TEMIT: Broad EM exposure from a well-resourced team

When required, TEMIT’s managers can draw on the deep resources of Franklin Templeton, which is the sixth-largest independent asset manager in the world with more than £1tn of assets under management. The company has been investing in emerging markets for more than 35 years and its emerging markets team of 75+ investment professionals research more than 700 securities. Franklin Templeton views its local presence in 13 emerging market countries as a competitive advantage in terms of building relationships and gaining valuable insights.

TEMIT’s managers seek to capitalise on long-term structural opportunities by identifying companies with sustainable earnings power that are trading at a discount to their intrinsic worth. ESG analysis is an integral part of the investment process.

Looking over the long term, from the date of TEMIT’s launch in June 1989 to end H124 (30 September 2023), the trust’s NAV total return of +3,832.7% is substantially higher than the benchmark’s +1,698.1% total return.

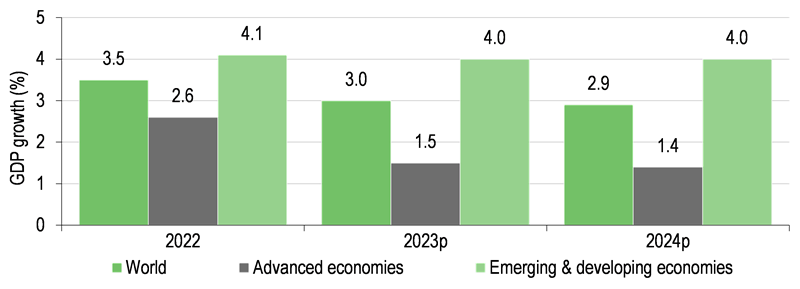

Four important trends in emerging markets contribute to their above-average economic growth potential: favourable demographics, the continued shift towards urbanisation, higher consumption helped by a rising middle class and technological innovation.

Emerging market institutions have made policy improvements. Despite shocks within the US and European banking sectors earlier in 2023, emerging markets’ banking systems have generally been more resilient. This is due to a more conservative approach in response to prior periods of stress such as the 1997–98 Asian financial crisis. Historically, emerging markets were sources of commodities and inexpensive manufacturing. This has shifted to higher demand for premium products and increased technology penetration in the regions. In terms of innovation, some emerging market technology companies have leapfrogged over their developed market peers to become global leaders, such as Taiwan Semiconductor Manufacturing Company, which is the world's largest contract manufacturer of semiconductor chips.

Data from Franklin Templeton show that from January 2008 to December 2022, average annualised rolling five-year total returns in emerging markets were 7.3%. The largest contributor at 5.4% was earnings growth, with dividends contributing 2.7% and higher valuations 0.6%. The combined 8.7% was partially offset by a 1.4% drag from currency movements.

Exhibit 1: Market performance and valuation

|

Performance of indices in £ (last five years) |

Valuation of MSCI indices (at 30 November 2023) |

|

|

Source: Refinitiv, MSCI, Edison Investment Research

|

In terms of performance over the last five years (Exhibit 1, left-hand side), both emerging markets and the UK have woefully lagged the performance of the world market. However, a large part of this is due to the outperformance of the US, which dominates global indices (70% of the MSCI World Index). The shares of large-cap US technology companies have performed particularly well, although there is no guarantee that this will continue. A shift in investor preferences towards markets/sectors that have lagged in recent years could be beneficial for the performance of emerging market stocks.

Emerging market shares continue to look very attractively valued versus their global peers (Exhibit 1, right-hand side). On a forward P/E basis at the end of October 2023, the MSCI Emerging Market Index was around 30% less expensive than the MSCI World Index and offered a higher dividend yield.

TEMIT versus the MSCI Emerging Markets Index

Comparing TEMIT with the benchmark in Exhibit 2, in terms of quality attributes it generates better returns and a has higher net margin, but a modestly lower operating margin than the MSCI Emerging Markets Index. Looking at forward EPS estimates, the trust has a lower growth profile, but is more attractively valued on multiple metrics, while offering a modestly higher dividend yield. Taken in aggregate, TEMIT could be considered as a ‘quality value fund’, which has potential to perform well in a variety of market environments, although it is likely to struggle in a market led by highly valued growth stocks or deep-value cyclical names.

Exhibit 2: Portfolio versus the benchmark (at 31 October 2023)

|

TEMIT’s portfolio |

Benchmark |

Quality |

|

|

Return on assets (%) |

9.6 |

8.5 |

Return on equity (%) |

19.5 |

17.8 |

Return on invested capital (%) |

14.3 |

13.4 |

Operating margin (%) |

19.6 |

20.5 |

Net margin (%) |

19.9 |

17.5 |

Net debt to equity (ex-banks, x) |

0.8 |

20.3 |

Growth |

|

|

Last 3-year sales growth (%) |

17.6 |

18.7 |

Last 3-year EPS growth (%) |

22.6 |

17.4 |

Estimated 3–5-year EPS growth (%) |

11.3 |

14.9 |

Valuation |

|

|

12-month trailing P/E (x) |

10.0 |

11.8 |

Price-to-cash flow (x) |

5.1 |

6.0 |

Price-to-book (x) |

1.3 |

1.5 |

Dividend yield (%) |

3.3 |

3.1 |

Current portfolio breakdown

TEMIT offers investors a broad and differentiated emerging markets exposure. At 30 September 2023, 34 distinct names representing 21% of the portfolio were not held by its major peers. Also, the fund had 30 names that are not represented in its benchmark and made up 17% of the fund.

Exhibit 3: Top 10 holdings (at 31 October 2023)

Company |

Country |

Sector |

Portfolio weight % |

31 Oct 2023 |

31 Oct 2022* |

Taiwan Semiconductor Manufacturing Co |

Taiwan |

Semiconductors & semi equip |

10.5 |

9.6 |

Samsung Electronics |

South Korea |

Technology hardware & equip |

5.6 |

6.6 |

ICICI Bank |

India |

Banks |

5.5 |

7.0 |

Alibaba Group Holding |

China |

Retailing |

5.0 |

4.4 |

Petroleo Brasileiro (Petrobras) |

Brazil |

Energy |

3.2 |

3.0 |

Naver Corporation |

South Korea |

Media & entertainment |

3.1 |

2.9 |

Tencent Holdings |

China |

Media & entertainment |

3.0 |

3.2 |

Samsung Life Insurance |

South Korea |

Insurance |

2.8 |

N/A |

Prosus |

China |

Retailing |

2.7 |

N/A |

LG Corporation |

South Korea |

Capital goods |

2.5 |

2.9 |

Top 10 (% of portfolio) |

|

|

43.9 |

46.1 |

Source: TEMIT, Edison Investment Research. Note: *N/A where not in October 2022 top 10.

At end-October 2023, TEMIT’s top 10 holdings, across a range of countries and sectors, made up 43.9% of the portfolio, which was a lower concentration compared with 46.1% 12 months earlier; eight positions were common to both periods.

The trust has exposure across the market cap spectrum. At end-October 2023, the portfolio was broken down as follows: market cap above $50bn (44.9%); $25–50bn (8.4%); $10–25bn (16.4%); $5–10bn (15.5%); $2–5bn (6.4%) and less than $2bn (8.4%).

There is a new position in the fund: Hypera (formerly known as Hypermarcas) is a leading Brazilian pharmaceutical company that sells prescription, generic and over-the-counter medicines as well as consumer health products. Brazil’s ageing population is a positive growth driver for its pharma industry. Hypera has a portfolio of well-known brands and a good record of new product launches, along with robust cash generation and a strong balance sheet.

TEMIT’s sector and geographic weightings are a result of bottom-up stock selection. As shown in Exhibit 5, over the 12 months to the end of October 2023, the largest changes in the trust’s sector exposure were higher weightings in industrials (+3.8pp) and healthcare (+2.5pp), with lower allocations to financials (-2.4pp) and materials (-2.1pp). In terms of active positioning versus the benchmark, IT remained the largest overweight (+5.8pp), while the largest underweight was consumer staples (-3.4pp).

Exhibit 4: TEMIT’s sector weights versus the benchmark (at end-October 2023)

|

")

|

Source: TEMIT, Edison Investment Research. Note: Excludes other net assets.

|

Exhibit 5: Portfolio sector changes and active weights versus benchmark (% unless stated)

|

Portfolio

end-Oct 2023 |

Portfolio

end-Oct 2022 |

Change

(pp) |

Active weight

vs index (pp) |

Information technology |

26.4 |

28.2 |

(1.8) |

5.8 |

Financials |

25.2 |

27.6 |

(2.4) |

2.7 |

Consumer discretionary |

12.1 |

12.5 |

(0.4) |

(1.5) |

Communication services |

9.2 |

8.0 |

1.2 |

(0.2) |

Industrials |

8.4 |

4.6 |

3.8 |

2.0 |

Materials |

6.2 |

8.3 |

(2.1) |

(1.6) |

Healthcare |

4.4 |

1.9 |

2.5 |

0.4 |

Energy |

3.5 |

3.4 |

0.1 |

(1.8) |

Consumer staples |

2.9 |

3.7 |

(0.8) |

(3.4) |

Utilities |

0.5 |

0.0 |

0.5 |

(2.1) |

Real estate |

0.4 |

0.4 |

0.0 |

(1.3) |

Other net assets |

0.7 |

1.4 |

(0.7) |

0.7 |

|

100.0 |

100.0 |

|

|

Source: TEMIT, Edison Investment Research. Note: Numbers subject to rounding.

Looking at TEMIT’s geographic breakdown in Exhibit 7, the largest country weighting is China, although the fund has an underweight position versus the benchmark (-4.3pp). Over the 12 months to the end of October 2023, the largest changes are a higher weighting to China (+2.0pp) and a lower allocation to Brazil (-2.1pp). The largest active weights are an above-index allocation to South Korea (+8.2pp) and below-index allocation to ‘the rest of the world’ (-9.4pp).

Exhibit 6: TEMIT’s geographic weights versus the benchmark (at end-October 2023)

|

")

|

Source: TEMIT, Edison Investment Research. Note: Excludes net other assets.

|

Exhibit 7: Portfolio geographic changes and active weights vs benchmark (% unless stated)

|

Portfolio

end-Oct 2023 |

Portfolio

end-Oct 2022 |

Change

(pp) |

Active weight

vs index (pp) |

China |

25.6 |

23.6 |

2.0 |

(4.3) |

South Korea |

20.0 |

19.6 |

0.4 |

8.2 |

Taiwan |

14.9 |

14.3 |

0.6 |

(0.2) |

India |

13.0 |

13.5 |

(0.5) |

(2.9) |

Brazil |

9.4 |

11.5 |

(2.1) |

4.0 |

US |

3.3 |

4.2 |

(0.9) |

3.3 |

Thailand |

2.5 |

2.7 |

(0.2) |

0.6 |

Rest of the world |

10.6 |

9.2 |

1.4 |

(9.4) |

Other net assets |

0.7 |

1.4 |

(0.7) |

0.7 |

|

100.0 |

100.0 |

|

|

Source: TEMIT, Edison Investment Research. Note: Numbers subject to rounding.