8,109) |

(4,590) |

(9,024) |

(9,546) |

|

|

|

|

|

|

|

|

Average Number of Shares Outstanding (m) |

|

|

42.7 |

46.8 |

48.4 |

55.3 |

62.2 |

Average Number of ADRs Outstanding (m) |

|

|

4.27 |

4.68 |

4.84 |

5.53 |

6.22 |

EPS - normalized (c) |

|

|

(21.61) |

(17.33) |

(9.49) |

(19.07) |

(15.36) |

EPS - diluted |

|

|

(21.61) |

(17.33) |

(9.49) |

(19.07) |

(15.36) |

Dividend per share (c) |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Earnings per ADR - normalized (c) |

|

|

(216.1) |

(173.3) |

(94.9) |

(190.7) |

(153.6) |

Earnings per ADR - diluted (c) |

|

|

(216.1) |

(173.3) |

(94.9) |

(190.7) |

(153.6) |

Dividend per ADR (c) |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

|

|

|

|

|

|

|

|

BALANCE SHEET |

|

|

|

|

|

|

|

Fixed Assets |

|

|

1,084 |

12,487 |

14,376 |

10,132 |

9,211 |

Intangible Assets |

|

|

625 |

12,098 |

11,080 |

9,972 |

8,975 |

Tangible Assets |

|

|

450 |

372 |

1 |

1 |

77 |

Investments |

|

|

10 |

17 |

3,295 |

160 |

160 |

Current Assets |

|

|

25,908 |

14,805 |

7,037 |

5,415 |

3,334 |

Stocks |

|

|

0 |

0 |

0 |

0 |

0 |

Debtors |

|

|

151 |

3,240 |

1,927 |

2,470 |

2,502 |

Cash |

|

|

25,424 |

10,986 |

4,527 |

2,361 |

248 |

Other |

|

|

333 |

580 |

584 |

584 |

584 |

Current Liabilities |

|

|

(1,088) |

(4,092) |

(2,955) |

(4,054) |

(4,188) |

Creditors |

|

|

(988) |

(1,423) |

(1,571) |

(2,670) |

(2,804) |

Short term borrowings |

|

|

0 |

0 |

0 |

0 |

0 |

Other |

|

|

(100) |

(2,669) |

(1,384) |

(1,384) |

(1,384) |

Long Term Liabilities |

|

|

(117) |

(3,943) |

(3,835) |

(3,918) |

(9,998) |

Long term borrowings |

|

|

0 |

0 |

0 |

0 |

(6,080) |

Other long-term liabilities |

|

|

(117) |

(3,943) |

(3,835) |

(3,918) |

(3,918) |

Net Assets |

|

|

25,788 |

19,257 |

14,624 |

7,575 |

(1,641) |

|

|

|

|

|

|

|

|

CASH FLOW |

|

|

|

|

|

|

|

Operating Cash Flow |

|

|

(9,411) |

(8,879) |

(6,673) |

(7,086) |

(8,140) |

Net Interest |

|

|

308 |

189 |

91 |

45 |

24 |

Tax |

|

|

0 |

0 |

0 |

0 |

0 |

Capex |

|

|

(399) |

(15) |

0 |

(76) |

(76) |

Acquisitions/disposals |

|

|

2 |

(5,394) |

114 |

1,775 |

0 |

Equity Financing |

|

|

594 |

(13) |

0 |

3,177 |

0 |

Dividends |

|

|

0 |

0 |

0 |

0 |

0 |

Other |

|

|

0 |

0 |

0 |

0 |

0 |

Net Cash Flow |

|

|

(8,906) |

(14,113) |

(6,469) |

(2,166) |

(8,193) |

Opening net debt/(cash) |

|

|

(33,722) |

(25,424) |

(10,986) |

(4,527) |

(2,361) |

HP finance leases initiated |

|

|

0 |

0 |

0 |

0 |

0 |

Other |

|

|

608 |

(326) |

10 |

0 |

0 |

Closing net debt/(cash) |

|

|

(25,424) |

(10,986) |

(4,527) |

(2,361) |

5,832 |

Source: Kazia Therapeutics accounts, Edison Investment Research. Note: Solely for the convenience of the reader the financial summary table has been converted at a rate of US$0.76 to A$1. Novogen reports statutory accounts in Australian dollars. These translations should not be considered representations that any such amounts have been or could be converted into US dollars at the assumed conversion rate.

Contact details |

Revenue by geography |

Level 24

Three International Towers

300 Barangaroo Ave

Sydney, NSW

Australia

Tel: +61 2 9472 4101

www.kaziatherapeutics.com |

N/A |

Contact details |

Level 24

Three International Towers

300 Barangaroo Ave

Sydney, NSW

Australia

Tel: +61 2 9472 4101

www.kaziatherapeutics.com |

Revenue by geography |

N/A |

Management team |

|

CEO: Dr James Garner |

Chairman: Iain Ross |

Dr Garner is an experienced life sciences executive who has previously worked with companies ranging from small biotechs to multinational pharmaceutical companies such as Biogen and Takeda. His career has focused on regional and global development of new medicines from preclinical to commercialization. Dr Garner is a physician by training and holds an MBA from the University of Queensland. He began his career in hospital medicine and worked for a number of years as a corporate strategy consultant with Bain & Company before entering the pharmaceutical industry. Prior to joining Kazia in 2016, he led R&D strategy for Sanofi in Asia-Pacific and was based in Singapore. |

Iain has held senior positions in Sandoz, Fisons, Hoffmann-La Roche and Celltech Group and also undertaken a number of start-ups and turnarounds on behalf of banks and private equity groups. His track record includes multiple financing transactions having raised in excess of £300m, both publicly and privately, as well as extensive experience of divestments and strategic restructurings. He has over 20 years’ experience in cross-border management as a chairman and CEO. He is chairman of e-Therapeutics (LSE:ETX), Redx Pharma (LON:REDX) and Biomer Technology. |

Principal shareholders at June 2017 |

(%) |

HSBC Custody Nominees |

35.1 |

Hishenk Pty Ltd plus HiShenk |

13.8 |

|

Companies named in this report |

Roche, Bayer, Novartis, Gilead Sciences, Verastem |

|

General disclaimer and copyright This report has been commissioned by Kazia Therapeutics and prepared and issued by Edison, in consideration of a fee payable by Kazia Therapeutics. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2019 Edison Investment Research Limited (Edison). All rights reserved FTSE International Limited (“FTSE”) © FTSE 2019. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Myonlineadvisers Pty Ltd who holds an Australian Financial Services Licence (Number: 427484). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument.

New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States The Investment Research is a publication distributed in the United States by Edison Investment Research, Inc. Edison Investment Research, Inc. is registered as an investment adviser with the Securities and Exchange Commission. Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|

General disclaimer and copyright This report has been commissioned by Kazia Therapeutics and prepared and issued by Edison, in consideration of a fee payable by Kazia Therapeutics. Edison Investment Research standard fees are £49,500 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2019 Edison Investment Research Limited (Edison). All rights reserved FTSE International Limited (“FTSE”) © FTSE 2019. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Myonlineadvisers Pty Ltd who holds an Australian Financial Services Licence (Number: 427484). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument.

New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States The Investment Research is a publication distributed in the United States by Edison Investment Research, Inc. Edison Investment Research, Inc. is registered as an investment adviser with the Securities and Exchange Commission. Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 1,185 Avenue of the Americas 3rd Floor, New York, NY 10036 United States of America |

Sydney +61 (0)2 8249 8342 Level 4, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

|