Senegal: Examine value not volumes

The discoveries of FAN-1 and SNE-1 in October and November 2014 (40% WI) respectively, were a high point for exploration in that year (FAN was the largest discovery globally). The consortium has drilled multiple exploration and appraisal wells since and Cairn has given indications of a development concept based on its current 2C reserves estimate. How should we approach a valuation of the assets? We review a number of approaches to give indications of value from invested capital to implied values from pure-play peers. Unsurprisingly, these give a range of values.

We believe the analysis indicates few major avenues for investors to see step-change upside in the asset other than reserves upgrades and successful exploration. We expect a reserves update in August after the results of the interference testing at SNE-6 are fully interpreted, which will inform how the upper reservoirs (which hold a majority of OIP but have produced the lower test rates so far) are best exploited. Exploration at FAN South and SNE North (formerly Sirius) could add incrementally, although time to develop these potential tie-ins to a core SNE development will mean that a marked increase in value is unlikely, we think.

Exhibit 4: Current value for Cairn’s Senegal stake

|

|

Source: Edison Investment Research

|

At the end of 2016, Cairn held the Senegalese assets on its balance sheet at US$330m, equivalent to 45p/share. With a proposed investment in 2017 of US$155m (including contingent drilling costs of $50m), this would rise to 65p/share by the end of the year.

Woodside’s 2016 acquisition of Conoco’s stake gives a good guide as to the value that industry attributes to the area. The acquisition for $442m of a 35% interest implies a gross block value of $1,257m (this includes $92m of adjustments to compensate for capex). This implies a Cairn value of 69p/share.

We use discounted cash flows as the primary valuation methodology, modelling the fiscal terms as available to us and a set of macro, opex and capex assumptions using company guidance where available and appropriate. This gives us a value that we can track over time to see how the value increases as capital is invested and production cash flows approach. The mechanism of value increase for SNE shown below indicates growth of around 25% pa (on an unrisked basis).

We note our risked valuation for SNE roughly tracks the capital invested until 2017/2018 as the long-term risked value of the asset only exceeds the significant (and required) outlay on appraisal wells. The excess of value over investment increases markedly in coming years however. By first oil in mid 2020s, our modelling assumes that Cairn (at current working interest of 40%) would have invested the equivalent of 312p/share, but would have an NPV12.5 of c 578p/share. In a farm-down scenario, the value in 2024 would be 357p/share having invested around 145p/share. In the first five years of production, the asset will produce over $9.6bn of gross post-tax cash flow (assuming long-term Brent prices of $70/bbl real, with a 2.5% quality discount applied given the 32° API oil).

Exhibit 5: (Un)risked valuation of SNE net to Cairn vs capex spent (assuming no farm-down is done)

|

Exhibit 6: (Un)risked valuation of SNE net to Cairn vs capex spent (farm down)

|

risked valuation of SNE net to Cairn vs capex spent (assuming no farm-down is done)")

|

risked valuation of SNE net to Cairn vs capex spent (farm down)")

|

Source: Edison Investment Research. Note: This assumes that Cairn retains 40% interest.

|

Source: Edison Investment Research. Note: This assumes our base case that Cairn farms-out 15% of its interest (retaining 25%) in return for a development carry.

|

Exhibit 5: (Un)risked valuation of SNE net to Cairn vs capex spent (assuming no farm-down is done)

|

|

Source: Edison Investment Research. Note: This assumes that Cairn retains 40% interest.

|

Exhibit 6: (Un)risked valuation of SNE net to Cairn vs capex spent (farm down)

|

|

Source: Edison Investment Research. Note: This assumes our base case that Cairn farms-out 15% of its interest (retaining 25%) in return for a development carry.

|

The major sensitivities to our valuation are discount rate and long-term oil price. Reducing our discount rate from 12.5% to 10% would see a >50% increase in NPV. A US$5/bbl decrease in the long-term oil price would see unrisked value fall by 14% (assuming Cairn farms-down).

Exhibit 7: Sensitivities to oil price and discount rates (NPV in 2017) (assuming a farm-down)

|

(assuming a farm-down)")

|

Source: Edison Investment Research

|

We also note that because of our methodology (assuming FAR’s relatively high estimate vs Cairn’s 473mmbbls, but using a higher capex intensity and risking at 60%), it is possible an increase in Cairn’s estimate of SNE volumes to below the 641mmbbls but lower capex than we conservatively assume will only have a relatively muted effect on our valuation. For example, an estimate of 580mmbbls and lower capital intensity would increase our SNE valuation by 4p/share (vs a 9p fall if we move our long-term Brent assumption from $70/bbl to $65/bbl, for example).

Valuing by proxy – FAR Ltd

FAR is an Australian-listed company that is (largely) a pure play on Senegal. We can therefore derive a proxy value for Cairn’s interest in Senegal by looking at the EV of FAR (WI 15%) and adjusting for working interests. This generates the charts below. We note the expansion in value implied by FAR is attributed to a doubling of the share price, a 60% plus increase in share count (from date of discovery) and a small movement of exchange rates.

Exhibit 8: FAR’s EV and share price (A$/share)

|

Exhibit 9: Implied value of Senegal to Cairn shareholders, p/share

|

")

|

|

Source: Bloomberg, Edison Investment Research

|

Source: Edison Investment Research, Bloomberg

|

Exhibit 8: FAR’s EV and share price (A$/share)

|

|

Source: Bloomberg, Edison Investment Research

|

Exhibit 9: Implied value of Senegal to Cairn shareholders, p/share

|

|

Source: Edison Investment Research, Bloomberg

|

Also overlain in the charts above is the implied value from the target price valuation of FAR analysts. Perhaps not surprisingly, given the range of analyst approaches and levels of optimism sometimes seen in pure-play explorers, this view implies a very high value. We note that the Bloomberg consensus target price includes four of the eight brokers, one of which has a target price over twice that of the consensus number. Just to underline the range of estimates for FAR’s value, there are two target prices above A$0.2/share, which, given the number of shares outstanding and net cash position, would imply that these analysts believe that FAR should be worth more than Cairn’s current market cap (even though Cairn has other assets and >2.5x the working interest in SNE).

This is a paradox. Cairn is a well-funded E&P with two large developments that will be cash flow positive by the end of 2017. It held cash of $335m at end December 2016 and will have c $210m of RBL facility by the end of 2017 (and an estimated peak RBL facility of $350-400m). The cash flows from Catcher and Kraken together with the RBL facility could be enough to fund the SNE development without recourse to new equity. On the other hand, FAR has no internally sourced cash flows and will have to source hundreds of millions (>US$500m) of capital pre-first oil. By definition, FAR has a much higher cost of capital and so arguably FAR should be valued at a lower level than Cairn, yet we believe that its assets are valued higher by the market.

Three avenues for upside in Senegal

FAN-1 was discovered in October 2014 with the SNE well success announced in November. Since then, the consortium has drilled six appraisal wells on SNE while none have been drilled at FAN. Cairn remarked that although the FAN structure is large, the reservoir quality is poor. Because of this and its lack of action on SNE, we do not believe FAN figures in any future development plans. For investors, this leaves three avenues for upside in Senegal, other than the natural de-risking as the development moves towards FID and then production: (i) a full delineation of SNE with possible increases following appraisal; (ii) exploration; or (iii) improvement of project economics.

Delineation and increases to reserve estimates hinge on recovery factors

SNE has seen consistent increases to recoverable barrels since discovery as successful appraisal wells have de-risked the flanks of the structure and given greater confidence in the reservoir characteristics. FAR has updated its (independently audited) estimates more regularly than Cairn, and the most recent estimate is notably above those of Cairn (as seen below). Cairn has indicated that FAR’s higher estimates are most likely due to the application of higher recovery factors (mid-year results, August 2016). Cairn expects to publish an updated reserve estimate in August.

Exhibit 10: Estimates for recoverable barrels from SNE (FAR, Cairn and Woodside)

|

")

|

Source: FAR, Cairn and Woodside. Note: The Woodside number seems to be the average of the available Cairn and FAR estimates at the time.

|

The reservoir at SNE consists of many layers, but they are broadly split by Cairn into Upper and Lower Zones. The Lower Zones are good quality and have produced at a constrained rate of 8,000bopd when tested in SNE-2.

As illustrated below, the consortium has concentrated far more on the upper reservoirs since then. They contain the majority of OIP but are described as being thinner and finer grained and have produced at lower rates than the Lower reservoir sands (SNE-3 produced at 5.4kbd). Additionally, during testing of these Upper Zones in SNE-3, slight pressure depletion was observed. This could have indicated that SNE-3 is not well connected to the rest of the field.

Exhibit 11: Summary of well results – a great deal more effort has been made to determine upper reservoirs

Date |

Well |

Reservoirs tested |

Flow rates achieved |

Gross oil bearing column |

10 Nov 2014 |

SNE-1 |

|

|

95m |

4 Jan 2016 |

SNE-2 |

Lower and upper reservoirs |

DST over a 12 metre (m) interval of high quality pay flowed at a maximum stabilised, but constrained rate of ~8,000bopd on a 48/64” choke, confirming the high deliverability of the principal reservoir unit in the SNE-2 well

DST over a 15m interval (~3.5m net) of relatively low quality “heterolithic” pay flowed at a maximum rate of ~1,000bopd on a 24/64” choke, confirming that these reservoirs are able to produce at viable rates and thus make a material contribution to resource volumes. Flow was unstable due to the 4.5” DST tubing |

103m |

1 Mar 2016 |

SNE-3 |

Upper reservoirs |

DST 1a flowed at a maximum rate of ~5,400bopd and a main flow rate of ~4,000bopd over a 24-hour period from a 15m) zone

For DST 1b an additional zone of 5.5m was added and a combined maximum rate of ~5,200bopd measured, with an associated main flow rate of ~4,500bopd over a six-hour period |

101m |

11 Apr 2016 |

SNE-4 |

Upper reservoirs |

Not tested |

c 100m |

7 Mar 2017 |

SNE-5 |

Upper reservoirs |

DST 1a flowed from an 18m interval at a maximum rate of ~4,500bopd on a 60/64” choke. Two main flows of 24 hours each were performed; the first at ~2,500bopd on a 40/64” choke, followed by a second at ~3,000bopd on 56/64” choke

For DST 1b an additional 8.5m zone was added and the well flowed at a maximum rate of 4,200bopd and for 24 hours at an average rate of ~3,900bopd on 64/64” choke |

|

6 Apr 2017 |

VR-1 |

Lower reservoirs |

5km step out. Cairn suggests that recovery factors from lower sands “should yield recovery factors of 30% or more”... “VR-1 confirmed the 1C proven resources for the field” |

|

18 May 2017 |

SNE-6 |

Upper reservoirs |

The objective of the SNE-6 well was to flow oil from one of the principal units in the upper (400 series) reservoirs and demonstrate connectivity between the two wells. Pressure data from SNE-6 immediately confirmed good connectivity with SNE-5 and accordingly a short DST was performed. Two DST were performed: a longer 48-hour test on an 11m interval that produced 3,700bopd and (with the addition of a further 12m interval) a 24-hour test averaging 4,700bopd. Pressure data confirmed that SNE-6 is connected to SNE-5 (1.6km away). We note that the plan pre-well was to test for 10 days and see connection to both SNE-5 and SNE-3. No mention was made of SNE-3 in the release |

|

Source: Cairn Energy, Edison Investment Research

Exhibit 12: SNE schematic cross section

|

|

|

|

To investigate this pressure decline further, the SNE-6 well was planned to be tested for a longer period of time (of around 10 days) in order to carry out an interference test. It was hoped that the pressure pulse generated by the change of pressure at SNE-6 would be detected by gauges installed at SNE-5 and SNE-3, providing a clearer picture of the connectivity of the reservoir. This would then be used to assess the potential effectiveness of waterflooding and could affect the field recovery factor. The results will have an impact on the number, design, placement and orientation of future development wells in the upper reservoirs. This is critical because the majority of OIP is in the upper reservoirs (and where we believe the recovery factor is currently estimated to be lower than that assumed in the lower reservoirs).

Results of SNE-6 (released by Cairn on 18 May), indicate that a much shorter DST was performed (48 hours vs 10 days planned) as pressure data immediately confirmed good connectivity with SNE-5. This is in line with Cairn’s existing model, which indicated that oil would flow preferentially to SNE-5. We note that no mention was made of connectivity with SNE-3 – it is possible that Cairn felt able to confirm its model given the speed at which connectivity with SNE-5 was measured.

Making a case for existing assumptions on recovery factors

An RNS by Cairn after the VR-1 well in April 2017 indicated that “the lower 500 series reservoirs are the better connected, more tabular, highly productive sands, where water-flooding should yield recovery factors of 30% or more.” We do not know the exact split of resources between the layers, but Cairn indicated that a greater proportion of the SNE resources sit in these Upper zones (the Q4 results indicated the upper reservoirs account for “the bulk of the oil in place”). Interpretations of “bulk” vary, but we would imagine that this could be seen as being between 60-80%. Using a 30% recovery factor in the lower reservoirs would imply that RF for the upper reservoirs is currently assumed in the 473mmbbl 2C estimate to be between 9-14% (depending on what the split of OIP between the reservoirs is). This rises to 19-22% if we assume the 641mmbbl 2C estimate given by FAR (and the estimate we adopt following the positive interference test). These are obviously very different ranges and illustrate why so much energy and capital has been expended trying to better understand the upper reservoirs.

Exhibit 13: Low implied recovery factors in the upper reservoirs assuming given recovery factors in lower reservoirs and OIP distribution (using 2C estimate of 473mmbbl)

|

|

% of volumes in upper reservoirs |

|

|

60% |

70% |

80% |

Assumed recovery factor in lower reservoirs |

25% |

12% |

14% |

15% |

30% |

9% |

12% |

14% |

35% |

5% |

10% |

13% |

40% |

2% |

8% |

12% |

Source: Edison Investment Research

This also informs our thinking about how much upside there could be above 641mmbbl. Unless the OIP increases and the recovery factor assumed in the lower reservoirs is above the 30% that seems to have been indicted by Cairn (both of which are possible), the 641mmbbl estimate already assumes a reasonable recovery factor in the upper reservoirs of perhaps 20%. The positive interference test gives us more confidence in the upper reservoirs, but we are hesitant to think it would necessarily move up to 30% at this stage.

Exhibit 14: Implied recovery factors in the upper reservoirs assuming given recovery factors in lower reservoirs and OIP distribution (using 2C estimate of 641mmbbl)

|

|

% of volumes in upper reservoirs |

|

|

60% |

70% |

80% |

Assumed recovery factor in lower reservoirs |

25% |

22% |

23% |

23% |

30% |

19% |

21% |

22% |

35% |

16% |

18% |

20% |

40% |

12% |

16% |

19% |

Source: Edison Investment Research

Cairn stated at its full year results announcement that it may drill two further exploration wells in 2017 (the Sirius/SNE North and FAN South prospects), so it was no great surprise to see FAR announce that the next exploration well would be at FAN South.

The first well drilled by Cairn in Senegal (FAN-1) was a discovery that, crucially, established the presence of world class source rocks in the region. It encountered a hydrocarbon interval of over 500m, but the reservoir quality was not as promising as seen in the subsequent shelf well SNE-1 and so Cairn focused on the appraisal of SNE while developing geological models to identify areas of improved reservoir thickness and quality either in FAN or in another fan along the trend.

Based on this modelling work, FAN South-2 was positioned slightly shallower in the basin than FAN-1, where Cairn believed it should be able to encounter much better developed reservoir characteristics. FAN South-2 was a new fan on trend with the North Fan and with a separate input point and new layers. The well was located around 20km south-east of SNE-3 in 2,139m of water (compared to 1,100m in SNE) and targeted a Cretaceous channelised turbidite fan with multiple stacked layers. It was estimated by Cairn to contain more than 110mmbbl with a consolidated chance of success of 24%. The same prospect was estimated in mid-2016 to contain just over 150mmbbl with a 15% CoS, so work had affected understanding of the prospects notably.

Exhibit 15: FAN-South well location cartoon

|

Exhibit 16: FAN structures in block

|

|

|

|

|

|

Exhibit 15: FAN-South well location cartoon

|

|

|

|

Exhibit 16: FAN structures in block

|

|

|

|

On 11 July, Cairn announced results from the well. Hydrocarbon bearing reservoir was encountered, with oil samples collected of 31 API oil. However, the company indicated that further work would be needed to assess potential commerciality of the discovery. This suggests to us that the discovery is not as large as forecast, that the reservoir has poorer permeability/porosity than thought. For now, it looks like both FAN wells have given sub-commercial results.

Sirius and other exploration

For Sirius/SNE North, Cairn currently estimates a 67% CoS over 80mmbbl (FAR indicates 294mmbbl at 60%). We note that these consolidated chances of success may be misleading for some, and cannot be directly applied to the total prospect sizes as each prospect is made up of a number of individual intervals with unique CoSs. We note the CoS for the two prospects given by FAR are lower as seen below (we also note the difference in sizes estimated).

Exhibit 17: Summary of exploration prospects and chances of success

Prospect |

Play type |

FAR estimates |

Cairn estimates |

Gross prospective recoverable oil (P50), mmbbl |

CoS, % |

Gross prospective recoverable oil (P50), mmbbl |

CoS, % |

Sirius/SNE North |

Albian shelf edge |

294 |

60% |

80 |

67% |

Spica |

Albian shelf edge |

199 |

37% |

|

|

Leebeer SNE |

Late Albian shelf |

116 |

33% |

|

|

Leebeer Sirius/SNE North |

Late Albian shelf |

50 |

20% |

|

|

Leebeer Spica |

Late Albian shelf |

47 |

20% |

|

|

Rufisque Onlap |

Albian |

181 |

14% |

|

|

Alhamdulillah |

Albian FAN |

80 |

23% |

|

|

Leraw |

Cenomanian |

108 |

23% |

|

|

Jabbah |

Cenomanian |

44 |

25% |

|

|

Jabbah Deep |

Cenomanian |

111 |

16% |

|

|

South FAN |

Cretaceous FAN |

134 |

18% |

110 |

24% |

Central FAN |

Cretaceous FAN |

96 |

17% |

|

|

Source: RISC (via FAR) and Cairn Energy Note: We consider the South FAN well sub-commercial and therefore valueless currently

Two questions occur to us on this exploration programme:

■

How many more exploration wells will be drilled in the blocks beyond FAN South and (we assume) Sirius/SNE North?

■

If successful, how much would discoveries be worth?

How many more exploration wells will be drilled?

In terms of material wells in the near term, we do not think many more will be drilled. Given the factors listed above, it is very useful to know (or at least have a good indication of) the sizes and characteristics of any other potential developments around the core field before the finalisation of the designs for the core development (and particularly the FPSO). Greater gas concentrations or different oil properties could require meaningful changes to a design that are best catered for in the initial construction. Changes to gas/water processing capacity are harder to make down the line.

The size of the prospects of the planned wells and the relatively low CoS for the South FAN suggests that there are few material candidates for exploration in coming years. The de-risking brought about by the SNE (and FAN) wells has only increased three of these prospects to above 30% CoS, while many are small and would not make a great deal of difference to FPSO design. Small tie-in exploration wells are possible in the fullness of time – we would not be surprised to see Spica drilled if Sirius is successful, but other prospects in the block may have to wait (indefinitely). The partners may look to deploy capex to other areas, especially if the CoS remains the same (relatively low).

Exhibit 18: Prospects around SNE and FAN

|

|

|

|

")

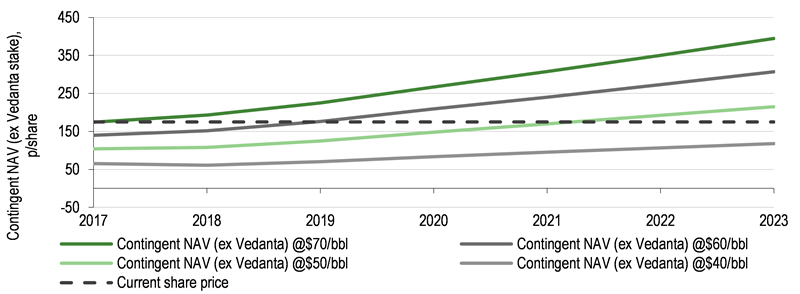

at different oil prices")

")

, since January 2015")

, since January 2015")