Company description: One-stop shop

Ernst Russ (ERAG) is a listed asset and investment manager with a focus on shipping assets. The maritime asset management activities provide a complete range of services including technical and commercial ship management, which ERAG provides to a fleet of c 180 vessels. The fleet includes 140 vessels controlled by ERAG closed-end funds or structures as well as vessels managed on behalf of third-party ship owners/operators. Its asset and investment management activities include approximately 200 active funds with invested equity of c €3bn and, allowing for gearing within the funds, an investment volume (assets under management, AUM) of more than €6.5bn (AUM is the sum of €3bn equity raised plus associated debt). The group in its current form is the product of a three-way combination in 2016 that merged König & Cie (the terms of which have not been disclosed), a provider of institutional focused ship asset and investment management services, and the ship owner and operator Ernst Russ Reederei, into the former HCI Group, whose roots were in initiating and issuing retail focused closed-end ship funds via banks and other intermediaries. The group also boosted its real estate asset management scale and capabilities with the acquisition of WestFonds (terms also not disclosed). The significant strategic repositioning of the group is aimed at restoring it to a growth path after the challenges of recent years, brought about by the collapse of closed-end fund issuance since the global financial crisis as a result of market conditions and regulatory changes.

Exhibit 1: Breakdown of total AUM

|

Exhibit 2: Five-year summary of revenues and EBT

|

|

|

|

|

Source: ERAG. Note: EBT stands for earnings before tax.

|

Exhibit 1: Breakdown of total AUM

|

|

|

|

Exhibit 2: Five-year summary of revenues and EBT

|

|

Source: ERAG. Note: EBT stands for earnings before tax.

|

The newly formed group has adopted a ‘three pillar’ business strategy that provides a full range of investment fund services including asset sourcing, fund initiation and distribution; a full range of asset management services; and investor/trustee services, an approach that the group refers to as “a one-stop shop”:

■

Asset management: the financial and strategic management of funds and complex investment structures, primarily for ships but also real estate and other alternative assets such as structured products, private equity and renewable energy.

■

Ship management: a full range of shipping services including technical management (eg crewing) and commercial management (eg chartering) for in-house and third-party controlled vessels.

■

Investor management: equity raisings with capital market access in Germany and the UK, distribution of retail and institutional alternative investment funds and the administration of funds and related activities. While ship and asset management are dealing with the financial and operational side of the asset, investor management is essentially providing the investor with information materials on the asset, annual reports and meetings.

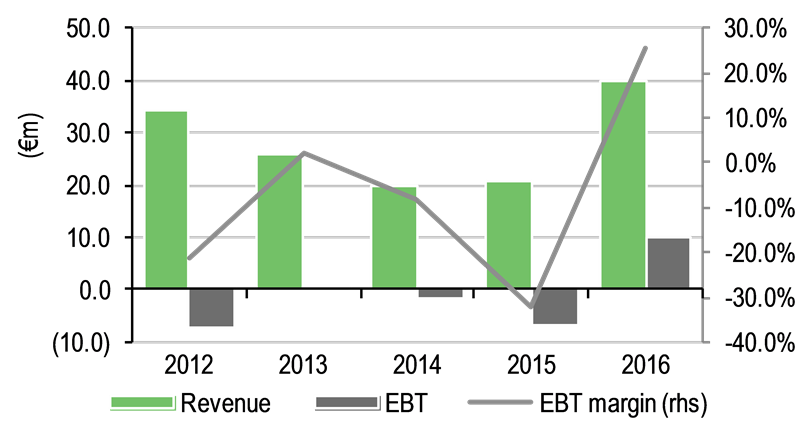

Revenues and profits both showed a material increase in 2016 as a result of the first time consolidation of the newly acquired businesses (Exhibit 2), while the 2016 revenue split shows a significant shift towards ship management and asset management. A full year contribution from the acquired business is expected to further increase these revenues in 2017.

Exhibit 3: Revenue mix 2016

|

Exhibit 4: Revenue mix 2015

|

|

|

|

|

|

Exhibit 3: Revenue mix 2016

|

|

|

|

Exhibit 4: Revenue mix 2015

|

|

|

|

A brief history of strategic development

ERAG has been built around HCI Capital AG, which was founded in 1985 as an issuer of ship fund investments primarily to retail investors, and listed in 2005. HCI grew rapidly to become a leading issuance house and expanded its business to include further asset classes such as property, private equity and alternatives. Since it was founded it has issued more than 500 funds and raised an aggregate c €6bn in equity to support, with fund debt, an aggregate initial investment volume of c €15bn. HCI focused on identifying suitable investment assets and bringing them together with investors by creating, structuring, and arranging financing for investment vehicles with a strong focus on equity issuance to retail investors through partners such as banks and IFAs (Independent Financial Advisers). Asset management in this context included the financial and strategic management of the assets, exercised by managing partner positions within the closed-end limited liability (KG) fund structures, but did not extend to the operational management of the assets, primarily ships. The financial model was highly dependent on high upfront issuance fees with a more modest contribution from recurring fees based on asset management and fund administration, including investor fiduciary/trustee services. Along with other issuers of closed-end funds in Germany, HCI was hit hard by the global financial crisis and its effects on global growth and the shipping sector in particular. The crisis brought issuance activity to an abrupt halt and in its aftermath, changed market conditions and a new regulatory framework meant the old model was no longer successful.

Exhibit 5: Long-term revenue trends (€000s)

|

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

Distribution & origination |

105,358 |

92,187 |

18,136 |

9,256 |

6,301 |

7,604 |

4,000 |

49 |

0 |

0 |

Ship management/asset management |

1,823 |

2,724 |

5,909 |

5,297 |

7,815 |

7,474 |

4,645 |

4,422 |

4,249 |

20,767 |

Investor management |

22,631 |

22,682 |

21,391 |

21,834 |

19,027 |

18,899 |

17,107 |

15,212 |

14,516 |

16,789 |

Chartering services |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

1,937 |

835 |

Other |

7,487 |

2,370 |

73 |

375 |

17 |

153 |

0 |

0 |

15 |

1,564 |

Total revenues |

137,299 |

119,963 |

45,509 |

36,762 |

33,160 |

34,130 |

25,752 |

19,683 |

20,717 |

39,955 |

% change |

|

-13% |

-62% |

-19% |

-10% |

3% |

-25% |

-24% |

5% |

93% |

Source: ERAG, Edison Investment Research

HCI initially focused on preserving the fund base that it had built up and the fiduciary services revenues that these would generate, and gaining regulatory approval as an Alternative Investment Fund Manager (AIFM), while seeking ways to capture more of the asset management value chain by broadening its competence in technical and operational shipping management in particular. At the same time, HCI set about diversifying its distribution and with demand from retail investors severely depressed it began building up its institutional investor and semi-professional investor relationships. During 2015 the group acquired its first container ship as a proprietary investment and decided, together with other experienced partners, to acquire further ship assets and finance them through joint venture structures managed by the group. The container ship was sold with a profit of c €500k at the beginning of 2016. ERAG currently controls and manages 13 ships through these structures in a JV.

The first major realignment of the group came in early 2016 with the acquisition of 90% of König & Cie in January 2016, which enabled the group to offer a complete range of ship management services, in particular technical and commercial management, while increasing its scale in asset and investor management. The acquisition of the long established shipping company Ernst Russ Reederei completed the group’s ability to provide a full range of ship management services.

The group was repositioned primarily as a maritime asset and investment manager and changed its name from HCI to Ernst Russ.

The business platform and model

ERAG divides its services into asset, ship and investor management. The ship management business is responsible for the operational support of the ships bought by investors through the closed-end funds originated by investor management, while the asset management unit runs the financial management of these funds. Administration and reporting of the closed-end funds is the task of the investor management unit, which could also include certain distribution functions. ERAG also offers these services for other asset classes, such as real estate, alternative investments and PE in particular.

Exhibit 6 summarises the group’s business model: its fully integrated ‘one-stop shop’ concept covers all aspects of the value chain.

Exhibit 6: ERAG’s business model

|

|

|

|

Before discussing the operating units that support the three pillars of the group’s strategy, it is worth considering the business strategy from an economic viewpoint. The group is involved at all stages of the investment process (for ships, real estate and other asset classes), beginning with the identification and sourcing of suitable assets, structuring them into an investment proposition (eg an AIF, or some other complex structure), and then arranging finance including equity investment from investors and partners as well as debt. The historical focus was on closed-end (KG) funds, the bulk of the current AUM, and for which the group provides trustee services (investor management) on behalf of the investors, generating a significant, but declining, fee stream over the remaining life of the funds, which management hopes to partly offset by providing similar services to third parties. ERAG’s intention is to replace these maturing legacy assets with new funds, AIFs and other complex institutional products, generating a higher level of fee revenue from a deeper participation in the management of the assets. This deeper participation is most evident in shipping, where the group can now provide a full range of ship management services in-house, but also in real estate where the WestFonds acquisition has added scale and breadth. Ship management is itself a pillar of strategy, given its significance and the fact that it is provided to ‘in-house’ funds and structures and external third-parties alike.

Exhibit 7: Ernst Russ– income structure

|

|

Source: Edison Investment Research

|

As we show in Exhibit 3, ERAG now reports ship management and asset management revenues as a block, and investor management revenues separately.

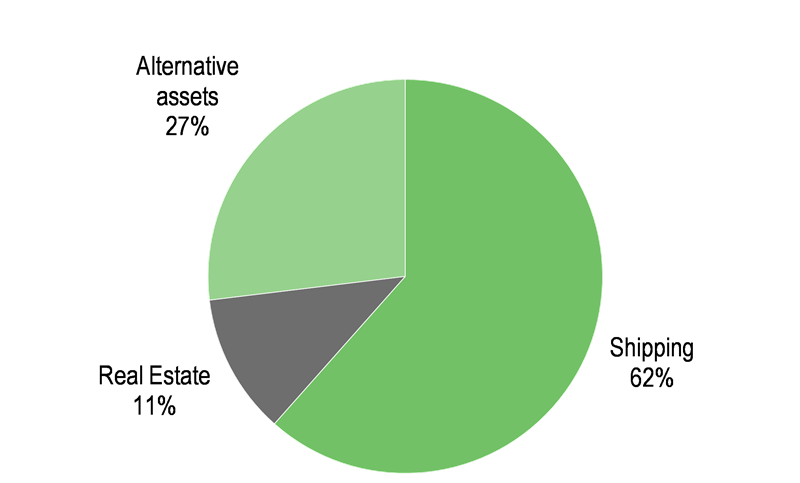

The group’s asset management activities in the maritime sector have all been grouped under Ernst Russ Maritime Management (ERMM), providing a full range of services to c 110 active shipping funds and structured investments managed by the group with an investment volume of c €4.0bn, as well as around 40 vessels owned by third-party ship owners/operators.

Assetando Real Estate is similarly positioned to provide a full range of real estate investment services, although it does not extend to the technical management of individual properties. AUM has grown to c €750m including c €540m of funds acquired with WestFonds.

HCAM is responsible for the group’s alternative assets under management including c $350m in structured funds managed through an umbrella structure in nearly 50 partner funds. There are also 15 funds invested in German and UK traded life assurance funds with an AUM of close to €600m, as well investments in solar parks, aircraft, private equity and infrastructure.

Since 2015, HCV Hanseatische Capital Verwaltung has been the fully authorised asset manager for the group (the KVG – fully licensed capital administration company), which allows it to issue closed-end domestic public AIFs (aimed at individual investors) and special AIFs directed at institutional investors. Additionally, since 2016 the group has partnered with Pareto Securities AS, a leading full service investment bank from Norway, to design and offer structured products for institutional investors, including debt products.

The group’s existing trust company activities and those acquired from König & Cie have all been grouped together under PECURA Anleger und Treuhandservice GmbH, which offers trustee services for a total of 12 internal and external trust companies. PECURA manages 200,000 closed-end fund certificates for more than 140,000 clients. The fiduciary fees that are earned on the majority of the existing limited partnership closed-end funds are long-term in nature, recurring annually (on the equity participation of investors or ‘managed trust capital’) over the life of those funds. ERAG continues to support the funds and safeguard the revenue stream, and particularly in the area of shipping funds, restructuring teams work with the funds and the banks to provide solutions for those funds that are stressed by the continuing weak shipping markets. Managed trust capital increased during 2016, from c €3.1bn to c €3.6bn. The increase is attributable to the acquisition of König & Cie, which added c €1.3bn, while fund insolvencies and asset realisations continued to erode the underlying position. PECURA has invested in digitalising its processes with the aim of successfully competing for external contracts that will help to offset the run-off of internal KG funds.

Conditions in the international shipping markets are obviously a key sensitivity for the business, with an impact on fee revenues from ship services, investor and asset management, as well as the value of investments and, potentially, receivables values. The protracted weakness in the shipping market, with oversupply and fierce competition a persistent feature, continued through 2016, and in particular in the container, bulker (unpackaged bulk cargo, eg coal), and product tanker (refined products) areas that are most relevant to ERAG. Summarising ERAG’s comments from the 2016 annual report, which cite industry data from Clarkson, a shipping industry research firm, container demand grew modestly but not enough to absorb available capacity and time charter rates were at similar low levels to 2009. With older ships being scrapped, bulker capacity growth slowed to the lowest level for many years, but still exceeded demand growth. The Baltic Dry Index (BDI), a price index for bulk dry goods, has continued to show characteristic volatility, falling from a 2015 high of c 1,200 in August 2015 to a year’s low of 688 in February before recovering to a 2016 high of 1,257 in November. We note that it has recently been quoted in the 800-850 range. Fleet growth in product tankers also exceeded demand growth. The Baltic Clean Tanker Index (BCTI), a key industry index, also fluctuated significantly through 2016 and into 2017; increasing from 535 to a high of 716 in early 2016, falling back to 352 by September before rallying to 678 at the end of the year. We note it has recently been quoted at around the 550 level.

ERAG management anticipates that ongoing consolidation among ship owners will support a reduction in the supply surplus and help to restore balance to the market over time. The group is now positioned to benefit significantly from any upturn, both in the areas of asset management and shipping services. Meanwhile, in cooperation with Pareto it seeks opportunities to provide corporate finance advice to shipping owners and operators.

The prospects for new fund launches remains relatively muted although economic improvement and continued low interest rates are creating more optimism. Changes in regulation and the market environment mean that new issuance of the traditional KG limited partnership closed-end funds is extremely challenging. However, there are signs that the global recovery and continued low interest rates may begin to stimulate retail interest in closed AIFs. A survey in January 2017 by the Federal Association of Property and Investment Assets (the BSI e.V) found that 60% of capital management companies consider the prospects for closed public AIF issuance as good or very good. The survey pointed to an estimated planned investment activity of c €1.4bn, focused on real estate. With its partnership with Pareto, ERAG seeks to launch institutionally focused products such as Special AIFs and other capital markets products including bonds. Management seeks opportunities in both shipping and German real estate, where demand from both private and institutional investors continues to be supported by a stable economy, rising employment and the continued low interest rate environment.

Management, corporate governance and shareholders

The ERAG management board has considerable industry and commercial experience. CEO Jens Mahnke joined the group through the acquisition of König & Cie, where he had also held the position of CEO since 2008. He brings strong industry experience to ERAG, having worked in the shipping industry, including a number of senior positions, for more than 25 years. The CFO is Ingo Kuhlmann, who joined the group through HCI in 2008, joining the board in 2012. The third member of the management board is David Landgrebe, who joined the group in June 2013 from Peter Döhle Schiffahrts-KG. He has previously worked at HSH Nordbank, a historically significant maritime lender, including four years as restructuring director, and has experience in real estate.

As a listed German company, ERAG is overseen by a supervisory board of four members, chaired by Alexander Stuhlmann. The other members of the supervisory board are Jochen Thomas Döhle, Robert Lorenz-Meyer and Robert Gärtner.

Shareholders and free float

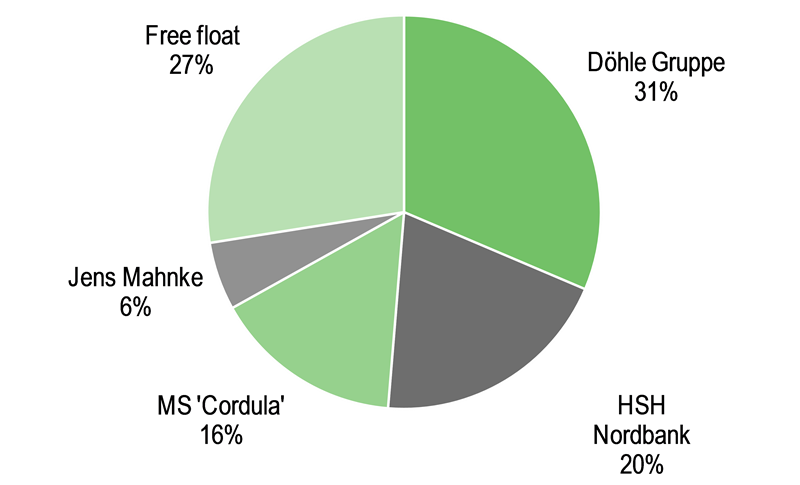

The main driver of the changes in the shareholder structure during 2016 was the issue of 6.2m new shares (24% of the total outstanding before the issue, increasing equity by c €9.5m and equivalent to €1.53 per share) as payment to the previous owners of Ernst Russ Reederei, Döhle Group, the Hamburg-based ship operator and shipping services group, and MS Cordula, also Hamburg based. HSH Nordbank is currently a 16% shareholder. The bank is owned by the states of Hamburg and Schleswig-Holstein, which are required to sell the bank by 28 February 2018. Both Döhle Group and MS Cordula were already shareholders in the group (as HCI). The free float is now 35%.

Exhibit 8: Recent shareholder structure

|

Exhibit 9: 2015 shareholder structure

|

|

|

|

|

|

Exhibit 8: Recent shareholder structure

|

|

|

|

Exhibit 9: 2015 shareholder structure

|

|

|

|

ERAG reports under German GAAP (the German HGB code). The acquisitions, König & Cie, Ernst Russ Reederei and WestFonds, are all consolidated in the 2016 accounts for the first time and have a significant impact on the group assets, earnings and cash position. We provide a summary in Exhibit 10, which shows both the year-on-year changes and the half-yearly development over the period. Reported 2016 revenues increased 93% to c €40m with net attributable profit reaching €6.2m (2015: €1.0m). On the balance sheet, total assets increased 71% to €103m and net assets increased to €39m (equity assets ratio is 37.3% compared with 35.5% in 2015). The closing cash position was €28m or €16.1m net of consolidated debt as the company has just €12.2m in bank debt.

Exhibit 10: Financial summary

Year to 31 December (€000s) |

2015 |

2016 |

|

H115 |

H215 |

H116 |

H216 |

|

HGB |

HGB |

|

HGB |

HGB |

HGB |

HGB |

INCOME STATEMENT |

|

|

|

|

|

|

|

Ship management/asset management |

4,249 |

20,767 |

|

|

|

|

|

Investor management |

14,516 |

16,789 |

|

|

|

|

|

Chartering services |

1,937 |

835 |

|

|

|

|

|

Other |

15 |

1,564 |

|

|

|

|

|

Total revenue |

20,717 |

39,955 |

|

9,952 |

10,765 |

17,029 |

22,926 |

Change in work in progress |

0 |

(119) |

|

0 |

0 |

0 |

(119) |

Other operating income |

8,310 |

34,969 |

|

3,428 |

4,882 |

11,989 |

22,980 |

Cost of materials/purchased services |

(1,632) |

(6,126) |

|

(579) |

(1,053) |

(2,852) |

(3,274) |

Personnel expenses |

(9,130) |

(20,578) |

|

(4,625) |

(4,505) |

(7,791) |

(12,787) |

Depreciation & amortisation |

(1,010) |

(7,862) |

|

(334) |

(676) |

(3,445) |

(4,417) |

Other operating expenses |

(20,886) |

(20,619) |

|

(6,800) |

(14,086) |

(10,182) |

(10,437) |

Operating profit |

(3,631) |

19,620 |

|

1,042 |

(4,673) |

4,748 |

14,872 |

Income from equity investments |

506 |

976 |

|

117 |

389 |

1,633 |

(657) |

Other interest & similar income |

1,000 |

2,189 |

|

378 |

622 |

1,185 |

1,004 |

Write-downs on financial assets |

(3,064) |

(7,557) |

|

(214) |

(2,850) |

(4,869) |

(2,688) |

Interest & similar expenses |

(1,194) |

(1,064) |

|

(406) |

(788) |

(531) |

(533) |

Share of profit of associates |

(270) |

(3,990) |

|

0 |

(270) |

89 |

(4,079) |

Earnings before tax |

(6,653) |

10,174 |

|

917 |

(7,570) |

2,255 |

7,919 |

EBT margin |

-32.1% |

25.5% |

|

9.2% |

-70.3% |

13.2% |

34.5% |

Tax |

7,627 |

(3,791) |

|

25 |

7,602 |

(1,419) |

(2,372) |

Consolidated net profit |

974 |

6,383 |

|

942 |

32 |

836 |

5,547 |

Non-controlling interest |

0 |

(157) |

|

0 |

0 |

(8) |

(149) |

Consolidated attributable net profit |

974 |

6,226 |

|

942 |

32 |

828 |

5,398 |

EPS (€) |

0.04 |

0.20 |

|

0.04 |

0.00 |

0.03 |

0,17 |

BALANCE SHEET |

|

|

|

|

|

|

|

Financial assets |

21,992 |

22,387 |

|

25,673 |

21,992 |

30,009 |

22,387 |

Intangible assets |

287 |

25,431 |

|

320 |

287 |

26,194 |

25,431 |

Property, plant & equipment |

5,702 |

456 |

|

5,917 |

5,702 |

424 |

456 |

Cash & equivalents |

12,775 |

28,273 |

|

11,995 |

12,775 |

12,110 |

28,273 |

Other current assets |

19,600 |

26,932 |

|

16,556 |

19,600 |

21,608 |

26,932 |

Total assets |

60,356 |

103,479 |

|

60,461 |

60,356 |

90,345 |

103,479 |

Financial liabilities |

(18,590) |

(12,167) |

|

(18,250) |

(18,590) |

(9,275) |

(12,167) |

Other liabilities |

(20,456) |

(52,727) |

|

(20,957) |

(20,456) |

(49,464) |

(52,727) |

Minorities |

0 |

(623) |

|

0 |

0 |

(1) |

(623) |

Shareholders' equity |

21,310 |

37,962 |

|

21,254 |

21,310 |

31,605 |

37,962 |

CASH FLOW |

|

|

|

|

|

|

|

Cash flow from operating activity |

379 |

4,584 |

|

367 |

12 |

5,048 |

(464) |

Cash from investing activity |

(8,973) |

14,333 |

|

(9,720) |

747 |

(4,228) |

18,561 |

Cash flow from financing activity |

(93) |

(3,342) |

|

36 |

(129) |

(1,339) |

(2,003) |

Other |

1,149 |

(77) |

|

1,000 |

149 |

(146) |

69 |

Net change in cash |

(7,538) |

15,498 |

|

(8,317) |

779 |

(665) |

16,163 |

Closing cash |

12,775 |

28,273 |

|

11,996 |

12,775 |

12,110 |

28,273 |

Closing net cash/(debt) |

(5,815) |

16,106 |

|

(6,254) |

(5,815) |

2,835 |

16,106 |

Source: ERAG. Note: HGB = German GAAP.

Exhibit 11: Effect of acquisitions on end 2016 balance sheet and 2016 P&L

2016 balance sheet effects, €000s |

König & Cie |

Ernst Russ Reederei |

WestFonds |

Total |

Goodwill |

4,256 |

2,966 |

0 |

7,222 |

Value of service contracts |

14,690 |

1,125 |

0 |

15,815 |

Financial assets |

1,619 |

5,392 |

1,584 |

8,595 |

Stocks |

0 |

0 |

7,664 |

7,664 |

Cash |

3,803 |

1,535 |

10,306 |

15,644 |

Difference arising from capital consolidation |

0 |

0 |

7,528 |

7,528 |

Pension provision |

0 |

(1,941) |

0 |

(1,941) |

Other provisions |

(3,829) |

(387) |

(6,141) |

(10,357) |

Debt |

(2,872) |

0 |

(7,350) |

(10,222) |

2016 P&L effects, €000s |

|

|

|

|

Revenues |

12,433 |

8,036 |

1,712 |

22,181 |

Cost of materials/purchased services |

(3,179) |

(1,619) |

(140) |

(4,938) |

Personnel costs |

(3,059) |

(5,466) |

(1,366) |

(9,891) |

Other operating expenses |

(2,667) |

(586) |

(399) |

(3,652) |

Interest & similar expense |

(438) |

|

(84) |

(522) |

In Exhibit 11 we show the details provided by ERAG on the 2016 impact of the three acquisitions. There will be further impacts on underlying earnings in 2017 as the acquisitions have a full year impact: full consolidation of König & Cie took effect on 31 January 2016 so it made a c 11-month contribution; Ernst Russ (30 April 2016) contributed c eight months; and WestFonds (31 July 2016) contributed almost five months. In aggregate, the acquisitions added €22.2m to 2016 revenues. Revenues from existing businesses appear to have declined from €20.7m in 2015 to €17.8m mainly due to asset sales, such as the container ship in early 2016.

The data provided by ERAG imply an EBT contribution from the acquisitions of c €3.2m, leaving c €7.0m for the existing business. While acquisitions added c €55m in total assets, assets from the existing business declined by around c €12m, which was largely related to depreciation and asset disposals. The acquisitions added €31.6m in long-term assets, including €7.2m goodwill, €15.8m in capitalised business contracts, and €8.6m in financial assets. The impact on group cash flow was strongly positive with an aggregate €15.6m in cash, largely due to WestFonds.

In addition to retained profits, shareholder equity increased by €9.5m with the issue of 6.2m new shares (taking the total to 32.4m) as payment in kind for Ernst Russ Reederei.

In addition to the significant changes in the financial statements that result from the acquisitions, the 2016 results also include some material non-recurring items. Other operating income increased by €26.7m, which management indicates was primarily the result of the write-back of provisions and the booking of income from loan settlements of €13.3m. During the year ERAG successfully concluded an agreement with banks that settled ERAG’s end 2015 liability of €12.5m in return for a cash payment of €2.5m, generating €9.0m in other operating income in the process. A similar transaction involving the successor to the Wölbern bank reduced the end 2015 liability of c €6.0m to c €2.0m, generating a gain of c €4.3m. ERAG stated at the AGM for the business year 2016 that it intends to focus on strengthening the balance sheet by retaining profits for the next three years, ie defer from paying any dividends.

Earnings outlook

It is beyond the scope of this note to provide forward looking estimates for the group and we note that there is currently no market consensus to refer to. Helpfully, management has given some guidance to its expectations for the current year. For 2017 it expects higher revenues from ship management and asset management and for revenues overall to be moderately higher than in 2016. Ship management and asset management revenues should be the main beneficiaries of a full year contribution from the acquisitions. The König & Cie contribution to investor management revenues was substantially recognised in its 11-month contribution in 2016 and we interpret management guidance as indicating ongoing revenue pressure from the trend run-off in managed trust capital. In terms of profitability, and barring unforeseen events, management guides to a positive net result that reaches the prior year level. We would expect group costs to continue to benefit in 2017 from the cost reductions that were made to the enlarged cost base during 2016. The headwind for 2017 operating profit compared with 2016 is the balance of other income and expenses. Management has indicated that it expects to make further significant impairments in relation to trustee services and investor management receivables in 2017, while it will not benefit from the high level of non-recurring income earned in 2016.

There are plans to invest further in the maritime and real estate sectors which may include further own investment in assets; on this basis management anticipates a small reduction in cash balances by the end of 2017 vs 2016, but still representing a high enough level to allow the company to act on opportunities as they arise.

In this section we comment on the valuation of ERAG shares in the context of a broad peer group of listed asset managers, including private equity, specialist and conventional asset managers in Europe and North America, using consensus data sourced from Bloomberg. The lack of forward looking consensus data for ERAG is a handicap in this respect, especially at a time of significant strategic and operational change. Although 2016 net earnings include substantial one-off income, noting management guidance of a moderate increase in current year operating earnings we have decided to use 2016 net earnings data as a guide to the current year. Readers should be aware that there could be a significant variance in the ratio of 2017 net income to operating profit vs 2016; with net income including the contribution from associates, income from investments and other financial income/costs, as well as taxes, all of which may differ greatly from 2016 levels.

The average of the consensus P/E multiples for the current year and next is surprisingly similar across each of the sub-groups despite the significant difference in business models that are represented. However, the spread within groups is larger. ERAG EPS in 2016 was €0.20 which puts the shares on a P/E of c 6.0x, substantially below the peer group average and implying the potential for significant undervaluation. We estimate the 2016 ERAG return on closing equity to have been c 16%. While this includes the one-off items referred to above it does not include a full year contribution from acquisitions. Although 16% is lower than the peer average this seems to be more than reflected in a lower P/BV at around 1x.

Exhibit 12: Peer valuation data

|

Share price (local cur) |

Mkt. cap (US$m) |

Current year P/E (x) |

Next year P/E (x) |

Current year ROE (%) |

Next year ROE (%) |

Last reported P/BV (x) |

Dividend yield (%) |

Private equity group |

|

|

|

|

|

|

|

|

Partners Group |

600 |

16,351 |

28.3 |

25.8 |

35.3 |

34.5 |

9.6 |

2.6% |

Blackstone |

33.37 |

39,896 |

11.4 |

10.5 |

25.6 |

32.8 |

5.8 |

5.0% |

Fortress |

7.99 |

3,094 |

8.0 |

7.8 |

N/A |

N/A |

N/A |

5.8% |

KKR |

18.96 |

15,409 |

8.5 |

7.8 |

16.4 |

17.9 |

1.4 |

3.4% |

3i Group |

9.305 |

11,363 |

10.0 |

9.6 |

14.7 |

14.0 |

1.4 |

2.8% |

Specialist group |

|

|

|

|

|

|

|

|

Apollo |

27.43 |

11,149 |

10.8 |

9.8 |

33.8 |

69.1 |

6.9 |

4.6% |

Ashmore |

3.597 |

3,227 |

17.1 |

17.3 |

22.2 |

19.3 |

3.5 |

4.6% |

Man Group |

1.556 |

3,256 |

10.4 |

8.2 |

13.8 |

18.5 |

1.5 |

5.8% |

Patrizia |

17.705 |

1,640 |

23.0 |

18.4 |

8.2 |

9.5 |

1.8 |

0.0% |

Lloyd Fonds |

3.551 |

36 |

8.7 |

79.3 |

16.6 |

15.7 |

1.4 |

4.5% |

MPC |

6.001 |

209 |

15.0 |

11.3 |

12.8 |

15.1 |

1.8 |

0.0% |

Ernst Russ |

1.19 |

35 |

N/A |

N/A |

N/A |

N/A |

1.0 |

N/A |

Deutsche Beteiligungs |

39.25 |

|

7.9 |

11.2 |

19.4 |

12.0 |

1.5 |

3.1% |

Conventional group |

|

|

|

|

|

|

|

|

Aberdeen |

2.912 |

4,867 |

13.4 |

12.9 |

13.8 |

14.1 |

2.2 |

6.7% |

Azimut |

18.09 |

2,870 |

13.7 |

13.0 |

28.8 |

28.5 |

3.5 |

5.5% |

Janus Henderson |

31.71 |

6,355 |

23.2 |

17.9 |

12.7 |

10.7 |

1.9 |

0.0% |

Jupiter |

4.972 |

2,876 |

14.8 |

14.3 |

24.4 |

22.7 |

3.5 |

3.0% |

Schroders |

31.39 |

10,566 |

15.9 |

15.0 |

17.2 |

16.9 |

2.5 |

3.0% |

Averages |

|

|

|

|

|

|

|

|

Private equity |

|

|

13.2 |

12.3 |

23.0 |

24.8 |

4.6 |

3.9% |

Specialist |

|

|

14.2 |

24.0 |

17.9 |

24.5 |

2.8 |

3.2% |

Conventional |

|

|

16.2 |

14.6 |

19.4 |

18.6 |

2.8 |

3.6% |

All |

|

|

14.5 |

17.4 |

19.8 |

22.6 |

3.1 |

3.6% |

Source: Bloomberg data as at 8 June 2017

In the absence of forward-looking estimates it may be useful to consider the valuation that the market is placing on the group’s potential earnings base as measured by AUM (although this would not capture any value for the third-party maritime asset management activities). In Exhibit 13 we compare ERAG with close local peers Lloyd Fonds and MPC, as well the real estate focused manager Patrizia.

Exhibit 13: P/AUM and revenue/AUM comparison with close local peers

|

Mkt. cap

(€m) |

AUM

(€bn) |

Mkt cap/AUM

(%) |

2016 revenues

(€m) |

Revenues/AUM

(%) |

Patrizia |

1,482 |

18.6 |

8.0% |

818 |

4.40% |

Lloyd Fonds |

32 |

1.4 |

2.3% |

9.5 |

0.68% |

MPC |

183 |

5.1 |

3.6% |

53.8 |

1.05% |

Ernst Russ |

32 |

6.5 |

0.5% |

40.0 |

0.61% |

Source: Company data, Bloomberg

While there appears to be a positive relationship between the level of valuation and the market capitalisation (the larger the market cap, the higher the ratio of market cap to AUM), the market cap/AUM valuation placed on ERAG is considerably lower than Lloyd Fonds which has a similar market capitalisation. We also note that both companies generate similar levels of revenues as a percentage of AUM. While this observation should not be taken as confirmation of undervaluation, it is a further indication that the market is undervaluing the earnings potential within ERAG.

The prospects for the group are particularly dependent upon the shipping markets. While the current challenging conditions in the shipping market may provide opportunities for ERAG to participate in restructuring situations and potential consolidation (providing advice, financial solutions, or engaging in M&A), a sustainable recovery in the market is needed to significantly boost the group’s fortunes. Meanwhile, revenues and the value of assets and receivables remain sensitive to volatile charter rates. In addition we would highlight the following:

■

An increase in interest rates and/or an economic slowdown could be expected to have a dampening effect on investor demand for real assets in general (including real estate) making it more difficult for ERAG to offset the impact of the decline over time in existing closed-end fund managed trust capital.

■

An economic slowdown would be likely to reduce the returns available on real assets, limiting returns on existing funds and investor appetite for new investments.

■

Currency risks are a feature of shipping assets in particular (where revenues are typically US$ denominated) with the potential to affect revenues as well as asset and receivables values. In some cases these risks are hedged although no details or sensitivities have been disclosed.

■

Legal risks, in particular related to the prospectus based issuing process of retail focused funds can create issues many years after fund issuance if the information provided can be shown to be incomplete, inaccurate, or misleading. The annual report provides details of outstanding legal claims. Briefly, total claims from investors outstanding at the end of 2016 were €147m (2015: €129m) of which €110m have proceeded to court (2015: €82m). Claims are regularly evaluated and at the end of FY16 management’s assessment was that 87% of claims were either ‘unlikely’ or ‘very unlikely’ to be successful with a statistical probability of 1–30%. Including an impact from the companies acquired, ERAG has provisions of €5m (2015: €1m) to cover claims in excess of the group’s insurance arrangements.

■

An additional legal risk, primarily to liquidity, arises from the historical distribution of closed-end fund liquidity against future expected earnings that have not materialised. The ERAG group, as limited partner, is potentially liable for settling claims by fund creditors, later reclaiming against fund investors. The issue, detailed in the annual report, covers liquidity payments of €274m as at the end of 2016 (2015: €258m) for which ERAG has a potential risk of €46.6m (2015: €49.7m), meaning that €46.6m is paid out and €41.2m is collected thereafter. ERAG continues to work on financial restructuring solutions for struggling funds that reduce the amount of liquidity potentially at risk, sometimes significantly. Taking into account the ability to reclaim any amount against fund investors, ERAG estimates a net risk of unenforceable claims on those investors of €5.4m for which €2.5m has been provided for as accruals on the balance sheet.

■

ERAG has issued guarantees for equity raised in certain fund products, largely ship funds. These guarantees are linked to the maturity of loans provided by the financing banks and are backed by zero and bearer bonds. The potential payments are linked to the performance of the funds. ERAG ended negotiations on the maximum draw at the beginning of the year, leading to a reduction in accruals from €4.5m in 2015 to €1.0m in 2016.

■

ERAG has also provided certain guarantees in relation to the placement of funds. ERAG said that there is a potential ‘significant’ risk to ERAG’s financial position if these guarantees are drawn.

Frankfurt +49 (0)69 78 8076 960 Schumannstrasse 34b 60325 Frankfurt Germany |

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom |

New York +1 646 653 7026 295 Madison Avenue, 18th Floor 10017, New York US |

Sydney +61 (0)2 8249 8342 Level 12, Office 1205 95 Pitt Street, Sydney NSW 2000, Australia |

Edison, the investment intelligence firm, is the future of investor interaction with corporates. Our team of over 100 analysts and investment professionals work with leading companies, fund managers and investment banks worldwide to support their capital markets activity. We provide services to more than 400 retained corporate and investor clients from our offices in London, New York, Frankfurt and Sydney. Edison is authorised and regulated by the Financial Conduct Authority. Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER

Any Information, data, analysis and opinions contained in this report do not constitute investment advice by Deutsche Börse AG or the Frankfurter Wertpapierbörse. Any investment decision should be solely based on a securities offering document or another document containing all information required to make such an investment decision, including risk factors. Copyright 2017 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Deutsche Börse AG and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2017. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent. |

|