PEY invests in direct private equity transactions alongside other Partners Group-managed funds and accounts, and private debt investments overseen by Partners Group, as well as co-investing with other private equity managers (such as 3i, the lead investor in PEY’s largest holding, Action). Its primary focus is on mid-cap buyouts (enterprise value of c €500m–2bn) where Partners Group has a controlling or majority position, either as the lead investor or as co-lead with another private equity manager. PEY invests in these deals both through Partners Group’s flagship limited partner funds, and as a co-investor. Having previously invested in third-party private equity funds, this has not been a focus for PEY since 2011. While funds still account for 13% of the portfolio, these are mature investments that are now largely in the process of returning capital. Although it is less diversified than a private equity fund of funds (which may have exposure to hundreds of underlying companies), PEY does hold a diversified portfolio, targeting direct investments in c 50–80 companies in order to reduce the volatility of cash flows that might occur with a more concentrated strategy.

Partners Group is a relative value investor, meaning it looks at the pricing of investment opportunities in the context of both history and a relevant peer group. The manager seeks to make direct investments in companies that are highly cash-generative and/or offer meaningful top-line growth potential. In an environment of generally high prices for private equity deals, Partners Group has found it beneficial to focus on companies that fit into one or more of the following categories:

■

Platform companies: well-managed businesses that can be expanded via bolt-on acquisitions;

■

Category winners: companies with a strong competitive position in a growing market segment;

■

Defensive leaders: cash-generative businesses in market areas with high barriers to entry.

A fundamental part of the Partners Group private equity investment approach is its industry value creation team (see below), which it uses to help drive through initiatives to enable companies to strengthen their financial and competitive positions, and achieve their full potential.

Private debt investments serve two purposes: uninvested cash may be used to buy first-lien senior loans, which are highly liquid but offer higher returns than other near-cash investments, while second-lien or mezzanine investments are longer-term and may be used to gain exposure to favoured private companies that are not seeking additional equity financing. Partners Group is a conservative lender with a focus on capital preservation, seeking businesses with predictable cash flows, sustainable margins, a conservative capital structure and a stable record of historical performance. All PEY’s debt investments have floating rather than fixed rates of interest, which should be beneficial in a rising interest rate environment.

Investment process: Proactive approach to deal sourcing

Through its primary and secondary private equity teams, along with private debt and infrastructure teams, Partners Group maintains a detailed database of c 8,000 companies from which to source investment ideas. In total, the group has information on more than 20,000 businesses, relationships with c 800 private equity general partners, and representation on c 300 advisory boards. Every investment professional has a target list of companies that they would like to own if the opportunity arose and the team spends time speaking to company managements, working out an investment case, and identifying value creation potential and likely M&A targets. In addition, by providing debt finance, the group can build detailed knowledge of the operational and financial characteristics of private companies (where publicly available information may be scant), giving Partners Group’s investors an advantage in due diligence terms when these companies seek private equity financing.

Partners Group has a highly selective approach to investment, with less than 1% of potential deals on average (0.9% in FY18) making it into the group’s portfolios in any given year. The team screens around 1,000 deals each year (1,054 in FY18) on a high-level basis, looking at industry dynamics, market attractiveness, headline company financials, return potential, exit scenarios and how Partners Group could add value to the business. From this initial screen, c 10–20% of potential deals (20.1% in FY18) are selected for initial due diligence, which assesses a range of quantitative and qualitative factors, and the most promising ideas (69 in FY18) are subjected to advanced due diligence, including in-depth financial modelling, scrutiny of legal terms and an assessment of environmental, social and governance (ESG) factors. Beyond checking on how a company measures up to various ESG metrics, the ESG team also comes up with positive drivers, identifying initiatives that can improve the profile of an asset in ESG terms, and ultimately create value.

Following the due diligence stage, the Partners Group team produces a detailed investment thesis, which includes an operational assessment by the IVC team, and creates a 100-day plan for execution of the deal and implementation of value creation initiatives. The final step of the process is a positive or negative investment recommendation. PEY made nine new direct private equity investments in FY18 (five with Partners Group as lead investor and four co-investments), broadly in line with historical averages. The fund aims to give exposure to c 50–80 companies (not including holdings in legacy third-party funds).

PEY invests mainly through Partners Group’s flagship direct private equity funds, which are raised every three to four years. PEY makes commitments to these funds, and may also make direct ‘top-up’ investments alongside them. Funds may take time to draw down the funds committed to them at launch; the newest programme is Partners Group Direct Equity 2016, which is still in its investment period. In order to smooth out the pace of investment and avoid ‘cash drag’, which may occur when cash is returned to the portfolio (for example, as a result of realisations from legacy third-party funds) but is not drawn down by the direct funds, PEY may also make direct co-investments with other managers. As well as reducing cash drag, co-investments bring additional diversification to the portfolio, while reducing costs as they do not incur an extra layer of fund fees.

New private equity positions are typically 0.5–3.0% of NAV; PEY aims to express conviction in its investments and position sizes are ideally at least 2.0%. However, this depends to an extent on the apportionment of investments across Partners Group strategies, as allocations may be larger or smaller than targeted. During FY18, several new investments were large enough to be included in PEY’s top 10 holdings. PEY typically holds investments for three to five years. Where an exit comes as the result of a company listing on a stock market, the manager will usually aim to sell down the investment within two years (subject to any lock-ups), although listed companies may be held for longer if there is a strong investment case for doing so.

Partners Group closely monitors investee companies through its board representation, quarterly performance assessments, active engagement with stakeholders and the progress of value creation initiatives. Private equity investments are revalued quarterly (in March, June, September and December), although material changes that may affect the value of an investment will be factored in as they occur.

On the private debt side (c 10% of the portfolio at end-FY18), investments may be made directly by PEY or via Partners Group programmes. Second-lien or mezzanine debt investments target high single- to low double-digit returns, with typical holding periods of two to three years, while liquid first-lien loans are more short-term in nature and are held mainly as a higher-yielding alternative to cash.

PEY uses hedging instruments such as options and forward contracts to reduce the impact of currency fluctuations (primarily $/€) on the portfolio. As a result of this, FX neither contributed to nor detracted from returns for FY18 as a whole. At end-FY18, PEY’s portfolio currency exposure before and after hedging (post-hedging figures in brackets) was 57% euro (86%), 37% US dollar (11%), 5% sterling (2%), and 1% other (1%).

Industry value creation (IVC)

Partners Group sees its IVC team as a key differentiating factor in its – and by extension PEY’s – offering. Many private equity groups engage management consultants to drive through operational improvements at investee companies, but Partners Group’s IVC team is in-house. The team is made up of more than 30 senior executives and entrepreneurs, organised across six industry groups (healthcare, technology, media & telecoms [TMT], education, financial & business services, industrials, and consumer), as well as infrastructure and real estate. The IVC team is involved in the investment process from the earliest stage of deal sourcing, and a key factor in declining a potential investment would be where there is no clearly identifiable opportunity for the team to create value. Where initiatives can be identified, the IVC team draws up a 100-day plan from the point of investment, and creates a five-year roadmap. The team coaches and assists the management of investee companies in the implementation of projects, with all IVC work co-ordinated through a strategic project management office. Examples of current initiatives include the merger of recently purchased industrial belt manufacturers Megadyne and Ammeraal Beltech (now known as Ammega), consolidating the businesses in growing end markets, creating economies of scale, optimising the footprint, and improving distribution and cross-selling opportunities. With software developer GlobalLogic (a new investment in Q318), the Partners Group platform itself is a key driver of value creation, as other investee companies provide both a potential customer base and an additional source of distribution.

There are currently more than 200 value creation initiatives in progress across Partners Group’s 2012 and 2016 direct programmes (funds). PEY director Felix Haldner points out that the systematic value creation approach includes time and consideration taken in composing investee company boards, so that they are tailored to the company and the investment thesis. Partners Group has a large industrial partner network from which it sources non-executive directors and will usually appoint a chairman who has industry-relevant executive experience and can step in as an interim CEO if required.

Financial resources and commitments

PEY received a record level of distributions (€191.1m) from its portfolio in FY17 and started 2018 with net liquid resources of €88.3m (11.9% of NAV). However, after a higher than usual pace of investment activity during the summer (€62.1m in Q318, after adjusting for partial syndications of some deals to third-party investors), net liquidity had fallen to €17.3m (2.2% of NAV) at 30 September 2018, meaning the portfolio was essentially fully invested. For the first nine months of 2018, new investments totalled €128.1m, against €111.8m of distributions. The comparable figures for 9M17 are €80.9m of investments and €113.1m of distributions. At 31 December 2018, €35m of the €50m available credit line was drawn, leading to net liquidity of -€5m (net gearing of 0.7%). The credit line was used on a short-term basis to meet investment commitments; the borrowing was partly repaid in January 2019 and Haldner expects PEY to return to a small net cash position as distributions continue to be received from the legacy funds portfolio.

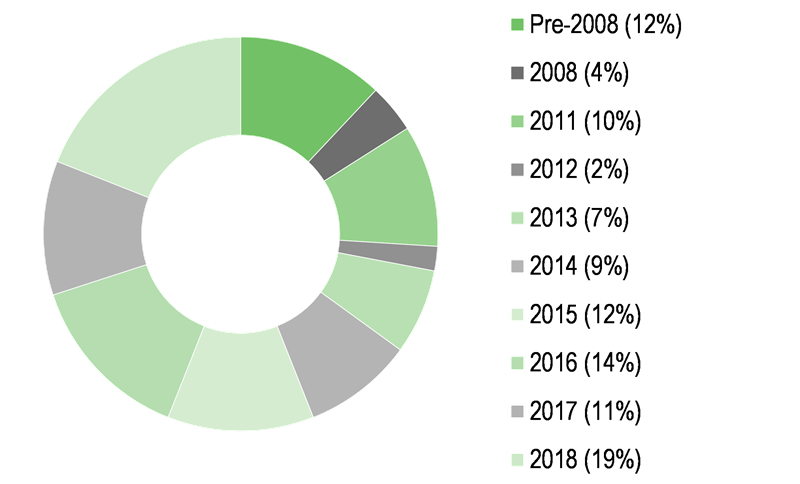

Exhibit 2: Investments and unfunded commitments by vintage

|

Current portfolio by investment year (%) |

Unfunded commitments by fund/programme vintage (%) |

|

|

Source: Princess Private Equity Holding, Edison Investment Research. Note: Data at end-December 2018.

|

Unfunded commitments at end-FY18 stood at €93.7m, including €16.5m to the Partners Group Direct Equity 2016 programme (down from €50m at end-FY17), €14.8m to the 2012 programme (unchanged on end-FY17), €2.2m to a 2011 mezzanine debt programme (€2.1m at end-FY17) and €21.7m of commitments to single-line direct investments (from €18.2m at end-FY17). Unfunded commitments to legacy third-party funds (PEY ceased new fund investments in 2011) stood at €38.5m (41% of total unfunded commitments), down from €39.0m at end-FY17. As shown in Exhibit 2 (right-hand chart), most of these commitments are to pre-2008 vintages, which are long past their initial investment period. Partners Group estimates that PEY’s €22.6m of commitments to pre-2007 vintages (24% of the total) are unlikely to be called, while the majority of the remaining €15.9m, if drawn, is likely to be accounted for by follow-on financing and fees.

Including the €15m (at end-FY18) undrawn borrowing facility and excluding the €22.6m of commitments that are deemed unlikely to be drawn, PEY’s outstanding commitments were equal to 7.11x its liquid resources at 31 December 2018. If all pre-financial crisis commitments are excluded, this falls to 5.47x available resources. However, this should be viewed in the context of the timing of the fund’s drawing on its credit line and its subsequent (post-FY18 end) repayment of the borrowing. At a fully invested position with the €50m credit line undrawn, the comparable figures are 1.42x and 1.09x available resources. PEY has not historically followed an overcommitment strategy – which many private equity managers use to reduce cash drag on money that has been committed to new programmes but has not yet been invested – instead preferring to use senior loans to boost returns on uninvested cash, and co-investments to bridge gaps in the timing of direct programme investments. However, owing to the higher level of new investments than realisations during FY18, PEY’s overcommitments including the credit line stood at 11.1% of NAV at 31 December 2018.

Investments and realisations in FY18

Following on from its record year of realisations in FY17, PEY was more active in making new investments in FY18, particularly in the second half of the year (Exhibit 3). New purchases in H118 included psychometric testing specialist SHL (a €6.3m co-investment in March, alongside Exponent Private Equity Partner), US baked goods firm Hearthside Food Solutions (a €17.8m co-lead investment in May, alongside Charlesbank Capital Partners), roofing products distributor SRS Distribution (€14.1m in June), and digital dentistry firm Amann Girrbach (€8.6m, also in June). July 2018 saw €69.7m of new investments (€17.9m of which was subsequently syndicated to other investors): €19.2m in sub-metering service provider Techem, €19.2m to fund the acquisitions of industrial belt manufacturers Megadyne Group and Ammeraal Beltech, and €21.9m in product engineering and software developer GlobalLogic. In October, €19.1m of debt financing was provided to listed company Envision Healthcare in support of a private equity buyout by KKR, while November saw a €13.8m investment in Vishal Mega Mart, one of India’s largest value retail brands. In total, c €170m was invested during the year (adjusted for the subsequent partial syndication of some deals following the initial investment), including follow-on financing and the purchase of liquid senior loans for liquidity management purposes.

A steady stream of cash was returned by the legacy funds portfolio throughout the year (totalling c €55m of the c €140m realisations in FY18). Notable direct investment realisations during the year included Trimco (€19.4m received in March after the sale of the garment trimmings company to Affinity Equity Partners, with €5.7m reinvested as a co-investment), and €10.3m in July from the sale of Varsity Brands to Bain Capital. The investment in Varsity Brands generated a 3.4x multiple over the acquisition cost in December 2014, while Trimco also generated a return of 3.4x the value at acquisition in May 2012. In line with its strategy of selling down holdings in companies that have listed on a stock market, PEY received €12.4m from the sale of its remaining shares in Swiss vacuum valve manufacturer VAT Group in January 2018, and sold €5.2m worth of shares in Black Knight Financial Services between February and May. On the private debt side, proceeds of €3.6m were realised in June 2018 from a debt investment in Cooperation Pharmaceutique Française, while €3.8m of a shareholder loan to hospitality and catering firm Vermaat was repaid in December, partially de-risking the investment by returning a substantial portion of its cost.

Exhibit 3: Investments and realisations in FY18

|

|

Source: Princess Private Equity Holding, Edison Investment Research. Note: investment figures have been adjusted for post-investment syndications.

|

Current portfolio positioning

At 31 December 2018, PEY’s top 10 direct holdings accounted for 42.3% of the portfolio (see Exhibit 1), up from 35.7% a year earlier. Three of the top 10 holdings – private equity stakes in GlobalLogic and Hearthside Food Solutions, and a private debt investment in Envision Healthcare Holdings – were new investments in FY18.

Exhibit 4: Investments by geography and sector

|

Investments by geography (%) |

Investments by industry sector (%) |

|

|

Source: Princess Private Equity Holding, Edison Investment Research. Note: As at 31 January 2019 (geographical); 31 December 2018 (industry sector).

|

PEY aims to hold 50–80 direct investments (not including underlying holdings in legacy third-party funds, which had fallen to 13% of the portfolio at 31 December 2018), and primarily focuses on the mid-cap segment of the market, which made up 59% of the portfolio at 31 December 2018 (see Exhibit 1). The fund is globally diversified, taking a relative value approach to regional allocation. At end-January 2019 (Exhibit 4, left-hand chart), 51% of the portfolio was invested in Europe, a 1pp reduction from 52% at 31 January 2018. North American exposure had risen from 32% to 34%, while Asia Pacific fell from 8% to 7%, and the 8% exposure to the rest of the world was unchanged on a year earlier. The portfolio is also broadly diversified by sector (Exhibit 4, right-hand chart), although it has deliberately low exposure to cyclical industries. Compared with the MSCI AC World index, a broad global index of listed companies, PEY’s portfolio has very high exposure to consumer discretionary companies (30.0% versus 10.6% for the index), and a significantly lower weighting to financial stocks (8% versus 20.5% for the index). Sector allocations remained broadly stable over FY18, with most changes being 2pp or less in either direction.

Exhibit 5: Portfolio by sponsor type (% unless stated)

|

Portfolio end-December 2018 |

Portfolio end-December 2017 |

Change (pp) |

Partners Group lead/co-lead |

62.0 |

58.0 |

4.0 |

Co-investments |

14.0 |

12.0 |

2.0 |

Funds |

13.0 |

19.0 |

(6.0) |

Debt |

11.0 |

11.0 |

0.0 |

|

100.0 |

100.0 |

|

Source: Princess Private Equity Holding, Edison Investment Research

As shown in Exhibit 5, Partners Group lead or co-lead investments grew as a percentage of the portfolio during 2018, as did PEY co-investments, while the proportion in funds continued to fall as the mature legacy fund holdings returned cash.

Exhibit 6: Valuation and performance metrics for direct portfolio

Valuation metrics (as at 31 December 2018) |

|

Performance metrics (12m to 31 December 2018) |

|

EV/EBITDA |

13.0x |

Revenue growth |

10.2% |

Net debt/EBITDA |

5.4x |

EBITDA growth |

11.5% |

Leverage |

43.2% |

Weighted average revenue |

€1.1bn |

Weighted average EV |

€2.5bn |

|

|

Source: Princess Private Equity Holding, Edison Investment Research

In terms of the performance of portfolio companies (Exhibit 6), the manager points to strong revenue and EBITDA (earnings before interest, tax, depreciation and amortisation) growth of 10.2% and 11.5% respectively over 12 months to 31 December 2018, far in excess of the rate of GDP growth in any large economy. In valuation terms, EV/EBITDA (where EV is enterprise value) multiples rose from 12.2x at 31 December 2017 to 13.0x at 31 December 2018, and net debt/EBITDA rose from 4.7x to 5.4x. The leverage ratio (net debt as a percentage of enterprise value) was broadly stable, at 43.2% versus 40.6% at 31 December 2017.

")