Company description: From post to global logistics enterprise

SingPost is a long-established company, but its traditional core market of domestic postal services has been in structural decline for many years. The subsequent ongoing pivot to logistics, both in Australia and as a global e-commence logistics solutions provider, is transformative and requires management with a suitable skill set. The strategic review has highlighted key changes in the group that are designed to identify the divisional value drivers and the potential to recycle stranded capital from non-core assets into areas of growth such as Australia.

Valuation: Sum-of-the-parts valuation implies c 50% upside

Following BofA’s strategic review of SingPost, we value the group at S$0.72/share on a sum-of-the-parts basis, which implies c 50% upside from the current depressed share price. The review identified operations and assets within the group that are non-core or underperforming and, as such, could become targets for capital recycling. To this end, post review reinvestment may result in a group that is more focused on growth and potentially better able to unlock value, and thus create further potential upside for investors.

The key drivers of value are the Australia division, which is worth more than the company’s entire market capitalisation, and the SingPost Centre, which is of comparable value.

Financials: Strength of cash flow and balance sheet hidden

We believe investors should think about SingPost not as the operator of a structurally declining and loss-making postal operator in Singapore, but as a large and growing logistics company in Australia, with a recovering international cross-border business as well as a postal business in Singapore that is stable and potentially profitable. After the strategic review, it is now possible to identify the non-core assets and businesses that could be sold, with the proceeds reinvested in the core logistics business, thus further reducing its exposure to Singapore and increasing its exposure to its chosen growth market, Australia. The SingPost Centre is a large element of the potential disposal portfolio. This is likely to result in investors attaching a higher valuation to the stock, which we believe is currently hidden from view, assuming successful disposal of the SingPost Centre at a value close to, or in excess of, its book value.

Sensitivities: Exposure to Australia becomes biggest risk

We believe that the biggest sensitivity that SingPost faces is its exposure to the Australian economy and the Singapore dollar/Australian dollar exchange rate, over which it has no control. Clearly, if Australia went into a recession, or its currency was to weaken against SingPost’s reporting currency, the Singapore dollar, then revenues and profits would face headwinds. Furthermore, Australia has been, and is likely to continue to be, the focus of acquisitive expansion, which implies growth, but also carries integration risks. In Singapore itself, the structurally declining postal market is a headwind and the company cannot yet rely on the regulator to continually push postal rates up to offset volume losses. Finally, Singapore Telecom (SingTel) (Temasek’s interest held via SingTel) (22%) and Alibaba (15%) hold 37% of the shares collectively and could ultimately reduce their holdings, which could put pressure on the share price. That said, neither shareholder has made any mention of reducing exposure.

Company description: Pivoting to an international logistics enterprise

SingPost is a long-established company, but its traditional core market of domestic postal services has been in structural decline for many years. The subsequent ongoing pivot to logistics, both in Australia and as an international e-commence logistics solutions provider, is transformative and requires management with a suitable skill set. The March 2024 strategic review was designed to underpin this change and to identify stranded capital that can be recycled in the business to accelerate this transformation. SingPost generates more than 85% of revenue and operating profit from outside its home market, Singapore, but we and management believe the market significantly undervalues the latent value within the group, which is driving the reorganisation of SingPost.

Divisional structure refocused and clarified

Singapore Post Private Limited (SingPost), formerly a subsidiary of SingTel, was the body in charge of the country’s postal system and services. Its history can be traced back to the early days after Singapore was founded in 1819, but its modern form stretches from its privatisation on 1 April 1992 and subsequently its listing on the Singapore stock exchange in May 2003. Given the structural decline of postal services globally, and the current strategic pivot away from postal services to logistics, its biggest revenue generator is its expanding logistics operations in Australia. In Singapore it maintains a universal post and parcel delivery service, an e-commerce logistics business and a network of post offices, and an international postal capability. The Corporate division contains a freight forwarding business, the SingPost Centre and some other minor operations.

Before the strategic review, SingPost was made up of three divisions (see Exhibit 1 below): Logistics (principally in Australia), Post and Parcel, and Property. However, following the strategic review, the business will be reported on a new basis (see Exhibit 2), which is expected to better illustrate the group’s core activities:

■

Australia, which accounts for c 56% of FY25e revenue, is principally made up of three acquired businesses: FMH, CouriersPlease and the recently acquired Border Express.

■

Singapore (14% of revenue) consists of the domestic post and parcel operations, the Post Office network and e-commerce.

■

International (15% of revenue): post and parcel operations.

■

Corporate: the remaining 15% of revenue is classified as corporate and primarily consists of the freight forwarder Famous Holdings, the property portfolio and some other minor non-core businesses. The operations in Corporate may be the subject of management’s focus on capital management and subject to potential disposal.

Exhibit 1: SingPost – revenue by division before strategic review (FY25e)

|

Exhibit 2: SingPost – revenue by division after strategic review (FY25e)

|

")

|

")

|

Source: SingPost, Edison Investment Research

|

Source: SingPost, Edison Investment Research

|

Exhibit 1: SingPost – revenue by division before strategic review (FY25e)

|

|

Source: SingPost, Edison Investment Research

|

Exhibit 2: SingPost – revenue by division after strategic review (FY25e)

|

|

Source: SingPost, Edison Investment Research

|

We discuss the strategic review and its implications later in the note, but one major outcome could be the disposal of the S$1.1bn SingPost Centre, which could raise significant capital that could be reinvested in the logistics diluting Singapore revenues further.

Experienced management team

Given the level of change that has already occurred within the business and the change that is likely in the future as the company continues to pivot to logistics and execute the recommendations identified by the strategic review, a strong and experienced management team is crucial. The biographies of the top team, detailed below, appear, in our opinion, to contain the right experience and skill set to navigate this important period of change.

Chairman: Simon Israel was appointed to the role in 2016. He is also a director of Stewardship Asia Centre CLG and a member of the Global Leadership Council of Leapfrog Investments. Mr Israel is a former chairman of Singapore Telecommunications and Asia Pacific Breweries, as well as an executive director and president of Temasek Holdings (Private) before retiring in 2011. Prior to that, he was chairman, Asia Pacific of the Danone Group. Mr Israel has also held various positions in Sara Lee Corporation before becoming president (household & personal care), Asia Pacific.

Group Chief Executive Officer: Vincent Phang Heng Wee was appointed as group chief executive officer of SingPost on 1 September 2021 to lead SingPost in its transformation strategy to drive its next phase of growth. Mr Phang first joined SingPost in April 2019 as chief executive officer for postal services and Singapore, which encompasses all SingPost’s core businesses in Singapore, including post, parcel and logistics. In that role, Mr Phang was responsible for leading the delivery network in Singapore, through a comprehensive and customer-centric suite of logistics, mail and parcel solutions. He was also responsible for SingPost’s international postal relationships. Mr Phang has over 20 years of regional experience in the supply chain, logistics, industrial and manufacturing industries in Asia, having served in various senior leadership roles including CEO of ST Logistics. Mr Phang holds a master of aeronautic engineering (first class honours) from the Imperial College, United Kingdom, and a post graduate diploma in flight test engineering from International Test Pilots School, United Kingdom.

Group Chief Finance Officer: Vincent Yik joined SingPost in December 2021 and is responsible for overall financial matters of the group, including financial and management reporting, taxation, investment management, risk management, treasury and other corporate matters. Vincent has more than 20 years of finance-related experience and, before assuming his current role, served as CFO at OUE Lippo Healthcare. Prior to that, Vincent held key executive roles, including CFO of Far East Orchard (a member of Far East Organization), chief operating officer, Australia Properties of Far East Organization, Sydney, as well as CFO, Australia & New Zealand Banking Group, Singapore Branch. Vincent holds a bachelor of commerce from the University of Queensland, Australia.

Chief Executive Officer, International: Li Yu was appointed as CEO, international of SingPost on 12 September 2022. He leads the development and growth of the international markets, advancing the cross-border e-commerce logistics business and orchestrating efficient supply chains for customers globally. Li Yu has over 17 years of experience spanning engineering, operations, project management, customer/sales support, strategy and technology implementation. He joined SingPost's management team from United Parcel Service (UPS), where he was most recently responsible for its APAC global logistics and distribution. Li also has experience in transformational P&L and commercial leadership. He led an e-commerce portfolio as part of the broader logistics line of business, and grew businesses including those in the ecommerce, healthcare, manufacturing and retail sectors in his previous roles.

Clear strategic direction revealed

SingPost is on a journey to de-emphasise its exposure to its declining domestic post and parcel market, and reallocate non-core capital to expand its international logistics activities, notably in Australia. To date, it has established a top five position in Australia, having acquired CouriersPlease (2014), FMH (2020–23) and Border Express (March 2024). This process is likely to be enhanced following the strategic review, which may result in capital recycled from non-core corporate operations into Australia and potentially elsewhere.

Strategic review principles defined

In 2023 SingPost appointed BofA to begin the process of a strategic review of its portfolio of businesses and the structure of the group. Its stated objectives were to improve shareholder returns and ensure the group is appropriately valued. The overarching theme of the review was to move progressively towards becoming a logistics company, divesting non-core businesses and assets, and recycling capital to support further growth and transformation.

In July 2023, the chairman outlined the company’s key principles that it wanted to address during the strategic review exercise. There included:

■

Defining what is core and non-core in the context of transitioning to a logistics business over time.

■

Divestment of non-core businesses/assets and those that it does not expect to earn a return above their cost of capital.

■

Recycling capital to support further investment in logistics.

■

Resetting the group’s dividend policy.

■

Optimising the group’s balance sheet and gearing.

■

Ensuring the structure of the group allows the group and its underlying businesses to be appropriately valued, while creating optionality for the future of these businesses

Medium-term strategic thrusts revealed

On 19 March 2024, SingPost announced the conclusion of its year-long strategic review, which is focused on creating market leading positions, orientating to growth and generating shareholder value. The board has agreed five strategic ‘thrusts’, which will be implemented over the next three years and are highlighted in Exhibit 3. Two of the five relate to the group at a corporate level, and the other three relate to high-level objectives for each of the three divisions. Each ‘thrust’ is detailed below.

Exhibit 3: Five strategic thrusts for the next three years

|

|

|

|

Reorganisation of the group

The group will be reorganised into three core business units: Singapore, Australia and International. The fourth unit is Corporate, which falls outside the long-term focus of the group. The three core units will operate independently in their respective markets with a focus on developing market-leading positions and building core capabilities in line with individual strategies. The separation is designed to provide clarity on the valuation of the individual businesses with reference to market and sector ratings. The revised corporate structure is designed to create flexibility and generate optionality, which could include the disposal of minority stakes to demonstrate core value. This potential can be clearly demonstrated by the comparison of the current market capitalisation of the whole group of c S$1.1bn, compared to just the SingPost Centre, which was valued at the end of March 2024 at a similar figure by the company.

Exhibit 4: Vision of the international logistics enterprise

|

|

|

|

Strategic management of capital

SingPost will continue to actively manage capital deployed in its portfolio of businesses and subject each to regular reviews of financial performance and returns against set targets. The target for each business unit is to generate a spread above the cost of capital. The group has identified a list of assets and businesses that are non-core to its strategy and that could be monetised to facilitate the recycling of capital. This includes selected properties as well as various assets in its international footprint. Potential proceeds would be appropriately allocated by the board to either reduce debt, support investment in growth opportunities and/or return value to shareholders in line with its new dividend policy, which is to pay out 30% to 50% of underlying net profit as dividends.

Exhibit 5: Unlock and recycle capital

|

|

|

|

Transforming urban logistics and deliveries in Singapore

The Singapore business unit will focus on maintaining its market-leading position in deliveries and building on its core postal network capability to participate in the structural growth of e-commerce logistics, while innovating and transforming the urban logistics landscape in Singapore. SingPost will continue to target building a best-in-class delivery network in terms of service, efficiency and sustainability.

Letters and printed papers make up almost 50% of the Singapore division’s revenue and are now profitable, following the price rise in October 2023, while another 10% is accounted for by the loss-making post office network, which is likely to be restructured. The remaining 41% is accounted for by ecommerce revenue in Singapore, which Statista forecasts will grow at more than 10% pa between 2024 and 2029 (March 2024).

Exhibit 6: Cost-effective logistics solutions for long-term financial sustainability

|

|

|

|

Achieving scale in Australia

SingPost’s Australian logistics network is now the fifth largest operation in a highly fragmented market. The business unit will leverage the asset-light hybrid 4PL and third-party logistics (3PL) capabilities and seek to strengthen its market position. (3PL is traditional warehousing and vehicle logistics, whereas 4PL is where the operator manages the logistics demands of an entity, utilising multiple logistics providers.) SingPost may also pursue partnerships that add to growth and/or supply equity to pay down acquisition debt. This may also offer an independent valuation yardstick. The group will continue to engage in M&A in a fragmented market and seek third-party funding to maximise value.

Exhibit 7: Nationwide coverage in Australia

|

Exhibit 8: Pro forma segmental revenue breakdown, Q323

|

|

|

|

|

|

Exhibit 7: Nationwide coverage in Australia

|

|

|

|

Exhibit 8: Pro forma segmental revenue breakdown, Q323

|

|

|

|

Building tech-driven excellence to serve cross-border customers

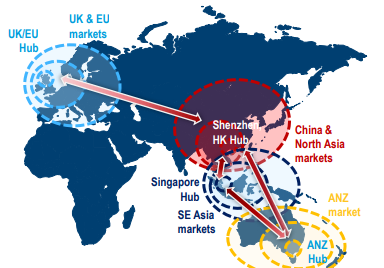

SingPost’s International division will focus on serving its e-commerce customers via an asset-light model and its recently launched 4PL platform ARRIV. The new system was designed to enhance customer experience, bolster its partnership network and achieve operational excellence in international connectivity. It will drive to expand its hubs in Singapore, Hong Kong and Europe and explore options to enhance its e-commerce supply chain network globally.

Exhibit 9: International connectivity potential

|

|

|

|

Strategic pivot from post to Australian logistics

SingPost’s foray into the steadily growing and fragmented Australian logistics market has accelerated in recent years with the acquisitions of FMH and recently Border Express. Furthermore, with the strategic review now complete, we believe it is likely that certain ‘non-core’ assets could be monetised and the capital raised could be invested in lifting its number five market position, or indeed returned to shareholders. In addition, we expect losses in Singapore and the International divisions to be eliminated such that, either way, Australia is likely to become an even more dominant division within the group.

Given SingPost’s starting position was that of a monopoly provider of postal services in Singapore and the structural challenges that this industry has faced for many years, it is no surprise that the company has chosen to pivot away from this declining industry, towards logistics, where it can utilise its long experience in high service provision in delivery and build a sustainable long-term logistics platform. This process has been evolving for many years following the original purchase of CouriersPlease in 2014.

Exhibit 10: Transformation of SingPost into a global logistics operator

|

|

|

|

SingPost has progressed its strategy to transform the company into an international logistics business. It has prioritised investing in Australia given the proximity and size of the logistics market, its profitability and potential returns. SingPost will be fully integrating CouriersPlease and Border Express into FMH in the next 12 months, which will position the company to offer B2B2C logistics solutions with significant growth potential. SingPost describes the combination of the three businesses as ‘an extensive end-to-end B2B2C integrated logistics network powered by technology’.

FMH has grown revenue and profit, both organically and through roll-up acquisitions. We expect FMH to continue its growth and to explore further acquisitions as it increases its network and capabilities. At the end of FY25, the first full year of ownership of Border Express, we anticipate that SingPost’s Australian logistics business will generate revenue of c S$1.2bn, approximately 56% of group revenue.

CouriersPlease is one of Australia’s leading metropolitan small-parcel delivery businesses. It has extensive national coverage and a low-cost network, and operates an asset-light franchisee model, with depots located primarily in eastern and southern Australia, comprising the majority of the Australian delivery market.

Management believes that FMH is the leading 4PL service provider based in Australia, providing integrated supply chain and distribution services through a proprietary technology platform. FMH has been expanding its geographical reach and 3PL capabilities as part of the group’s strategy to develop a digitally enabled integrated B2B and B2C logistics business.

Border Express, the sixth largest pallet and parcel distribution operator in Australia, has a presence across every state and territory in Australia, with comprehensive freight connectivity, warehouses and regional centres, providing end-to-end interstate logistics services. With a network of 16 facilities, a fleet of over 700 vehicles and a team of 1,300 employees, Border Express has over 3,000 clients from across industries, including large retail and consumer brands.

Exhibit 11: Map of SingPost’s Australian logistics network

|

|

|

|

Australian logistics market is set to grow steadily

The Australian logistics market grew revenue by 3.4% pa (source IBISWorld) between 2018 and 2023 and is forecast to grow 1.3% pa between 2023 and 2028, and it is this steady growth that is one of the key attractions of the Australian logistics market. Collectively, we estimate that SingPost will account for c 2–3% of the very fragmented Australian logistics market, where the top five players account for less than 20% of revenue and a large number of relatively small players make up the other 80%+, implying scope for consolidation.

Given the strategy, the cash-generative nature of the group (discussed later) and the fragmented Australian logistics market, we believe it is only a matter of time before more M&A is announced and the group’s exposure to this growing market is increased.

The Singapore division accounts for c 14% of revenue and includes three interconnected operations: the domestic post and parcel operations, which are now profitable after the postage rate increase with effect from 9 October 2023; a fast-growing e-commerce logistics operation; and a network of 57 loss-making post offices. SingPost has a universal obligation to deliver to every address over the 284 square miles of the territory. There is postal competition, but only SingPost has access to mailboxes in high-rise blocks, which limits the attractiveness of the postal market to third parties.

SingPost’s second largest division, accounting for c 15% of revenue, is its International division, which is its cross border e-commerce business, including an international post and parcels business. This business is based in the regional airport/multimodal hubs of Singapore, Hong Kong, Shenzhen, Australia and Belgium, which effectively cover the South-East Asian markets, China and North Asia, Australia, New Zealand and Europe (EU, UK and others).

Exhibit 12: International cross-border e-commerce logistics network

|

|

|

|

Profits by division; Australia dominates

Exhibit 14 below shows the operating profit (before ‘other’ which are unallocated overhead costs ) generated from the various business in SingPost’s new, post-review shape. We expect Australia, already the largest division by profit in FY23 and FY24e, to almost double its profit in FY25 with the full-year inclusion of Border Express, while we believe losses in Singapore and International were eliminated by FY24 due to post rate rises, volume increases and self-help initiatives (such as efficiency drives) assisting profitability.

We believe that Freight Forwarding profits ‘normalised’ in FY24 at lower levels following an exceptional FY23, and that SingPost Centre profit remained largely flat given the predictable nature of the rental income. Both of these businesses could be considered ‘non-core’.

Exhibit 13: EBIT (pre ‘other’ ) by division and year

|

by division and year")

|

Source: SingPost, Edison Investment Research

|

This exhibit ignores the potential for the disposal of the SingPost Centre assets (described below) that management valued at c S$1.1bn (as at end March 2024), which could be reinvested in M&A in Australia, entirely in line with the new strategy. The same would be true if SingPost was to dispose of its Freight Forwarding business, which is classified under Corporate in the new divisional breakdown. In this scenario, the group would consist of a very profitable Australian operation, and two smaller, modestly profitable operations in Singapore and International. Equally, given the new strategy of the group, it is possible that this capital could be allocated to shareholders if it was unable to find satisfactory acquisition targets.

Balance sheet headroom from redeployment of capital

At the outset of the strategic review, the chairman highlighted that the disposal of loss-making or underperforming assets was a key priority. We believe that, assuming SingPost transitions into a leading logistics operator in Australia, there is significant value to be unearthed in the rest of the group’s portfolio.

In particular, SingPost is the owner of an extensive investment property portfolio, which we believe is non-core. The portfolio is revalued every year by an independent valuer and was valued in the FY24 preliminary results at S$1.0bn and includes the SingPost Centre, which was valued at S$1.1bn. SingPost Centre hosts SingPost’s headquarters and is partly used for mail sorting. We understand that these operations could be co-located to the parcel sorting site located at Tampines, which would offer certain operational synergies. SingPost Centre also has commercial space, including office space and a retail mall. The building has a gross floor area of 1,476,100 sq ft and a net lettable area of 980,210 sq ft. As of end-March 2024, SingPost Centre’s occupancy rate stood at 96.2%, down from 98.2% in March 2023, with the retail mall space at 99.6% occupancy and office space occupancy at 94.8%, implying healthy demand. SingPost Centre sits on land held by SingPost on a 99-year lease from 30 August 1982.

In FY23, the total investment property portfolio generated revenue of c S$54m pa, implying a gross yield of c 5.6%, which could be attractive to property investors in the region. It generated an operating profit of S$44m in the period. SingPost also owns a portfolio of associates and joint ventures, listed on the balance sheet with a combined value of S$23.1m, which could also be sold. Collectively, these two groups of assets have a potential disposal value of c S$1bn (see exhibit below), which is not materially short of the market capitalisation of the whole company.

Additionally, SingPost has a post office network of c 51 branches in the territory, which in their current form are loss-making. Following the review, SingPost may decide that the network could be structured in a different way, which could see the portfolio run more efficiently.

Exhibit 14: Non-core asset value (FY24)

Asset |

% held |

FY24 valuation (S$m) |

Investment properties |

100% |

1,002.3 |

Associates and joint ventures |

|

|

GDEX Berhad |

12% |

|

Dash Logistics |

30% |

|

Efficient E-Solutions |

21% |

|

Morning Express |

33% |

|

Paya Lebar Central Partnership |

33% |

|

Total associates and JVs |

|

23.1 |

Total non-core assets value |

|

1,025.4 |

Source: SingPost, Edison Investment Research

Sustainability targets taken seriously

SingPost is actively working towards achieving net-zero goals for its operations in Singapore by 2030 and globally by 2050. The group has implemented various initiatives to optimise operational efficiency, reduce wastage, utilise renewable energy and shift to low carbon transportation options.

In FY23 SingPost aligned its practices with the Task Force on Climate-Related Financial Disclosures (TCFD) recommendations and framework, and participated in the 27th session of the Conference of the Parties of the UNFCCC (COP 27) to promote decarbonisation across the logistics sector. The group also actively engages in community investment, and places importance on corporate governance, diversity and inclusion. It aims to lead in the green economy by tapping into opportunities and addressing the challenges that climate change presents.

Historical board issues resolved

Some years ago, SingPost was beset with issues relating to the make-up of the board, with several serving members having been on the board for a particularly long time, which also raised investor concerns relating to judgement and age. We believe these issues are now no longer relevant as the board has been renewed in recent years. There are nine board members, all appointed since 2016. The current chairman, Simon Israel, was appointed in 2016 and the group CEO, Vincent Phang Heng Wee, was appointed in September 2021 to oversee the transformation of the company. We therefore believe that the historical board concerns have been resolved.

Sensitivities: Exposure to Australia is key

We believe that the biggest sensitivity that SingPost faces is its exposure to the Australian economy and currency. Clearly, if the country went into recession, or its currency weakened against SingPost’s reporting currency, the Singapore dollar, revenues and profits would face headwinds. Furthermore, Australia has been, and is likely to continue to be, the focus of acquisitive expansion, which implies growth, but also carries integration risks. In Singapore itself, the structurally declining postal market is a headwind and the company cannot rely on the regulator to continually push postal rates up to offset volume losses. Finally, SingTel (22%) and Alibaba (15%) hold 37% of the shares collectively and could ultimately reduce their holdings, which could put pressure on the share price. That said, neither shareholder has made any mention of reducing exposure.

Macroeconomic and currency related risks

Most other material risks to the business could be categorised as either macroeconomic or currency related. On the operational side, particularly in Logistics, the biggest risk we see is unexpected volume declines, which might be the result of a slowing of either the Australian or the global economy. In this scenario, clearly lower volumes would lead to lower revenue, but FMH’s 4PL business is asset light and CouriersPlease operates a franchise model for delivery. which implies risks are mitigated. In the international operations, revenue and costs are much more elastic and so costs are likely to move more in line with volumes.

From a currency point of view, the translation of mainly Australian dollar revenue and profits into Singapore dollars would have a negative impact on reported figures in periods of Singapore dollar strength versus the Australian dollar, which is the current long-term trend. In the International business in particular, SingPost enters many contracts in Chinese renminbi (yuan), which can have an effect depending on its relative strength versus the Singapore dollar.

Integration and strategic review risks

SingPost completed the purchase of Border Express (BEX) on 1 March 2024. The company has been active in acquisitions for many years in Australia, so we view the risk of integrating BEX into the business as relatively low, but execution risk remains. Furthermore, the outcome of the strategic review could have unforeseen outcomes, such as workforce unrest due perhaps to facility closures or relocations, and any anticipated disposals may not achieve the value anticipated. Indeed, even if value is achieved, the reinvestment of capital may not produce the returns anticipated.

Postal review and focus on e-commerce could reduce risks of losses

SingPost holds the only licence for the delivery of letters in Singapore, and this implies an obligation to deliver to every address, regardless of its profitability. This is often referred to as the ‘universal service obligation’. For a long time this worked well, given the fairly predictable volume of post and SingPost’s understanding of cost. However, for many years now, postal volumes have been in structural decline and the cost base has risen, and in FY23 and H124, SingPost reported losses. Discussions with the regulator resulted in the first postal rate rise for many years, from 31c to 51c, from 9 October 2023, which management anticipates will return the business to profitability, at least for the foreseeable future, although volumes are likely to remain in decline and costs are likely to increase.

We understand that SingPost and its regulator are jointly reviewing the postal services including its network, against the outlook of further letter declines, but growth in e-commerce volumes. We believe this government support provides some comfort that the business will be commercially sustainable over the longer run. Exhibit 16 illustrates the growth in eCommerce volumes by quarter in FY24 demonstrating SingPost’s success in attracting new business.

Exhibit 15: Growth in e-commerce volumes (year-on-year)

|

")

|

|

|

In the International area, the Universal Postal Union Congress sets the delivery rates every four years with reference to local delivery charges. These include caps and floors in the rate increase. The last rise was between 10% and 17% set in 2021, to take effect from 2023.

Valuation offers considerable upside

Post the strategic review of SingPost, we value the group at S$0.72/share on a sum-of-the-parts basis, which implies c 50% upside from the current depressed share price. The review was designed to identify operations and assets within the group that are non-core or underperforming and, as such, could become targets for capital recycling. To this end, post review reinvestment may result in a group that is more focused on growth and potentially better able to unlock value, and thus create further potential upside for investors.

Sum-of-the-parts valuation implies c 50% upside

Given the transformation of SingPost from a declining traditional postal operator collecting and distributing letters and parcels on a largely domestic basis in a relatively densely populated geography, into a global logistics solutions provider, we believe it is best to value the company on a sum-of-the-parts basis. This is even more appropriate when considering the degree of overlap in the businesses between the divisions, which although it exists, in reality, is perhaps not the primary reason for the development of the logistics business, which is largely in Australia.

In the table below we have valued the three divisions separately: the Australia logistics division; Singapore, which is made up of three subdivisions (Logistics – letters and printed papers, Logistics – e-commerce and the Post Office network); and International. In addition, we have valued the SingPost Centre at its FY24balance sheet value and separated out the Famous freight forwarding business. Finally, we have applied a 7.5x multiple to the ‘Other’ division, which represents mainly intersegmental costs and is a deduction to the overall value.

We have estimated the FY25 EBITDA of the Australia business, with a full year of Border Express (the deal was completed in March 2024), and applied an EV/EBITDA multiple of 8.2x, being the average FY25e multiple of four quoted Australian logistics companies. It would appear that size is relevant, as the multiples of Freightways and Qube are somewhat higher than those at the smaller end of the spectrum. The average applied to Singapore Post sits comfortably within the range.

Exhibit 16: Sum-of-the-parts valuation

Division |

Basis |

EBITDA (S$m) FY25 |

Multiple (x) |

Valuation (S$m) |

Comment |

Australia |

EV/EBITDA |

140.7 |

8.2 |

1,157.9 |

Average of four quoted Australian listed logistics companies |

Singapore |

EV/EBITDA |

22.0 |

6.6 |

144.3 |

Average of four quoted global postal companies |

International |

EV/EBITDA |

22.6 |

5.0 |

113.8 |

Average of six quoted global logistics companies |

Freight Forwarding |

EV/EBITDA |

22.8 |

5.0 |

115.1 |

Average of six quoted global logistics companies |

SingPost Centre |

Balance sheet value |

44.2 |

- |

1,091.0 |

31 March, 2024 value, taken from FY24 presentation commentary |

Other |

EV/EBITDA |

(34.1) |

7.5 |

(256.1) |

|

Value of divisions |

|

218.1 |

|

2,366.0 |

|

Net debt |

|

|

|

|

|

Net debt including leases |

|

|

|

(499.1) |

FY24e |

Perpetual securities |

|

|

|

(251.5) |

FY24e |

Total net debt |

|

|

|

(750.6) |

FY24e |

|

|

|

|

|

|

Equity value (S$m) |

|

|

|

1,615.4 |

|

|

|

|

|

|

|

Shares outstanding |

|

|

|

2,249.9m |

|

Value per share (S$) |

|

|

|

0.72 |

|

Current price |

|

|

|

0.48 |

|

Upside/(downside) to implied value/share |

|

|

|

50% |

|

Source: Edison Investment Research

We have applied a similar rationale to the Singapore division, valuing the operations against a range of international peers, which are no doubt all experiencing the same declining volume and rising costs pressures, as electronic communications continue to replace physical post. The average multiple of 6.6x is clearly lower than the more robust Australia peer average multiple, but also gives credit for the monopolistic characteristics that post and parcel companies tend to enjoy.

Finally, we have valued the International division with reference to peers and valued the SingPost Centre at the FY24 balance sheet value, recognising that the portfolio is revalued every year. At the end of FY23, the property portfolio was revalued by external agent Colliers International Consultancy and Valuation (Singapore).

Exhibit 17: Comparative valuation

|

|

|

Market cap |

EV/EBITDA (x) |

P/E (x) |

Company |

Country |

Year end |

(S$m) |

FYa |

FY1e |

FY2e |

FYa |

FY1e |

FY2e |

|

|

|

|

(x) |

(x) |

(x) |

(x) |

(x) |

(x) |

|

|

|

|

|

|

|

|

|

|

Singapore Post Ltd |

Singapore |

Mar-25 |

1,103.4 |

9.9 |

7.8 |

7.5 |

26.9 |

16.2 |

13.5 |

|

|

|

|

|

|

|

|

|

|

Freightways Group Ltd |

Australia |

Jun-24 |

1,166.4 |

9.5 |

9.1 |

8.3 |

19.0 |

18.6 |

15.9 |

Qube Holdings Ltd |

Australia |

Jun-24 |

5,677.6 |

15.7 |

15.4 |

14.3 |

29.1 |

24.5 |

24.1 |

Silk Logistics Holdings Ltd |

Australia |

Jun-24 |

108.8 |

4.4 |

4.1 |

3.7 |

7.6 |

10.1 |

7.6 |

CTI Logistics Ltd |

Australia |

Jun-24 |

102.4 |

3.9 |

- |

- |

- |

- |

- |

Move Logistics Group Ltd |

Australia |

Jun-24 |

37.5 |

5.3 |

8.4 |

6.6 |

-6.1 |

-2.5 |

-4.3 |

Wiseway Group Ltd |

Australia |

Jun-24 |

14.5 |

11.4 |

- |

- |

- |

- |

- |

Average |

- |

- |

|

8.4 |

9.2 |

8.2 |

12.4 |

12.7 |

10.8 |

|

|

|

|

|

|

|

|

|

|

Yamato Holdings Co Ltd |

Japan |

Mar-25 |

5,364.0 |

6.0 |

4.7 |

4.0 |

15.9 |

13.8 |

10.2 |

JD Logistics Inc |

Hong Kong |

Dec-24 |

10,834.2 |

4.2 |

3.9 |

3.8 |

27.8 |

17.8 |

13.6 |

Sinotrans Ltd |

Hong Kong |

Dec-24 |

7,608.7 |

7.9 |

7.8 |

7.5 |

7.4 |

7.6 |

7.0 |

YUNDA Holding Co Ltd |

China |

Dec-24 |

4,437.0 |

5.4 |

4.9 |

4.5 |

14.8 |

11.4 |

9.8 |

Kerry Logistics Network Ltd |

Hong Kong |

Dec-24 |

2,742.6 |

5.8 |

5.5 |

5.1 |

20.9 |

10.6 |

9.6 |

CJ Logistics Corp |

South Korea |

Dec-24 |

2,575.5 |

5.4 |

5.5 |

5.3 |

10.8 |

9.2 |

7.9 |

Average |

- |

- |

|

5.8 |

5.4 |

5.0 |

16.3 |

11.7 |

9.7 |

|

|

|

|

|

|

|

|

|

|

Japan Post Holdings Co Ltd |

Japan |

Mar-25 |

41,667.7 |

- |

-55.1 |

-47.8 |

18.7 |

13.5 |

11.0 |

CTT Correios de Portugal SA |

Portugal |

Dec-24 |

908.6 |

- |

15.7 |

14.6 |

10.1 |

13.3 |

11.5 |

PostNL NV |

The Netherlands |

Dec-24 |

932.8 |

4.1 |

4.0 |

3.7 |

11.4 |

11.6 |

8.9 |

Bpost SA |

Belgium |

Dec-24 |

1,003.2 |

1.9 |

1.7 |

1.7 |

4.7 |

5.6 |

5.5 |

Oesterreichische Post AG |

Austria |

Dec-24 |

3,171.7 |

6.8 |

6.5 |

6.3 |

16.5 |

16.3 |

15.6 |

Average |

- |

- |

|

4.3 |

7.0 |

6.6 |

12.3 |

12.1 |

10.5 |

Source: LSEG, Edison Investment Research. Note: Priced at 15 May 2024.

Strategic review designed to add value

Given the structural issues that face the business, especially the domestic postal operation that was lossmaking in FY23, the management of SingPost has completed a review of the group structure and the assets within it. The review was designed to improve shareholder returns and ensure the group is appropriately valued. The review is expected to result in certain assets being sold, thus realising their real potential value.

Given the transformation of the group towards a full-service global logistics company, centred on the growing Australian market, it feels likely that any capital that is recycled from the existing operations of the group would be redeployed in this activity, either in Australia or potentially neighbouring geographies. This refocusing of capital may lead to value creation, which could add to the upside described above.

Financials: Strength of cash flow and balance sheet hidden

We believe investors should think about SingPost not as the operator of a structurally declining and loss-making postal operator in Singapore, but as a large and growing logistics company in Australia, with a traditional postal business in Singapore that is likely to become increasingly regulated but profitable, plus an International e-commerce delivery business. These three entities are backed up by a Corporate division that contains the SingPost Centre, the freight forwarding arm and other smaller operations. Following the strategic review, it is possible that these corporate ‘non-core’ businesses could be sold, with the proceeds reinvested in the core logistics business, thus further reducing its exposure to Singapore and increasing its exposure to its chosen growth market, Australia. This is likely to result in investors reassessing the value of the stock, which we believe is currently hidden from view, as discussed in the previous section.

Earnings quality to increase as regulator eliminates loss risk

In SingPost’s new divisional structure, the Australia division is the main generator of both revenue and revenue growth, mainly through the acquisitions of CouriersPlease, FMH and Border Express, which completed in March 2023. We anticipate low growth in the short to medium term, reflecting the macroeconomic trends in Australia. However, given the fragmented nature of the industry, it is quite possible that the division could grow by acquisition, with SingPost acting as a consolidator. We assume margins edge up from 5.8% in FY23 to 5.9% in FY24, and then accelerate to 7.1% in FY25 and 7.9% in FY26.

The Singapore division is very interesting. Although volumes have been in structural decline, particularly in the domestic markets, it remained profitable until FY23, when it reported an operating loss of S$10.6m. We believe it was loss-making again in H124, but we believe it returned to profit in H224 following the review of the postal charges from 9 October. This is a very interesting and perhaps poorly understood situation. We believe that the regulator would like to see a viable postal system maintained.

Exhibit 18: SingPost – post-strategic review divisional operating profit breakdown

|

|

Source: SingPost, Edison Investment Research

|

We believe it is therefore fair to assume that SingPost and the regulator are likely to establish a mechanism that gives SingPost a decent chance of generating a profit, in return for certain measurable outputs. Thus, from an investor’s point of view, the worst-case scenario would be a division that broke even or made a small profit every year, rather than potentially generating significant losses on an annual basis, thus removing the risk of substantial losses.

The International division returned to profit in FY24 as price rises and self-help measures take effect. Management expects it to sustain its improvements.

The final division is Corporate, which includes the freight forwarder Famous Holdings, SingPost Centre and ‘others’. Famous is likely to see profit normalise in FY24 at much lower levels, due to overearning in the COVID-affected FY23, and the SingPost Centre should see revenue and profit at roughly the same level as last year given the predictable nature of the rental income streams generated.

Cash flows of c S$60–70m pa set to pay down debt

SingPost is a cash-generative company, producing c S$150m pa of net cash flow from operations, post working capital movements and tax. After investing c S$55m pa in capex, c S$10m in dividends to perpetual shareholders that rank as ‘debt’ and c S$18m pa in net interest, its underlying cash generation is c S$60–70m pa. Excluding M&A, this explains much of the movement in net debt from S$236.6m at the end of FY22 to S$128.7m at FY23, implying a net debt to EBITDA ratio at that point of 0.7x.

The ratio rose to c 2.0x at the end of FY24, following the normalisation of profits from the freight forwarding division, which was over-earning post COVID-19 in FY23, and an increase in net debt due largely to the acquisition of the remaining stakes in FMH and the purchase of Border Express. We expect the net debt/EBITDA ratio to fall to 1.4x in FY25 and, assuming no further M&A investment, we believe the ratio will fall back to c 1.0x in FY26. We assume no business or asset disposals in forecast years, but in the wake of the strategic review, assets sales are entirely possible and these would clearly reduce debt levels. Equally, the proceeds could be reinvested in M&A or returned to shareholders.

Exhibit 19: Net debt, EBITDA and net debt to EBITDA ratio

|

|

Source: SingPost, Edison Investment Research

|

Balance sheet: Dominated by investment properties

The main feature of the balance sheet is the investment properties. These are a collection of office, retail and industrial buildings on long leases, including the SingPost Centre, valued at S$1,002m as at 31 March 2024. This is broadly similar to the entire market capitalisation of the group, which is c S$1.1bn. Given the relatively low level of net debt, the balance sheet is arguably under-geared and offers management flexibility and options.

In addition to the net debt discussed above, SingPost has c S$251.5m in perpetual securities, which are debt-like equity. Technically they are shares, but holders rank higher for dividends than the ordinary shareholders. The dividends are paid semi-annually at a rate of 4.35%, with a review due in 2027. SingPost is not obliged to pay the dividend, nor redeem the shares.

Exhibit 20: Financial summary

|

|

S$m |

2020 |

2021 |

2022 |

2023 |

2024 |

2025e |

2026e |

2027e |

31-March |

|

|

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

IFRS |

INCOME STATEMENT |

|

|

|

|

|

|

|

|

|

|

Revenue |

|

|

1,313.8 |

1,404.7 |

1,665.6 |

1,872.3 |

1,686.7 |

2,124.9 |

2,198.5 |

2,278.7 |

Cost of Sales |

|

|

(1,313.8) |

(1,404.7) |

(1,665.6) |

(1,872.3) |

(1,686.7) |

(2,124.9) |

(2,198.5) |

(2,278.7) |

Gross Profit |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

EBITDA |

|

|

209.8 |

141.3 |

175.3 |

175.3 |

173.4 |

222.1 |

244.1 |

254.2 |

Normalised operating profit |

|

|

141.8 |

72.5 |

100.8 |

92.7 |

92.3 |

128.0 |

150.0 |

160.1 |

Amortisation of acquired intangibles |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Exceptionals |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Share-based payments |

|

|

(2.8) |

(3.0) |

4.5 |

0.4 |

(7.4) |

(4.0) |

(4.0) |

(4.0) |

Impairment |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Other |

|

|

4.6 |

9.7 |

6.7 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Reported operating profit |

|

|

143.6 |

79.3 |

112.1 |

93.2 |

84.9 |

124.0 |

146.0 |

156.1 |

Net Interest |

|

|

(5.8) |

(7.6) |

(11.4) |

(17.5) |

(20.3) |

(20.3) |

(22.8) |

(20.2) |

Joint ventures & associates (post tax) |

|

|

(0.1) |

1.0 |

4.8 |

0.0 |

(1.5) |

(1.5) |

(1.5) |

(1.5) |

Exceptionals |

|

|

(9.1) |

(12.5) |

1.9 |

(7.7) |

36.8 |

0.0 |

0.0 |

0.0 |

Profit Before Tax (norm) |

|

|

126.8 |

53.5 |

96.1 |

75.3 |

70.5 |

106.1 |

125.7 |

138.3 |

Profit Before Tax (reported) |

|

|

128.6 |

60.3 |

107.4 |

68.0 |

99.9 |

102.1 |

121.7 |

134.3 |

Reported tax |

|

|

(28.3) |

(13.3) |

(19.6) |

(29.2) |

(18.4) |

(30.6) |

(36.5) |

(40.3) |

Profit After Tax (norm) |

|

|

98.4 |

40.2 |

76.5 |

46.0 |

52.0 |

75.5 |

89.2 |

98.0 |

Profit After Tax (reported) |

|

|

100.3 |

47.0 |

87.7 |

38.8 |

81.5 |

71.5 |

85.2 |

94.0 |

Minority interests |

|

|

2.8 |

0.6 |

(4.6) |

(14.1) |

(3.1) |

0.0 |

0.0 |

0.0 |

Discontinued operations |

|

|

(12.0) |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Net income (normalised) |

|

|

89.2 |

40.8 |

71.9 |

31.9 |

48.9 |

75.5 |

89.2 |

98.0 |

Net income (reported) |

|

|

91.1 |

47.6 |

83.1 |

24.7 |

78.3 |

71.5 |

85.2 |

94.0 |

|

|

|

|

|

|

|

|

|

|

|

Basic average number of shares outstanding (m) |

|

2,250 |

2,250 |

2,250 |

2,250 |

2,250 |

2,250 |

2,250 |

2,250 |

EPS - Pre distribution to perpetual securities holders (norm) (c) |

4.05 |

1.82 |

3.20 |

1.42 |

2.17 |

3.35 |

3.96 |

4.36 |

EPS - Pre distribution to perpetual securities holders (IRFS) (c) |

4.05 |

2.12 |

3.69 |

1.10 |

3.48 |

3.18 |

3.79 |

4.18 |

EPS - Post distribution to perpetual securities holders (norm) (c) |

3.30 |

1.15 |

2.59 |

0.94 |

1.69 |

2.87 |

3.48 |

3.87 |

EPS - Post distribution to perpetual securities holders (IRFS) (c) |

3.39 |

1.46 |

3.09 |

0.62 |

3.00 |

2.69 |

3.30 |

3.69 |

DPS (c) |

|

|

2.70 |

1.10 |

1.80 |

0.60 |

0.74 |

1.27 |

1.51 |

1.67 |

|

|

|

|

|

|

|

|

|

|

|

Revenue growth (%) |

|

|

14.4 |

(-0.2) |

(-28.9) |

21.0 |

50.9 |

(-1.8) |

0.0 |

0.0 |

Gross Margin (%) |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

EBITDA Margin (%) |

|

|

16.0 |

10.1 |

10.5 |

9.4 |

10.3 |

10.5 |

11.1 |

11.2 |

Normalised Operating Margin |

|

|

10.8 |

5.2 |

6.1 |

5.0 |

5.5 |

6.0 |

6.8 |

7.0 |

|

|

|

|

|

|

|

|

|

|

|

BALANCE SHEET |

|

|

|

|

|

|

|

|

|

|

Fixed Assets |

|

|

1,966.0 |

2,028.4 |

2,115.2 |

2,074.3 |

2,374.9 |

2,341.3 |

2,312.7 |

2,286.1 |

Intangible Assets |

|

|

297.4 |

314.5 |

529.4 |

501.0 |

636.3 |

636.3 |

636.3 |

636.3 |

Tangible Assets |

|

|

441.5 |

405.4 |

412.5 |

386.9 |

454.3 |

422.2 |

395.2 |

370.1 |

Investments & other |

|

|

1,227.2 |

1,308.4 |

1,173.3 |

1,186.4 |

1,284.4 |

1,282.8 |

1,281.3 |

1,279.7 |

Current Assets |

|

|

785.6 |

693.4 |

564.3 |

763.5 |

761.0 |

864.7 |

916.9 |

970.4 |

Stocks |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Debtors |

|

|

262.1 |

166.4 |

234.1 |

229.8 |

252.4 |

306.1 |

308.6 |

312.1 |

Cash & cash equivalents |

|

|

502.8 |

508.3 |

289.0 |

496.2 |

477.1 |

529.2 |

581.0 |

633.2 |

Other |

|

|

20.7 |

18.7 |

41.2 |

37.5 |

31.5 |

29.4 |

27.3 |

25.1 |

Current Liabilities |

|

|

(756.7) |

(594.8) |

(829.4) |

(719.9) |

(698.0) |

(757.5) |

(768.8) |

(780.0) |

Creditors |

|

|

(507.9) |

(507.2) |

(668.1) |

(634.0) |

(605.8) |

(653.1) |

(658.4) |

(665.8) |

Tax and social security |

|

|

(40.5) |

(19.8) |

(24.5) |

(22.4) |

(10.6) |

(22.8) |

(28.7) |

(32.5) |

Short term borrowings |

|

|

(157.0) |

(9.5) |

(77.5) |

(1.4) |

(10.3) |

(10.3) |

(10.3) |

(10.3) |

Other |

|

|

(51.3) |

(58.4) |

(59.2) |

(62.2) |

(71.3) |

(71.3) |

(71.3) |

(71.3) |

Long Term Liabilities |

|

|

(352.6) |

(455.5) |

(705.9) |

(743.6) |

(1,017.0) |

(983.6) |

(950.3) |

(917.0) |

Long term borrowings |

|

|

(207.5) |

(312.8) |

(439.5) |

(623.0) |

(816.8) |

(816.8) |

(816.8) |

(816.8) |

Other long term liabilities |

|

|

(145.2) |

(142.7) |

(266.4) |

(120.6) |

(200.1) |

(166.8) |

(133.5) |

(100.1) |

Net Assets |

|

|

1,642.3 |

1,671.4 |

1,144.2 |

1,374.3 |

1,421.0 |

1,464.9 |

1,510.6 |

1,559.5 |

Minority interests |

|

|

(42.9) |

(47.8) |

165.3 |

7.4 |

(37.5) |

(37.5) |

(37.5) |

(37.5) |

Shareholders' equity |

|

|

1,599.4 |

1,623.6 |

1,309.5 |

1,381.7 |

1,383.5 |

1,427.4 |

1,473.1 |

1,522.1 |

|

|

|

|

|

|

|

|

|

|

|

CASH FLOW |

|

|

|

|

|

|

|

|

|

|

Op Cash Flow before WC and tax |

|

|

156.3 |

115.7 |

162.2 |

121.3 |

162.5 |

165.6 |

179.3 |

188.2 |

Returns on investment and other |

|

|

1.6 |

6.7 |

(1.3) |

(18.6) |

(38.4) |

0.0 |

0.0 |

0.0 |

Working capital |

|

|

24.8 |

109.3 |

(55.5) |

(8.2) |

(34.9) |

(7.4) |

2.1 |

3.8 |

Exceptional & other |

|

|

(5.1) |

(5.1) |

(26.2) |

6.3 |

(12.5) |

(13.6) |

(8.6) |

(8.6) |

Tax |

|

|

(36.3) |

(35.5) |

(24.0) |

(32.8) |

(31.0) |

(18.4) |

(30.6) |

(36.5) |

Other |

|

|

41.9 |

24.3 |

34.4 |

47.6 |

47.7 |

60.9 |

64.2 |

65.5 |

Net operating cash flow |

|

|

183.2 |

215.4 |

89.5 |

115.7 |

93.4 |

187.1 |

206.4 |

212.3 |

Capex |

|

|

(27.0) |

(21.5) |

(23.8) |

(27.7) |

(46.8) |

(54.0) |

(59.0) |

(61.0) |

Acquisitions/disposals |

|

|

2.1 |

(52.3) |

(33.2) |

(166.4) |

(178.0) |

0.0 |

0.0 |

0.0 |

Net interest |

|

|

(9.7) |

(6.0) |

(11.7) |

(15.3) |

(18.1) |

(20.3) |

(22.8) |

(20.2) |

Equity financing |

|

|

46.1 |

(74.5) |

(200.3) |

356.3 |

159.7 |

(33.3) |

(33.3) |

(33.3) |

Dividends |

|

|

(94.6) |

(53.8) |

(41.9) |

(51.5) |

(29.4) |

(27.6) |

(39.5) |

(45.0) |

Other |

|

|

0.7 |

0.8 |

1.8 |

4.2 |

0.3 |

0.0 |

0.0 |

0.0 |

Net Cash Flow |

|

|

100.8 |

8.2 |

(219.5) |

215.3 |

(19.0) |

51.9 |

51.8 |

52.8 |

Opening net debt/(cash) |

|

|

(101.3) |

(128.6) |

(178.9) |

236.6 |

128.7 |

350.4 |

298.5 |

246.7 |

FX |

|

|

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

0.0 |

Other non-cash movements |

|

|

(73.5) |

50.3 |

(415.5) |

107.9 |

(221.7) |

0.0 |

0.0 |

0.0 |

Closing net debt/(cash) |

|

|

(128.6) |

(178.9) |

236.6 |

128.7 |

350.4 |

298.5 |

246.7 |

194.0 |

Source: Company accounts, Edison Investment Research

Contact details |

Revenue by geography (FY23) |

10 Eunos Road 8

Singapore Post Centre

Singapore

408600

+65 6222 5777

www.singpost.com |

|

Contact details |

10 Eunos Road 8

Singapore Post Centre

Singapore

408600

+65 6222 5777

www.singpost.com |

Revenue by geography (FY23) |

|

Management team |

|

Chairman: Simon Israel |

Group Chief Executive Officer: Phang Heng Wee, Vincent |

Simon Israel is a director of Stewardship Asia Centre CLG and a member of the Global Leadership Council of Leapfrog Investments. He is a former chairman of Singapore Telecommunications and Asia Pacific Breweries, and has previously served as a director of Fonterra Co-operative Group, CapitaLand and Stewardship Asia Centre. Mr Israel was a member of the governing board of the Lee Kuan Yew School of Public Policy and Westpac's Asia Advisory Board, as well as an executive director and president of Temasek Holdings (Private), before retiring in 2011. Prior to that, he was chairman of Asia Pacific at the Danone Group. Mr Israel has also held various positions in Sara Lee Corporation, before becoming president (household and personal care), Asia Pacific. He holds a diploma in business studies from the University of the South Pacific. |

Vincent Phang was appointed group chief executive officer Singapore Post on 1 September 2021 to lead the company in its transformation strategy to drive its next phase of growth. He joined Singapore Post in April 2019 as CEO of postal services and Singapore, which encompasses all of the company’s core businesses in Singapore, including Post, Parcel and Logistics. In that role, Mr Phang was responsible for leading the delivery network in Singapore, through a comprehensive and customer-centric suite of logistics, mail and parcel solutions for customers. He was also responsible for the company’s international postal relationships. Mr Phang has over 20 years of regional experience in the supply chain, logistics, industrial and manufacturing industries in Asia, having served in various senior leadership roles including CEO of ST Logistics. He has a master of aeronautic engineering (first-class honours) from Imperial College, UK, and a post graduate diploma (distinction) in flight test engineering from International Test Pilots School, UK. He also attended the Advanced Management Programme at Harvard Business School in 2014. |

Group Chief Finance Officer: Vincent Yik |

Chief Executive Officer, International: Li Yu |

Vincent Yik joined Singapore Post in December 2021 and is the group CFO, responsible for the group’s overall financial matters, including financial and management reporting, taxation, investment management, risk management, treasury and other corporate matters. He has more than 20 years of finance-related experience and, before assuming his current role, served as CFO at OUE Lippo Healthcare. Prior to that, Vincent held key executive roles, including CFO of Far East Orchard (a member of Far East Organization), COO, Australia Properties of Far East Organization, Sydney and CFO, Australia & New Zealand Banking Group, Singapore Branch. He has a bachelor of commerce from the University of Queensland, Australia. Vincent is a member of CPA Australia as well as the Institute of Singapore Chartered Accountants. |

Li Yu was appointed CEO, International of Singapore Post on 12 September 2022. He leads the development and growth of the international markets, advancing the cross-border e-commerce logistics business and orchestrating efficient supply chains for customers globally. Li has over 17 years of experience spanning engineering, operations, project management, customer/sales support, strategy and technology implementation. He joined Singapore Post's management team from United Parcel Service, where he was most recently responsible for its APAC global logistics and distribution. Li also has experience in transformational P&L and commercial leadership. He led an e-commerce portfolio as part of the broader logistics line of business, and grew businesses including those in the e-commerce, healthcare, manufacturing and retail sectors in his previous roles. He has a bachelor of applied science, industrial engineering from the University of Toronto in Canada. |

Management team |

Chairman: Simon Israel |

Simon Israel is a director of Stewardship Asia Centre CLG and a member of the Global Leadership Council of Leapfrog Investments. He is a former chairman of Singapore Telecommunications and Asia Pacific Breweries, and has previously served as a director of Fonterra Co-operative Group, CapitaLand and Stewardship Asia Centre. Mr Israel was a member of the governing board of the Lee Kuan Yew School of Public Policy and Westpac's Asia Advisory Board, as well as an executive director and president of Temasek Holdings (Private), before retiring in 2011. Prior to that, he was chairman of Asia Pacific at the Danone Group. Mr Israel has also held various positions in Sara Lee Corporation, before becoming president (household and personal care), Asia Pacific. He holds a diploma in business studies from the University of the South Pacific. |

Group Chief Executive Officer: Phang Heng Wee, Vincent |

Vincent Phang was appointed group chief executive officer Singapore Post on 1 September 2021 to lead the company in its transformation strategy to drive its next phase of growth. He joined Singapore Post in April 2019 as CEO of postal services and Singapore, which encompasses all of the company’s core businesses in Singapore, including Post, Parcel and Logistics. In that role, Mr Phang was responsible for leading the delivery network in Singapore, through a comprehensive and customer-centric suite of logistics, mail and parcel solutions for customers. He was also responsible for the company’s international postal relationships. Mr Phang has over 20 years of regional experience in the supply chain, logistics, industrial and manufacturing industries in Asia, having served in various senior leadership roles including CEO of ST Logistics. He has a master of aeronautic engineering (first-class honours) from Imperial College, UK, and a post graduate diploma (distinction) in flight test engineering from International Test Pilots School, UK. He also attended the Advanced Management Programme at Harvard Business School in 2014. |

Group Chief Finance Officer: Vincent Yik |

Vincent Yik joined Singapore Post in December 2021 and is the group CFO, responsible for the group’s overall financial matters, including financial and management reporting, taxation, investment management, risk management, treasury and other corporate matters. He has more than 20 years of finance-related experience and, before assuming his current role, served as CFO at OUE Lippo Healthcare. Prior to that, Vincent held key executive roles, including CFO of Far East Orchard (a member of Far East Organization), COO, Australia Properties of Far East Organization, Sydney and CFO, Australia & New Zealand Banking Group, Singapore Branch. He has a bachelor of commerce from the University of Queensland, Australia. Vincent is a member of CPA Australia as well as the Institute of Singapore Chartered Accountants. |

Chief Executive Officer, International: Li Yu |

Li Yu was appointed CEO, International of Singapore Post on 12 September 2022. He leads the development and growth of the international markets, advancing the cross-border e-commerce logistics business and orchestrating efficient supply chains for customers globally. Li has over 17 years of experience spanning engineering, operations, project management, customer/sales support, strategy and technology implementation. He joined Singapore Post's management team from United Parcel Service, where he was most recently responsible for its APAC global logistics and distribution. Li also has experience in transformational P&L and commercial leadership. He led an e-commerce portfolio as part of the broader logistics line of business, and grew businesses including those in the e-commerce, healthcare, manufacturing and retail sectors in his previous roles. He has a bachelor of applied science, industrial engineering from the University of Toronto in Canada. |

Principal shareholders |

(%) |

SingTel |

21.99 |

Alibaba Group Holding |

14.56 |

The Vanguard Group |

2.08 |

Blackrock |

1.01 |

Dimensional Fund Managers |

0.95 |

Norges Bank |

0.89 |

Harbor Capital Partners |

0.62 |

Horizon Investment Programme |

0.40 |

State Street |

0.12 |

Charles Schwab |

0.11 |

|

|

General disclaimer and copyright This report has been commissioned by Singapore Post and prepared and issued by Edison, in consideration of a fee payable by Singapore Post. Edison Investment Research standard fees are £60,000 pa for the production and broad dissemination of a detailed note (Outlook) following by regular (typically quarterly) update notes. Fees are paid upfront in cash without recourse. Edison may seek additional fees for the provision of roadshows and related IR services for the client but does not get remunerated for any investment banking services. We never take payment in stock, options or warrants for any of our services. Accuracy of content: All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report and have not sought for this information to be independently verified. Opinions contained in this report represent those of the research department of Edison at the time of publication. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. Exclusion of Liability: To the fullest extent allowed by law, Edison shall not be liable for any direct, indirect or consequential losses, loss of profits, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. No personalised advice: The information that we provide should not be construed in any manner whatsoever as, personalised advice. Also, the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The securities described in the report may not be eligible for sale in all jurisdictions or to certain categories of investors. Investment in securities mentioned: Edison has a restrictive policy relating to personal dealing and conflicts of interest. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report, subject to Edison's policies on personal dealing and conflicts of interest. Copyright: Copyright 2024 Edison Investment Research Limited (Edison).

Australia Edison Investment Research Pty Ltd (Edison AU) is the Australian subsidiary of Edison. Edison AU is a Corporate Authorised Representative (1252501) of Crown Wealth Group Pty Ltd who holds an Australian Financial Services Licence (Number: 494274). This research is issued in Australia by Edison AU and any access to it, is intended only for "wholesale clients" within the meaning of the Corporations Act 2001 of Australia. Any advice given by Edison AU is general advice only and does not take into account your personal circumstances, needs or objectives. You should, before acting on this advice, consider the appropriateness of the advice, having regard to your objectives, financial situation and needs. If our advice relates to the acquisition, or possible acquisition, of a particular financial product you should read any relevant Product Disclosure Statement or like instrument. New Zealand The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (i.e. without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision.

United Kingdom This document is prepared and provided by Edison for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. A marketing communication under FCA Rules, this document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. This Communication is being distributed in the United Kingdom and is directed only at (i) persons having professional experience in matters relating to investments, i.e. investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the "FPO") (ii) high net-worth companies, unincorporated associations or other bodies within the meaning of Article 49 of the FPO and (iii) persons to whom it is otherwise lawful to distribute it. The investment or investment activity to which this document relates is available only to such persons. It is not intended that this document be distributed or passed on, directly or indirectly, to any other class of persons and in any event and under no circumstances should persons of any other description rely on or act upon the contents of this document. This Communication is being supplied to you solely for your information and may not be reproduced by, further distributed to or published in whole or in part by, any other person.

United States Edison relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. This report is a bona fide publication of general and regular circulation offering impersonal investment-related advice, not tailored to a specific investment portfolio or the needs of current and/or prospective subscribers. As such, Edison does not offer or provide personal advice and the research provided is for informational purposes only. No mention of a particular security in this report constitutes a recommendation to buy, sell or hold that or any security, or that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. |

London │ New York │ Frankfurt 20 Red Lion Street London, WC1R 4PS United Kingdom |

|

|

|

London │ New York │ Frankfurt 20 Red Lion Street London, WC1R 4PS United Kingdom |

|

|

|

|