Revenues: FY18 affected by Argentine peso devaluation

FY18 revenues declined 9.9% vs FY17 to €1,476.4m. This was driven by a 30% decline in Argentine revenues, due to the depreciation of Argentine peso against the euro, which was partially offset by a 17% revenue increase in Spain. In constant currency, revenues were up 9.3% vs the prior year. The impact of the Argentine peso is reflected in our FY19 figures and we forecast flat revenues in FY19, at €1,477.4m. Thereafter, we are forecasting 9.0% growth in FY20 and 8.5% in FY21, particularly driven by Mexico and Spain, as well as a return to normal conditions in Argentina.

Adjusted EBITDA: Cost controls offset the impact of rising taxes and FX

Despite the increase in taxes and FX headwinds in Argentina, FY18 EBITDA increased 3.4% to €282.9m (in line with guidance of €280–285m). The improvement was largely due to performance initiatives across the business; management delivered €49.4m of cost and growth efficiencies in FY18 and expects a further €41–46m in FY19.

In FY19 the trends will be similar, with cost controls offsetting rising taxes and FX headwinds. Our FY19 EBITDA forecast is €361.9m, which is positively affected by c €80m in IFRS 16 adjustments (lower operating costs). Note that the adjusted EBITDA also excludes €12m of exceptional online marketing costs in Mexico. This is in line with company guidance of adjusted EBITDA of €280–290m (pre IFRS 16 adjustments).

We summarise our forecast assumptions in Exhibit 16 below; please see the individual country sections for more details on revenue and EBITDA dynamics.

Mexico: 8% revenue growth, one-off €10–15m marketing costs in FY19

Underlying revenue growth in the Mexican market has historically been around 3%, but we believe this will rise significantly due to ongoing investment and the openings of new halls. For FY19 and FY20, we forecast a c 8% revenue increase to €355.5m and €383.9m, respectively. Management is focusing on cost containment and we forecast a continued strong EBITDA margin of c 45% (note that this now includes an estimated c €38m positive contribution due to IFRS 16 adjustments). For FY19, we forecast additional marketing costs of €12m, but this is included as a non-recurring item.

Argentina: Peso devaluation and tax increases

Given the impact of the devaluation of the peso, we forecast an absolute decline in revenues of 20% in FY19, before returning to 15% growth in FY20 and FY21. This increase is similar to trends from previous periods that followed significant currency devaluations (specifically after 2001), although our forecast revenue of €431.2m in FY21 is still considerably lower than €582.4m revenues achieved in FY17. The impact of the tax increase is estimated at around €10m annually and, together with continued cost controls, we forecast an FY19 EBITDA of €73.6m, rising to €91.0m in FY20. IFRS 16 positively affects EBITDA by an estimated c €7m.

Italy: Stringent gaming regulation affects EBITDA by €10m

Despite the capacity reductions in Italy in FY18, Codere successfully managed to optimise its portfolio with the result that revenues remained flat. Similar to trends in Q119, we forecast a modest 1.4% revenue growth for FY19 and 2% thereafter. This will be accompanied by steadily rising taxes (as detailed above). Codere has guided to a c €10m reduction in EBITDA, as mitigation will offset some of the increase in taxes. We forecast FY19 EBITDA of €28.6m, which includes a positive estimated impact of c €9m from IFRS 16 adjustments.

Spain: Sports betting to drive growth; online reported separately from FY19

With the increased momentum in sports betting and online, FY18 revenue increased by 17% to €220.0m. From FY19, online will no longer be reported within the Spanish division and we forecast Spanish revenues of €208.0m in FY19. Thereafter, we forecast 15% revenue growth in FY20 and FY21 as investment in the sports betting shops steadily translates to revenue. Our EBITDA forecast goes from €26.4m (12% margin) in FY18 to €49.6m (23.8% margin) in FY19, as the lower margin online is excluded and IFRS 16 contributes an estimated c €8m.

Other: Including online from FY19 onwards

In FY18, other operations were affected by FX and by the closure of underperforming halls, and revenues declined by 4.3% to €183.8m. In line with Q119 trends, our FY19 forecasts assume an 8.1% decline in Panama revenues and a 4% decline in Colombia revenues, offset by a 10.6% increase in Uruguay revenues. Following the closure of underperforming halls in Panama and Colombia, we forecast a return to low single-digit growth in those regions for FY20.

For online, we forecast revenues of €64.2m in FY19 and €73.9m in in FY20, as Codere begins to gain traction in Mexico and Spain in particular. We believe these figures are reasonably conservative and suspect there be upside.

Altogether for other operations, we forecast FY19 revenue growth of 34.1% (which importantly now includes online). Online margins were only 8% in Q119 but, given the cost containments across all geographies and an estimated c €17m increase from IFRS 16 adjustments, our total EBITDA margin for other operations goes from 21.7% in FY18 to 24.7% in FY19.

We include a summary table of the country revenue and EBITDA mix here:

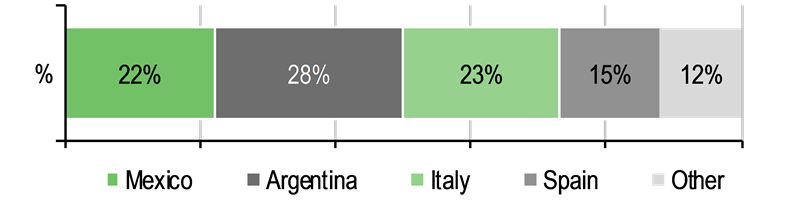

Exhibit 16: Geographic revenue and EBITDA split (€m)

Revenue |

2014 |

2015 |

2016 |

2017 |

2018 |

2019e* |

2020e* |

2021e* |

Mexico |

341.9 |

355.3 |

329.8 |

339.9 |

328.3 |

355.5 |

383.9 |

406.9 |

growth |

|

3.9% |

-7.2% |

3.1% |

-3.4% |

8.3% |

8.0% |

6.0% |

Argentina |

489.0 |

681.8 |

534.5 |

582.4 |

407.7 |

326.1 |

375.0 |

431.2 |

growth |

|

39.4% |

-21.6% |

9.0% |

-30.0% |

-20.0% |

15.0% |

15.0% |

Spain |

149.9 |

155.9 |

170.2 |

188.0 |

220.0 |

208.0 |

239.2 |

275.1 |

growth |

|

4.0% |

9.2% |

10.5% |

17.0% |

-5.4% |

15.0% |

15.0% |

Italy |

263.8 |

284.2 |

321.5 |

335.8 |

336.5 |

341.4 |

348.2 |

355.2 |

growth |

|

7.7% |

13.1% |

4.4% |

0.2% |

1.4% |

2.0% |

2.0% |

Others |

141.0 |

162.3 |

189.8 |

192.1 |

183.8 |

246.5 |

263.6 |

278.7 |

growth |

|

15.1% |

16.9% |

1.2% |

-4.3% |

34.1% |

6.9% |

5.7% |

Total |

1,385.6 |

1,639.5 |

1,545.8 |

1,638.2 |

1,476.4 |

1,477.4 |

1,609.9 |

1,747.1 |

growth |

|

18.3% |

-5.7% |

6.0% |

-9.9% |

0.1% |

9.0% |

8.5% |

EBITDA |

2014 |

2015 |

2016 |

2017 |

2018 |

2019e |

2020e |

2021e |

Mexico |

75.1 |

91.5 |

88.5 |

92.9 |

105.9 |

162.2 |

169.6 |

181.4 |

margin |

22.0% |

25.8% |

26.8% |

27.3% |

32.3% |

45.6% |

44.2% |

44.6% |

Argentina |

93.4 |

146.1 |

131.0 |

134.2 |

96.1 |

73.6 |

91.0 |

112.1 |

margin |

19.1% |

21.4% |

24.5% |

23.0% |

23.6% |

22.6% |

24.3% |

26.0% |

Spain |

17.6 |

24.6 |

29.5 |

25.1 |

26.4 |

49.6 |

60.7 |

75.9 |

margin |

11.7% |

15.8% |

17.3% |

13.4% |

12.0% |

23.8% |

25.4% |

27.6% |

Italy |

29.4 |

26.7 |

26.4 |

23.6 |

27.6 |

28.6 |

28.6 |

30.7 |

margin |

11.1% |

9.4% |

8.2% |

7.0% |

8.2% |

8.4% |

8.2% |

8.6% |

Others |

18.9 |

14.2 |

23.1 |

28.2 |

39.9 |

60.9 |

61.2 |

63.1 |

margin |

13.4% |

8.7% |

12.2% |

14.7% |

21.7% |

24.7% |

23.2% |

22.7% |

Corporate costs |

(21.2) |

(23.0) |

(30.9) |

(30.4) |

(13.0) |

(13.0) |

(14.5) |

(15.5) |

Total |

213.2 |

280.1 |

267.7 |

273.5 |

282.9 |

361.9 |

396.7 |

447.7 |

margin |

15.4% |

17.1% |

17.3% |

16.7% |

19.2% |

24.5% |

24.6% |

25.6% |

Source: Codere, Edison Investment Research. Note: *Includes IFRS 16 adjustments.

As discussed above, Codere has been facing FX headwinds (particularly in Argentina) and rising taxes in both Argentina and Italy. However, these are expected to be offset by a continued cost-savings programme, with management guiding to €41–46m cost efficiencies for FY19.

Codere’s financial statements are complex and we highlight some of the key income statement items below:

■

Gaming and other taxes: in FY18 gaming and other taxes were €528.1m, or 35.8% of total revenues. This compares to 36.4% in FY17, with the decline being due to lower absolute taxes from Argentina (due to FX). For FY19, we forecast a total gaming tax rate of 36%.

■

Depreciation and amortisation: D&A for FY18 was €113.9m, which was flat vs FY17. Largely due to IFRS 16 adjustments, our D&A forecast increases to €164.0m in FY19.

■

Rental costs: total machine and other rental costs were €110.4m in FY18, which compares to €125.1m in FY17. The decline was due to continued cost containment, portfolio optimisation and the purchase of machines (rather than rentals). With the implementation of IFRS 16, a large portion of this figure (c €80m) is now capitalised and our rentals forecast for FY19 is €31.1m.

■

Other operating expenses: as part of the continuing cost-reduction programme (as well as FX in Argentina), personnel costs declined from €298m in FY17 to €252m in FY18 and we forecast Codere to continue focusing on personnel cuts. Total marketing costs were €45.6m in FY18 or 3.1% of revenues. Aside from the additional c €10–15m marketing spend for online expansion in Mexico, we expect this to rise steadily to c 5% of revenues, as online becomes more significant. Note that the pure online companies typically spend 25–30% of revenues on marketing, but clearly do not have many of the retail investment costs.

■

Tax: Codere’s tax position is highly complex, due to M&A, corporate reorganisations, financing structure and international operations. In FY18, the tax provision decreased by €25.8m to €38.4m, primarily due to the devaluation of the Argentine peso together with the positive €7.7m in deferred taxes (non-recurring), which was a result of applying the new regulation in Argentina that allows the revaluation of assets for corporate income tax purposes. The company has guided to a total tax cost of €40m in FY19.

■

Non-controlling interests: minority interests of €6.8m largely relate to Codere’s 85% owned ICELA subsidiary. In the absence of detailed information on ICELA, we assume a similar level going forward.

■

Non-recurring items in 2018 were €42.7m, which was largely due to the changes in the company leadership in January 2018 and to the operational efficiencies deployed by the new leadership. The breakdown was €13.0m management transition, €19.4m operational and personnel restructuring, €3.5m tax contingencies and €6.8m other. For FY19, the company has guided to non-recurring costs of €25m (€10m for litigation, €10m for restructuring and €5m other) and a further €10–15m in exceptional marketing costs in Mexico. Thereafter we are assuming c €10m per year.

Inflation adjusted accounting and asset revaluation

Given that inflation in Argentina reached more than 100% cumulatively over the last three years, the company started to apply IAS 29 (inflation accounting) in Q318. For FY18, Codere provided the impact of this accounting in four line items:

■

Operating profit was affected negatively by €19.5m: €12.2m on EBITDA and €7.3m on other opex.

■

Interest income was affected by €1.3m.

■

€7.7m lower tax due to the impact on the revaluation of assets for tax purposes.

■

An €87.6m increase in shareholders’ equity as assets were revalued.

Operating cash flow increased 9.1% to €182.8m in FY18, with the decrease in EBITDA fully offset by lower working capital and a decrease in cash tax paid. We summarise some of the key points here, which notably include capex.

In FY18, the cash interest expense was €68.8m: €53.3m for the senior notes, €13.8m for the OpCo debt (including capital leases) and €1.7m for the credit facility. Our cash interest forecast of €67m for FY19 excludes the non-cash IFRS interest expense on the P&L (c €45m annually).

Deferred payments: To affect FY19 and FY20

In FY18, deferred payments increased by €48.2m, consisting of a €2m decrease in authorised deferred gaming taxes in Spain and an increase in deferred payments with capex suppliers of €50.2m, mainly in Mexico and Panama (associated with new supplier financing deals on acquired slot products previously leased). We forecast an associated cash outflow of €20m in FY19, €25m in FY20 and €5m in FY21.

FY18 capex amounted to €163.4m, of which €82.1m was for maintenance and €81.3m for growth.

■

Growth capex relates to the expansion of the business, for example obtaining new licences, increasing the number of gaming machines, increasing the number of bingo seats or otherwise expanding the business. For 2018, growth capex was €81.3m (vs €64.2m in 2017), including €51.4m for acquisitions, of which c €39m was incurred in new product agreements mostly in Mexico and Panama.

■

Maintenance capex relates to maintaining the current capacity, including licence renewals. Maintenance capex in FY18 was €82.1m, due mainly to investment in Mexico of €25.2m (slot renewals and hall refurbishments, €21m in Spain (higher commercial capex offsetting lower product renewals in retail AWP) and €13m in Argentina (slot renewals, halls and casino management) and a €7.6m investment in Uruguay.

Exhibit 17 shows the capex profile, split between maintenance and growth. Codere has guided to c €100m for FY19, roughly split between €20–25m growth and €75–80m maintenance. We forecast a total of €95m and note that the lower capex spend in FY19 will enable the company to achieve its goal of turning net cash flow positive.

Maintenance capex |

2015 |

2016 |

2017 |

2018 |

Argentina |

|

3.5 |

7.1 |

7.4 |

13.0 |

Mexico |

|

12.4 |

21.1 |

28.9 |

25.2 |

Panama |

|

3.2 |

4.8 |

13.9 |

3.2 |

Colombia |

|

3.3 |

2.8 |

1.9 |

2.1 |

Uruguay |

|

0.1 |

9.1 |

5.2 |

7.6 |

Brazil |

|

0.0 |

0.2 |

0.1 |

0.0 |

Italy |

|

7.1 |

10.7 |

6.8 |

4.7 |

Spain |

|

16.8 |

24.2 |

22.5 |

21 |

Other |

|

0.6 |

0.4 |

0.4 |

5.3 |

Total maintenance capex |

|

47.0 |

80.4 |

87.1 |

82.1 |

% of sales |

|

2.9% |

5.2% |

5.3% |

5.6% |

Growth capex |

|

|

|

|

Argentina |

|

6.5 |

2.0 |

0.0 |

1.9 |

Mexico |

|

2.1 |

1.3 |

28.4 |

43.4 |

Panama |

|

0.0 |

0.0 |

0.0 |

5.7 |

Colombia |

|

0.0 |

0.6 |

2.5 |

2.2 |

Uruguay |

|

1.2 |

31 |

0.0 |

0.0 |

Brazil |

|

1.2 |

0.1 |

0.1 |

0.0 |

Italy |

|

4.9 |

0.3 |

6.5 |

0.2 |

Spain |

|

3.0 |

11.7 |

26.7 |

27.9 |

Total growth capex |

|

18.9 |

47.0 |

64.2 |

81.3 |

% of sales |

|

|

|

3.9% |

5.5% |

Total capex |

|

65.9 |

127.4 |

151.3 |

163.4 |

Balance sheet: Net debt/EBITDA of 3.1x

As we detail on pages 19–20, Codere successfully restructured its balance sheet in 2016 and at the end of FY18, it reported net debt of €781.6m vs €748.6m in FY17. Adjusting for IFRS 16, net debt was €1,120m at Q119, which includes €75.7m cash.

Debt profile: €500m/$300m senior notes due 2021

Codere reported total financial debt of €866.6m at Q119, of which €782.7m was from senior notes (from the 2016 refinancing), as well as €85.7m of debt at the operating company level. Including €309.3m of capitalised operating leases, total adjusted debt was €1.2bn at Q119.

As shown in Exhibit 18 below, this resulted in net debt of €810.9m (pre-IFRS), which leads to a net debt/adjusted EBITDA of 2.9x. Post IFRS 16 adjustments, the net debt/adjusted LTM EBITDA was 3.1x. This is comfortably within all its banking covenants and the credit agency ratings are B2 (Moody’s) and B (S&P), both with a stable outlook, suggesting liquidity is regarded as adequate.

Codere expects to generate positive net cash in FY19, which is in line with our forecast of a €5.6m net cash flow in FY19. Assuming no major unforeseen FX changes, we forecast net debt of €1,093m in FY19 and €1,039m in FY20. In terms of cash balance, we assume that the company pays back a net amount of c €20–30m bank debt annually. Note that IFRS 16 has added c €309m to gross debt.

The senior notes are due in 2021 and there are sizeable licence renewals from Argentina and Italy in 2021–24 (c €80m). We therefore expect the company will look to refinance and/or seek an equity issuance before then.

Exhibit 18: Capitalisation (€m) and leverage ratios (x)

Capitalisation table |

2018 |

Q119 |

Opco Debt |

|

|

|

|

81.4 |

85.7 |

Opco Capital Leases |

|

|

|

|

8.6 |

8.2 |

Super Senior Revolving Credit Facility |

|

|

|

|

9.9 |

10.0 |

Senior Notes |

|

|

|

|

763.5 |

782.7 |

Total Financial Debt |

|

|

|

|

863.4 |

886.6 |

Capitalisation of Operating Leases |

|

|

|

|

316.6 |

309.1 |

Total Adjusted Debt |

|

|

|

|

1180.0 |

1195.7 |

Cash |

|

|

|

|

81.8 |

75.7 |

Net Debt |

|

|

|

|

781.6 |

810.9 |

Total adjusted net debt |

|

|

|

|

1098.2 |

1120.0 |

LTM Adjusted EBITDA |

|

|

|

|

282.9 |

283.0 |

LTM Adjusted EBITDA (post IFRS 16) |

|

|

|

|

350.9 |

363.0 |

Pro-forma Interest Expense |

|

|

|

|

59.9 |

61.8 |

Pro-forma Interest Expense (post IFRS 16) |

|

|

|

|

96.9 |

111.3 |

Leverage |

|

|

|

|

|

|

Senior Financial Debt/LTM Adjusted EBITDA |

|

|

|

|

0.4x |

0.4x |

Total Financial Debt/LTM Adjusted EBITDA |

|

|

|

|

3.1x |

3.1x |

Total Adjusted Net Debt/LTM Adjusted EBITDA (post IFRS 16) |

|

|

|

3.1x |

3.1x |

Total Net Financial Debt/LTM Adjusted EBITDA |

|

|

|

|

2.8x |

2.9x |

including inflation accounting |

|

|

|

|

2.8x |

2.9x |

Coverage |

|

|

|

|

|

|

LTM Adjusted EBITDA/)Pro-forma Interest Expense |

|

|

|

4.7x |

4.6x |

including inflation accounting |

|

|

|

|

4.7x |

4.6x |

")