The adoption of IFRS 15 at the start of FY19 has led to a restatement of H118 and FY19 numbers. H118 revenues are reduced by £0.8m, adjusted operating profit by £0.36m and adjusted EPS by 0.5p. Due to the timing of revenue recognition much of the shortfall was made up in H119, slightly enhancing performance primarily of EID. It should be noted the accounting changes do not affect cash flow.

The salient features of the interim results are as follows:

■

Order intake of £45.6m (H118 £39.2m)

■

Reported closing order book of £108.8m (H118 £132.1m) was up from £102.5m at the start of the year, with £45m to be delivered in H219.

■

By the end of November, this had risen to £135.4m of which £50m is scheduled for delivery by the year end, providing strong order cover of 81% of FY19 consensus forecast expectations.

■

Reported revenues were £39.5m (H118 £44.0m restated for adoption of IFRS 15).

■

Reported adjusted operating profit was £1.0m (H118 £3.3m restated).

■

Reported adjusted EPS was 1.99p (H118 5.80p restated).

■

Reported DPS was 2.85p (H118 2.55p), a 12% increase in line with the group’s progressive dividend policy.

■

Net cash of £4.7m (H118 £5.7m), down from £11.3m at FY18, was lower than expected in part due to inventory build ahead of higher H2 activity.

■

Acquisition of 81.84% of Chess Technologies for total cash consideration of up to £41.9m, including future purchase of the minority holding.

MASS (H119 sales £16.0m; 41% of group sales, adjusted operating profit of £2.18m) produced a revenue decline due to the completion of Electronic Warfare (EW) support work for an export customer. Training support work for the UK Ministry of Defence (MOD) has also declined. New business has been secured under contract and will begin in H219. MASS was selected in October as preferred bidder to provide technical support to a key UK MOD operational requirement. In addition, the business is continuing to see growth in its cyber operations. Overall, MASS’s FY19 revenue expectations are 80% underpinned by the current order book, through conversion of which the company expect to deliver growth year-on-year.

SEA (H119 sales £14.3m; 36% of group sales, adjusted operating profit of £0.38m) saw a moderate decline in revenues, largely due to project timing. In H119, the business had lower submarine revenues and completed a Transport for London project. Meanwhile, ROADflow sales saw positive momentum and oil & gas revenues were flat in the same period. Planned restructuring was completed in H119 at a cost of £0.5m and projected annual saving of £1.0m. Once again, the order book strength, including £17m to be delivered in H219, lends support for FY19 growth year-on-year.

EID (H119 sales £3.7m; 9% of group sales, adjusted operating loss of £0.27m) performance reflected timing issues in both naval and tactical (land) divisions. While some major projects completed in FY18, there were also order delays. However, the defence market backdrop in Portugal is supportive of upgrade system work plus the order book already supports a return to profitability in H219 and for the FY19.

MCL (H119 sales £5.5m; 14% of group sales, Adjusted operating profit of £0.03m) revenue and operating profits were below expectations, reflecting lower margin/higher volume activity for the UK MOD plus an order cancellation. MCL has been building its order book and looks set to deliver growth year-on-year.

Acquisition of Chess Technologies

Cohort also announced on 12 December the acquisition of 81.84% of Chess Technologies, from existing cash and financing facilities. The outline of the deal timing and financial conditions are as follows:

■

Initial consideration of £20.1m for 81.84%, payable on completion.

■

Additional earn-out for selling shareholders of up to £12.7m based on revenue performance to 30 April 2021.

■

Acquisition of remaining shares (18.16%) for up to £9.1m after 30 April 2021. This will be based on the company’s order book and EBIT performance.

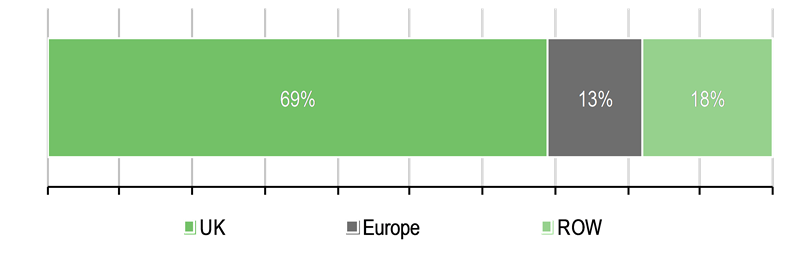

Chess was founded in 1993, employs over 140 people and is based in Horsham (UKHQ), Plymouth (UK), Wokingham (UK) and Denver, Colorado (US). The business has two operating units: Chess Dynamics Ltd and Vision4ce Ltd. The core technology focus is providing a suite of surveillance and fire control systems for defence programmes and commercial infrastructure projects. With around one third of FY18 revenues from the UK, Chess brings to Cohort a broad geographic reach including, importantly, access to the growing US defence market for the first time.

Chess has a diversified client base, with over 100 customers and not more than 15% of company revenues from any one customer. FY18 (30 April year end) revenues were £18.2m (FY17 £16.5m) and FY18 EBIT of £2.4m (FY17 £1.6m). The closing order book at 30 April 2018 was £31.2m (FY17 £28.2m) and supports further growth in FY19.

Assuming a WACC of 8% and a tax charge of 17%, Chess will have to increase EBIT to over £4m to create value, should the earn-out agreement be payable in full.

As a Tier 1 or Tier 2 supplier Chess only sells 34% of its primarily product-based offering to UK-based customers, some of which goes on systems exported indirectly. The US presence is the first foothold for Cohort in the defence market, which may enable it to raise awareness of its capabilities and offerings across the rest of the divisions. There is a modest commercial element of 6% of sales, but the focus is on defence and security markets.

Exhibit 1: Chess Technologies FY18 sales by region

|

Exhibit 2: Chess Technologies FY18 sales by segment

|

|

|

|

|

|

Exhibit 1: Chess Technologies FY18 sales by region

|

|

|

|

Exhibit 2: Chess Technologies FY18 sales by segment

|

|

|

|

The products offered have a good balance between naval and land, with the custom products relating to radar control systems. There is also a growing C-UAS (counter unmanned air systems) offering, which is an area of significant interest and where Chess has demonstrated operational capability.

We have adjusted our earnings assumptions to reflect three factors: a modest boost from IFRS 15, an adverse trading mix largely at EID and the benefit of consolidating Chess, which will be immediately earnings enhancing. The changes are reflected in Exhibit 3:

Exhibit 3: Cohort earnings estimates revisions

Year to April (£m) |

2019e |

2020e |

|

Prior |

New |

% change |

Prior |

New |

% change |

MASS |

39.8 |

39.8 |

0.0% |

42.2 |

43.4 |

2.9% |

SEA |

38.2 |

38.2 |

0.1% |

40.1 |

38.9 |

(2.9%) |

MCL |

19.7 |

22.0 |

11.7% |

20.9 |

20.9 |

0.1% |

EID |

20.8 |

18.0 |

(13.5%) |

21.6 |

26.6 |

23.1% |

Chess |

|

8.0 |

|

|

21.0 |

|

Total group revenues* |

118.4 |

125.9 |

6.4% |

124.8 |

150.8 |

20.9% |

|

|

|

|

|

|

|

EBITDA |

17.3 |

17.8 |

3.3% |

18.3 |

21.1 |

15.1% |

|

|

|

|

|

|

|

MASS |

7.6 |

8.0 |

5.8% |

8.0 |

8.0 |

(0.4%) |

SEA |

4.6 |

5.2 |

13.4% |

4.8 |

5.4 |

12.5% |

MCL |

2.4 |

2.3 |

(3.1%) |

2.5 |

2.0 |

(20.6%) |

EID |

4.4 |

3.0 |

(31.6%) |

4.5 |

4.6 |

0.8% |

Chess |

|

1.0 |

|

|

2.6 |

|

HQ other and intersegment |

(2.8) |

(2.9) |

4.2% |

(2.8) |

(3.0) |

7.8% |

EBIT (pre PPA amortisation) |

16.1 |

16.6 |

3.0% |

17.1 |

19.6 |

14.6% |

|

|

|

|

|

|

|

Underlying PTP |

16.0 |

16.3 |

1.6% |

17.0 |

18.9 |

11.3% |

|

|

|

|

|

|

|

EPS - underlying continuing (p) |

31.2 |

32.3 |

3.5% |

33.2 |

36.1 |

8.6% |

DPS (p) |

9.2 |

9.2 |

0.0% |

10.1 |

10.1 |

0.0% |

Net cash/(debt) |

12.1 |

(16.0) |

N/A |

24.7 |

(6.5) |

N/A |

Source: Edison Investment Research estimates. Note: *After intra-group sales £0.05m.

Adjusting for IFRS and the Chess acquisition, the underlying progress of the continuing activities is now modestly below our previous assumption, but still shows progress on the prior year.

A significant variation is that the company is now forecast to carry net debt of £16m at the year end. While a large part of this is due to the initial consideration payable for the acquisition of Chess, it also reflects the assumption that the group will carry more working capital through its year end in anticipation of higher activity levels in FY20 as it starts to execute significantly increased order backlogs.

The new £30m banking facility that is now drawn to the extent of £25m including £18m for the Chess consideration and carries a net debt/EBITDA covenant of 2.5x, which Cohort remains comfortably within at less than 1.0x.

")

")

")

")

(before Chess)")